Main issues

What is an option? Calls, puts, and the four basic positions

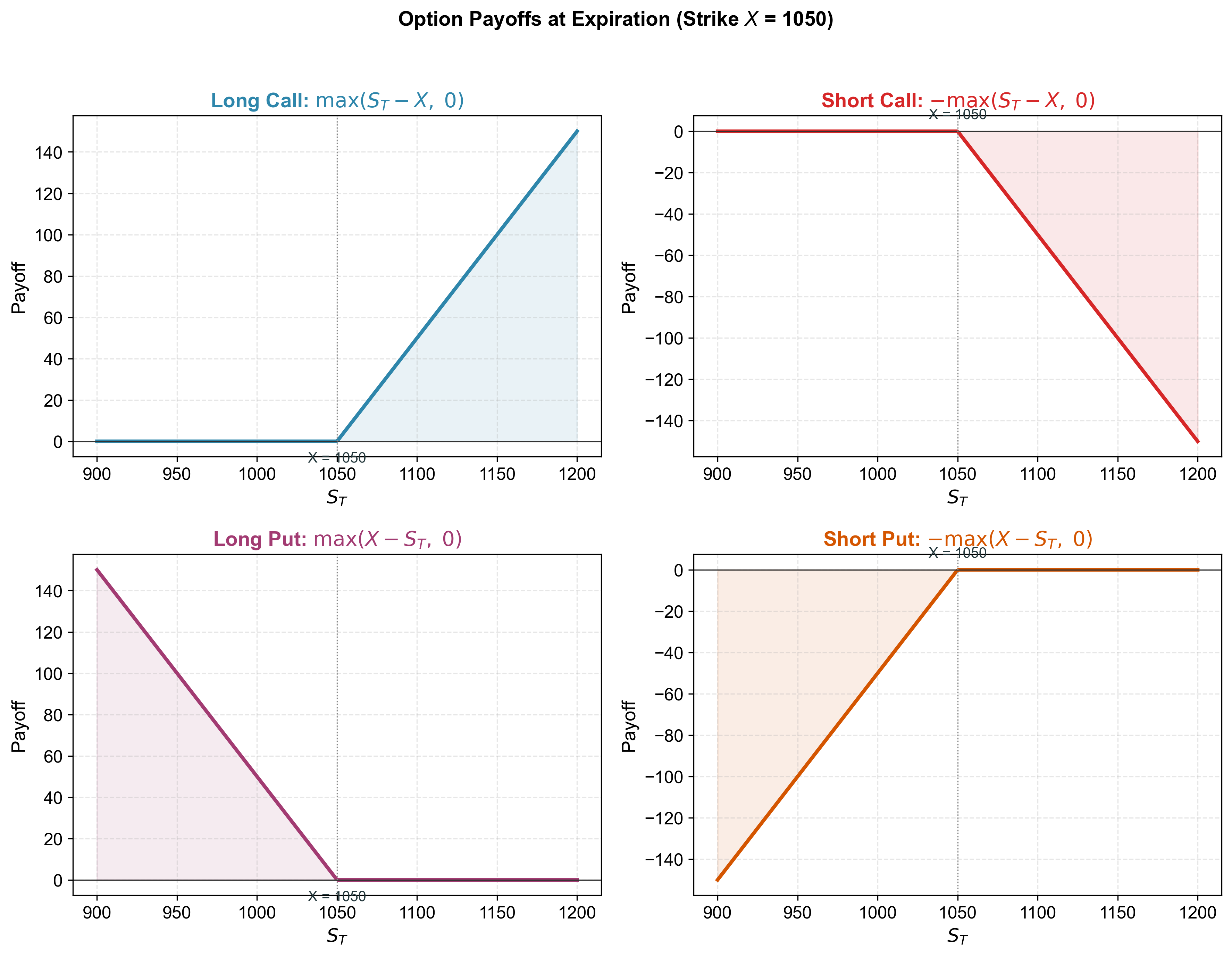

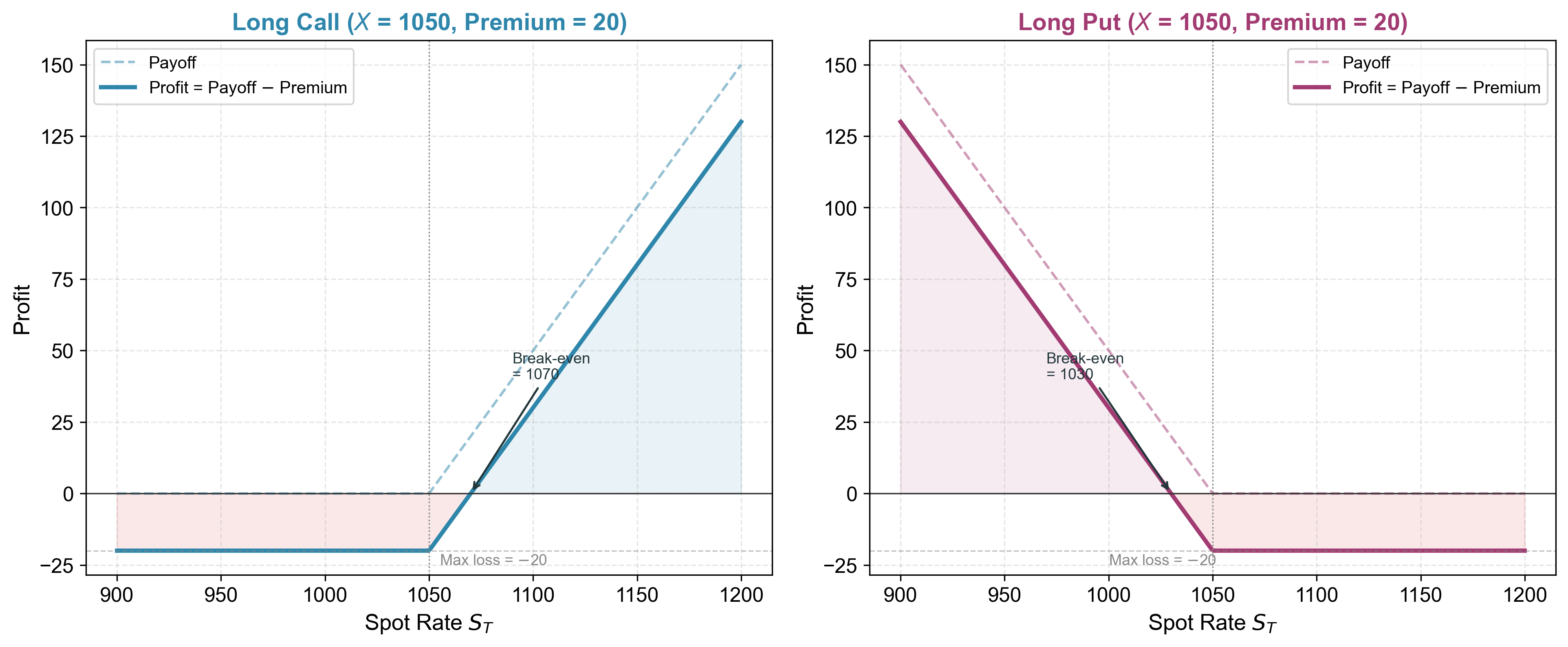

Payoff diagrams: visualizing option positions at expiration

FX options: conventions, intrinsic value, and key price drivers

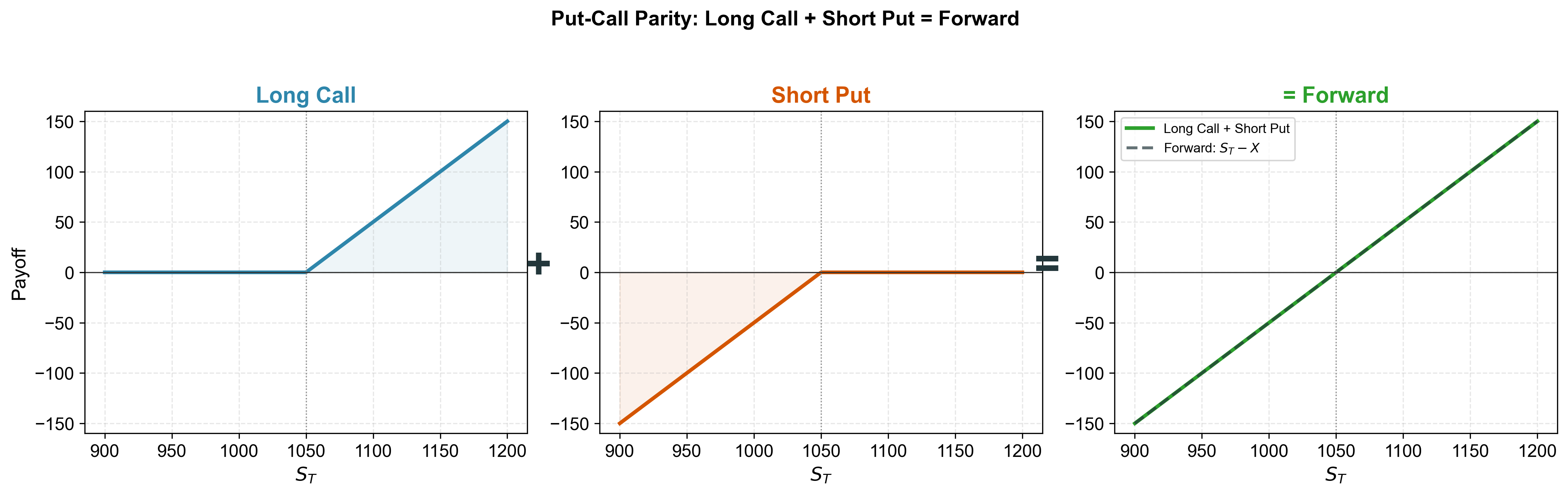

Put-call parity: the fundamental link between calls, puts, and forwards

Binomial option pricing: one period, multi-period, and convergence to Garman-Kohlhagen

This primer provides the pricing background used in Lecture 8 (Nonlinear Exposure and FX Options).

This is a technical primer. Lecture 8 focuses on why firms need options and how to use them strategically. This primer covers the mechanics: what options are, how their payoffs work, and how they are priced using no-arbitrage arguments.

FX option = right to exchange currencies

An FX option gives the right to exchange one currency for another at a fixed rate.

Convention: An FX option is simultaneously a call on one currency and a put on the other.

Example: A EUR call with \(X = 1.10\) USD/EUR gives the right to buy EUR 1 for USD 1.10.

Exercise if \(S_T > 1.10\) : buy EUR cheaply at 1.10 and sell at market rate \(S_T\)

Don’t exercise if \(S_T < 1.10\) : buy EUR at the cheaper market rate instead

The forward rate and option moneyness

For a European FX option, the payoff at maturity depends on the terminal spot rate \(S_T\) :

\[\text{Call: } \max(S_T - X,\, 0) \qquad \text{Put: } \max(X - S_T,\, 0)\]

Today, the no-arbitrage benchmark for maturity \(T\) is the forward rate (CIP):

\[F_{0,T} \;=\; S_0 \times \frac{1 + r}{1 + r^*}\]

Forward moneyness:

\(X < F_{0,T}\) : call is ITM forward ; put is OTM forward \(X = F_{0,T}\) : both are at-the-money forward (ATMF) \(X > F_{0,T}\) : call is OTM forward ; put is ITM forward

Key takeaway. The forward rate is the no-arbitrage anchor for option moneyness. The terminal payoff still depends on \(S_T\) , not on \(F\) .

At-the-money forward and put-call parity

For European options with the same strike and expiry, put-call parity gives:

\[c - p \;=\; \frac{F_{0,T} - X}{1 + r}.\]

When \(X = F_{0,T}\) :

\[c - p \;=\; 0 \quad\Longrightarrow\quad c = p.\]

This is why the at-the-money forward (ATMF) strike is the natural reference: call and put have the same price, and the forward is the no-arbitrage anchor. The full derivation appears in the next section.

The expressions \(\max(F - X, 0)\) and \(\max(X - F, 0)\) are sometimes called “forward intrinsic value” or “forward moneyness.” They are useful classification labels, not exercise values for European options (which can only be exercised at \(T\) , against \(S_T\) ). Present-value lower bounds on European option prices are \(c \geq \max(F_{0,T} - X, 0)/(1+r)\) and \(p \geq \max(X - F_{0,T}, 0)/(1+r)\) , i.e., the forward moneyness discounted to today.

Factors affecting option prices

Five key inputs determine option value (table holds the forward \(F\) fixed when varying \(r\) ):

Forward \(F\) \(\uparrow\)

\(\uparrow\) \(\downarrow\) Higher expected terminal rate

Strike \(X\) \(\uparrow\)

\(\downarrow\) \(\uparrow\) Harder/easier to exercise

Volatility \(\sigma\) \(\uparrow\)

\(\uparrow\) \(\uparrow\) More chance of large moves

Time to expiry \(T\) \(\uparrow\)

\(\uparrow\) \(\uparrow\) (\(^*\) )More time for favorable moves

Domestic rate \(r\) \(\uparrow\) (holding \(F\) fixed)

\(\downarrow\) \(\downarrow\) Future payoffs discounted more heavily

\(^*\) Generally true for plain European options; can be affected by rates/carry in edge cases.

Note. If spot \(S_0\) and \(r^*\) are held fixed instead, a higher domestic rate raises the forward \(F\) , which tends to raise calls and lower puts . The table separates this forward effect from pure discounting.

Volatility is the most important input — it measures how much the exchange rate might move. Higher volatility \(\Rightarrow\) more “upside” for the option buyer \(\Rightarrow\) higher price.

The fundamental link

For European options with the same strike and expiry:

\[\boxed{c - p = \frac{F - X}{1 + r}}\]

where \(c\) = call price, \(p\) = put price, \(F\) = forward rate, \(X\) = strike, \(r\) = domestic interest rate.

This is a no-arbitrage relationship, not a model — it holds regardless of what pricing model you use.

Put-call parity links calls, puts, and forwards. It is model-free because it relies only on the absence of arbitrage. If it were violated, you could construct a riskless profit by trading the three instruments.

Proof by replication

Consider two portfolios at time 0:

Portfolio A: Long call + invest \(\frac{X}{1+r}\) in domestic bonds

Portfolio B: Long put + long forward at rate \(F\) + invest \(\frac{F}{1+r}\) in domestic bonds

At expiration \(T\) :

\(S_T > X\) \((S_T - X) + X = S_T\) \(0 + (S_T - F) + F = S_T\)

\(S_T \leq X\) \(0 + X = X\) \((X - S_T) + (S_T - F) + F = X\)

Both give \(\max(S_T, X)\) at \(T\) . Same payoff \(\Rightarrow\) same price today:

\[c + \frac{X}{1+r} = p + 0 + \frac{F}{1+r} \quad \Rightarrow \quad c - p = \frac{F - X}{1+r}\]

Visual: long call + short put = forward

Key implication: A forward is just a combination of a call and a put at the same strike.

At strike \(X = F\) : the call and put have equal value (\(c = p\) ).

Numerical example

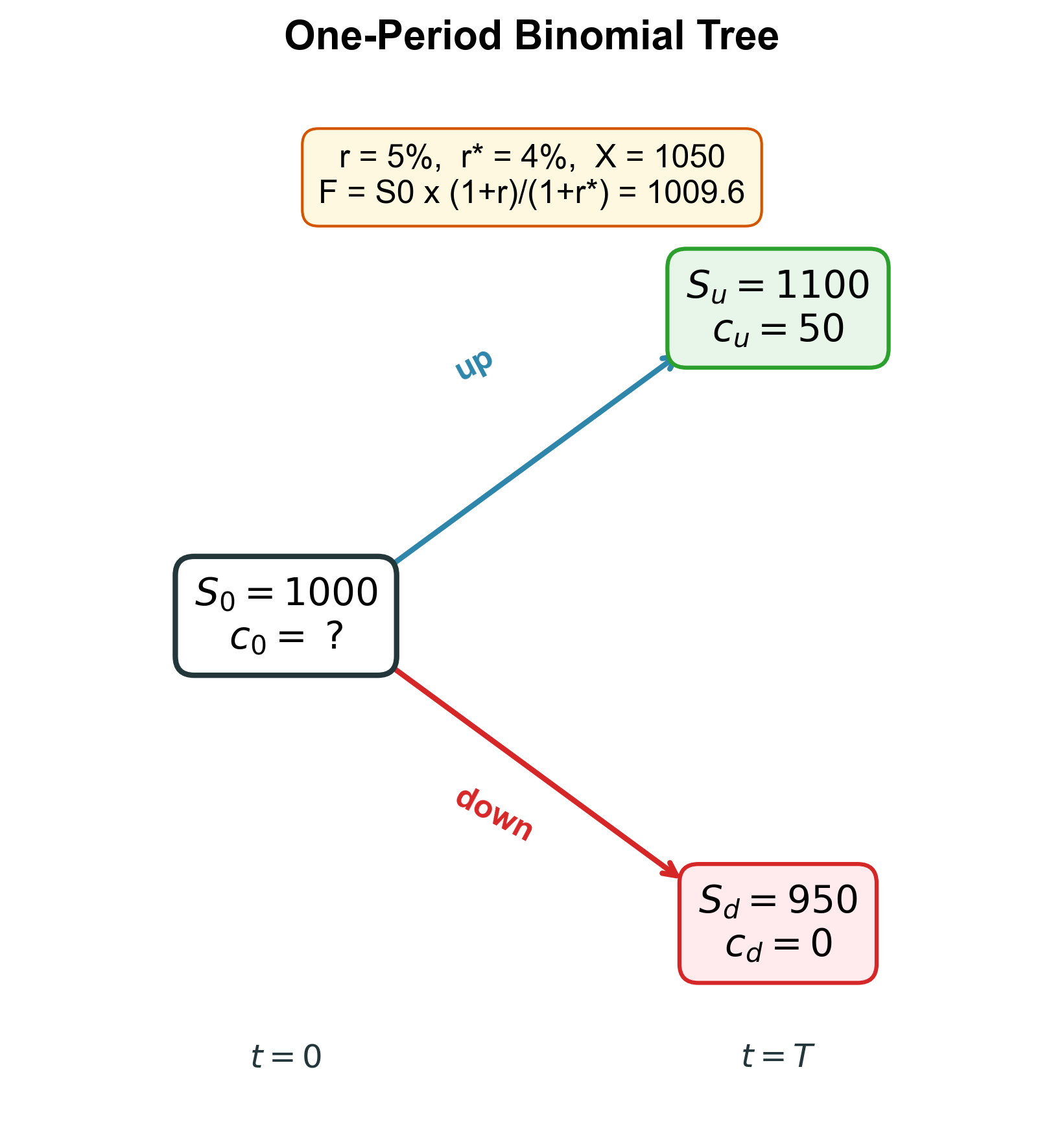

Setup: \(S_0 = 1000\) , \(r = 5\%\) , \(r^* = 4\%\) , \(X = 1050\)

Forward rate: \(F = 1000 \times \frac{1.05}{1.04} \approx 1009.6\)

Put-call parity: \(c - p = \frac{F - X}{1 + r} = \frac{1009.6 - 1050}{1.05} = \frac{-40.4}{1.05} = -38.5\)

So \(c = p - 38.5\) . The call is cheaper than the put because the strike is above the forward.

If someone quotes you \(p = 60\) , then \(c = 60 - 38.5 = 21.5\)

If you know the call price, you get the put price for free (and vice versa)

One-Period Binomial Model

Setup

Two possible states at \(T\) : the exchange rate goes up to \(S_u\) or down to \(S_d\) .

The call has known payoffs: \(c_u = \max(S_u - X, 0)\) and \(c_d = \max(S_d - X, 0)\) .

Question: What is the fair price \(c_0\) today?

The replication idea

Key insight: We can replicate the option payoff using two instruments:

\(\Delta\) units of a forward contract (costs nothing to enter)

\(B\) dollars invested in a domestic bond (earns \(r\) )

Replicating portfolio payoffs at \(T\) :

Two equations, two unknowns. Solve for \(\Delta\) and \(B\) .

Solving for the option price

Subtract down from up:

\[\Delta(S_u - S_d) = c_u - c_d \quad \Rightarrow \quad \boxed{\Delta = \frac{c_u - c_d}{S_u - S_d}}\]

\(\Delta\) is the hedge ratio — how many forwards replicate the option.

From the down-state equation:

\[B = \frac{c_d - \Delta(S_d - F)}{1 + r}\]

Option price = cost of replicating portfolio = \(B\) (forward is free to enter)

\[\boxed{c_0 = B = \frac{c_d - \Delta(S_d - F)}{1 + r}}\]

No probabilities needed!

Notice: we never used the probability of up vs. down.

The option price comes purely from no-arbitrage — if the option is mispriced relative to the replicating portfolio , there is a riskless profit

Different investors can disagree about probabilities and still agree on the price

This is the power of replication : price by matching payoffs, not by forecasting

This is the same logic behind CIP (Lecture 4) and forward pricing:

Risk-neutral pricing

An equivalent and often more convenient approach. Define:

\[\boxed{q = \frac{F - S_d}{S_u - S_d}}\]

Then the option price can be written as:

\[c_0 = \frac{q \cdot c_u + (1 - q) \cdot c_d}{1 + r}\]

\(q\) is the risk-neutral probability — it makes the expected rate equal to the forward

Not a real-world probability — it’s the probability that is consistent with no-arbitrage pricing

Equivalent to the replication approach, but often faster to compute

Numerical example

Setup: \(S_0 = 1000\) , \(S_u = 1100\) , \(S_d = 950\) , \(r = 5\%\) , \(r^* = 4\%\) , \(X = 1050\)

\(F = 1000 \times \frac{1.05}{1.04} \approx 1009.6\) , \(\quad c_u = 50\) , \(\quad c_d = 0\)

Delta: \(\Delta = \frac{50 - 0}{1100 - 950} = \frac{50}{150} = \frac{1}{3}\)

Bond: \(B = \frac{0 - \frac{1}{3}(950 - 1009.6)}{1.05} = \frac{0 + 19.87}{1.05} = 18.92\)

Option price: \(c_0 = B = 18.92\)

Check with risk-neutral pricing:

\(q = \frac{1009.6 - 950}{1100 - 950} = \frac{59.6}{150} = 0.397\)

\(c_0 = \frac{0.397 \times 50 + 0.603 \times 0}{1.05} = \frac{19.87}{1.05} = 18.92\) \(\checkmark\)

Multi-Period Binomial Model

From one period to two

The tree recombines: an up move followed by a down move gives the same node as down-then-up. This is critical for computational efficiency — with N periods, we have N+1 terminal nodes instead of 2^N.

Working backwards

Backward induction: Start from the terminal payoffs and work backwards one period at a time.

At each node, apply the one-period formula with the same risk-neutral probability:

\[q = \frac{f_{\Delta t} - d}{u - d} \qquad \text{where } f_{\Delta t} = \frac{1 + r_{\Delta t}}{1 + r^*_{\Delta t}}\]

Step 1: Terminal payoffs — \(c = \max(S_T - X, 0)\) at each final node

Step 2: At each period-1 node: \(c = \frac{q \cdot c_u + (1-q) \cdot c_d}{1 + r_{\Delta t}}\)

Step 3: At the root: same formula using the period-1 values

Each backward step is just the one-period model applied locally.

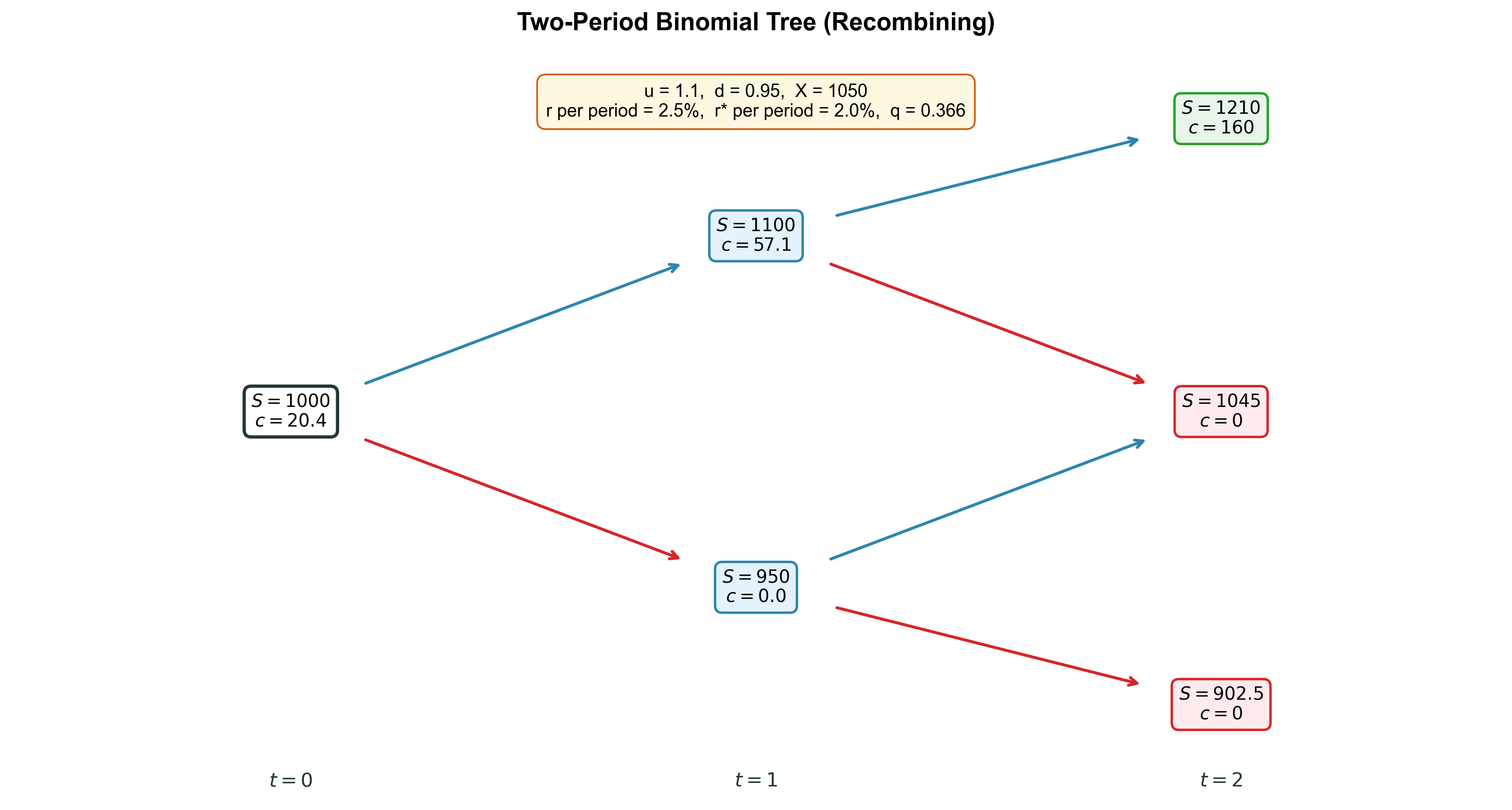

Two-period example

Using \(u = 1.10\) , \(d = 0.95\) , \(X = 1050\) , \(r_{\Delta t} = 2.5\%\) , \(r^*_{\Delta t} = 2.0\%\) :

Terminal payoffs:

\(S_{uu} = 1210\) : \(c_{uu} = \max(1210 - 1050, 0) = 160\)

\(S_{ud} = 1045\) : \(c_{ud} = \max(1045 - 1050, 0) = 0\)

\(S_{dd} = 902.5\) : \(c_{dd} = 0\)

Risk-neutral probability: \(q = \frac{1.025/1.02 - 0.95}{1.10 - 0.95} = \frac{0.0549}{0.15} = 0.366\)

Period 1 (up node): \(c_u = \frac{0.366 \times 160 + 0.634 \times 0}{1.025} = \frac{58.6}{1.025} = 57.1\)

Period 1 (down node): \(c_d = \frac{0.366 \times 0 + 0.634 \times 0}{1.025} = 0\)

Period 0: \(c_0 = \frac{0.366 \times 57.1 + 0.634 \times 0}{1.025} = \frac{20.9}{1.025} = 20.4\)

From 2 to N periods

The two-period model extends naturally:

Split the time horizon \(T\) into \(N\) equal periods of length \(\Delta t = T/N\)

Each period has up factor \(u\) and down factor \(d\)

Tree has \(N+1\) terminal nodes (recombining), backward induction from the end

Key question: How to choose \(u\) and \(d\) ?

Cox-Ross-Rubinstein (CRR) calibration:

\[\boxed{u = e^{\sigma\sqrt{\Delta t}}, \qquad d = \frac{1}{u} = e^{-\sigma\sqrt{\Delta t}}}\]

\(\sigma\) = annualized volatility of the exchange rate

As \(N\) increases, \(\Delta t \to 0\) and the binomial model produces finer and finer approximations

The tree structure ensures \(d = 1/u\) so the tree recombines

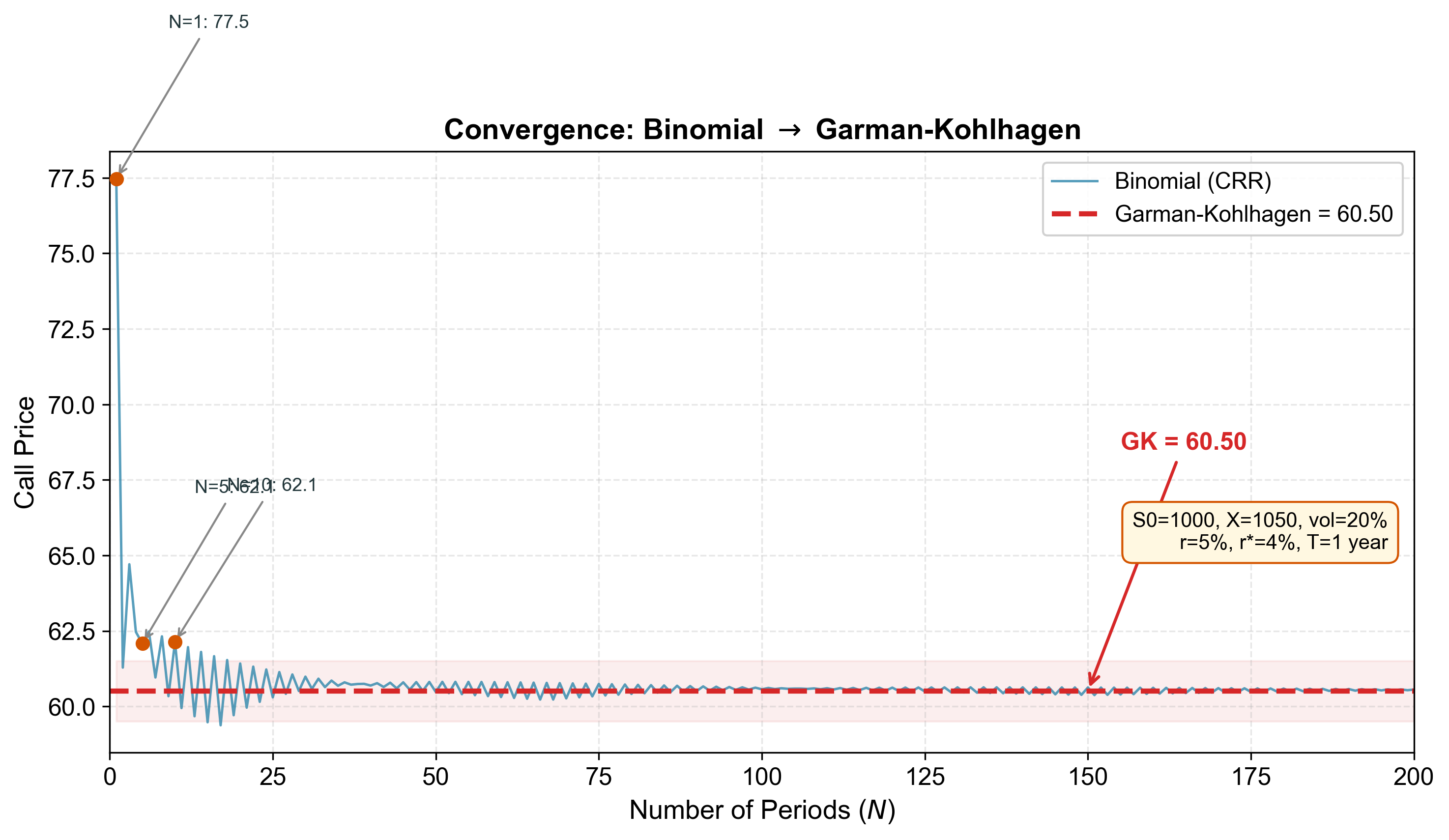

Convergence to Black-Scholes

Binomial \(\to\) Garman-Kohlhagen

The oscillating blue line is the binomial price as a function of the number of periods N. It converges rapidly to the GK price (red dashed line). The oscillation between odd and even N is typical of binomial models. By N=50 or so the price is very close to GK.

Summary

Options

Right, not obligation — buyer pays premium for asymmetric payoff

Payoffs

Kink at strike; four basic positions (long/short \(\times\) call/put)

FX conventions

EUR call = USD put; forward rate anchors ATMF and put-call parity

Put-call parity

\(c - p = (F-X)/(1+r)\) : model-free, links calls, puts, forwards

Binomial model

Replication + no-arbitrage \(\Rightarrow\) unique price without probabilities

Risk-neutral pricing

Probability \(q\) that makes expected return = forward; equivalent to replication

Multi-period

Backward induction; CRR calibration: \(u = e^{\sigma\sqrt{\Delta t}}\)

Convergence

Binomial \(\to\) Garman-Kohlhagen as \(N \to \infty\)

Next: Lecture 8 applies these tools to corporate hedging — option strategies, nonlinear exposure, and the information content of implied volatility.