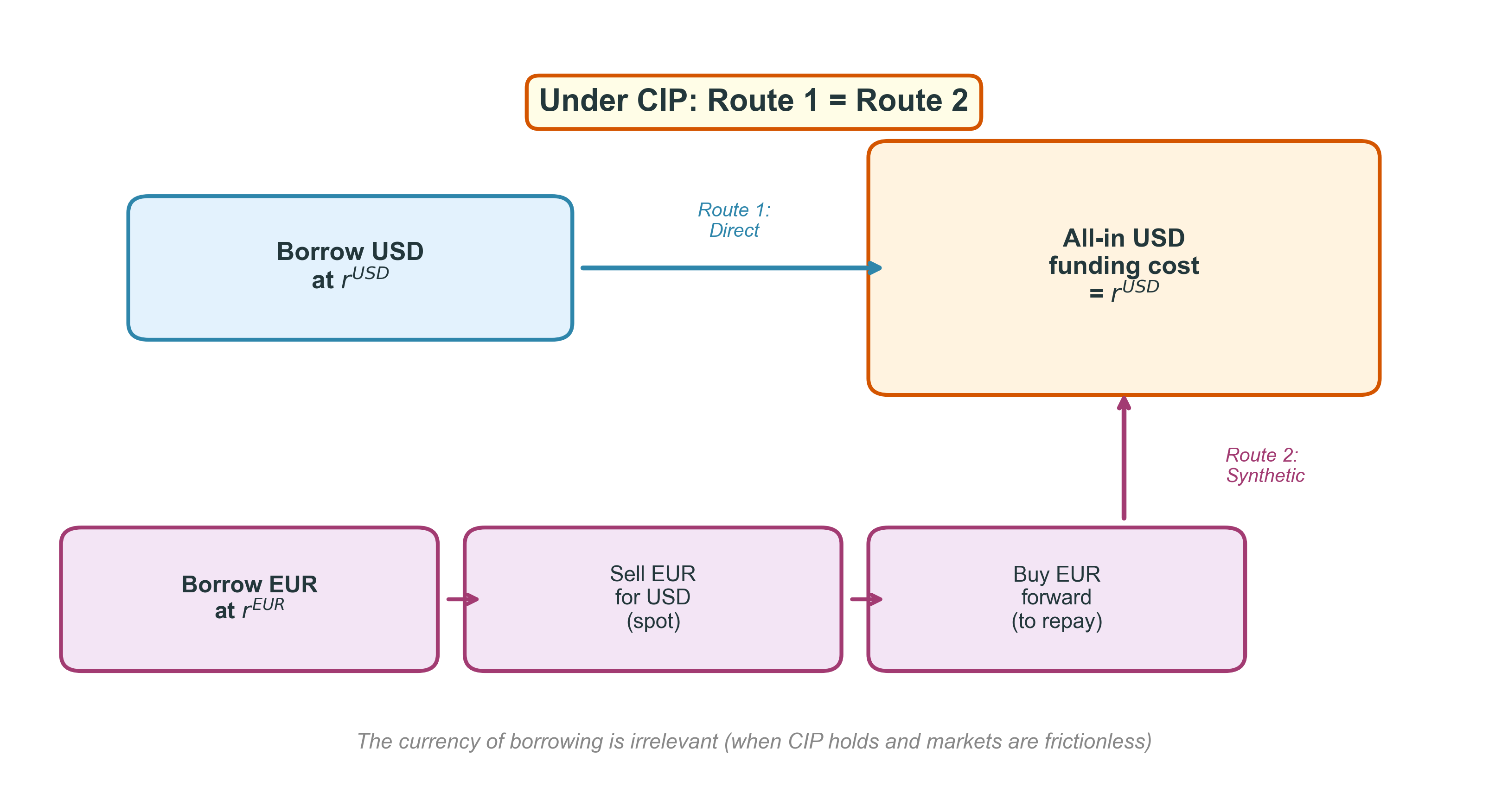

Negative basis: synthetic USD funding is more expensive than direct USD funding

Positive basis: synthetic USD funding is cheaper

When basis \(\neq 0\), Route 1 \(\neq\) Route 2. This is the same convention used in Lecture 4.

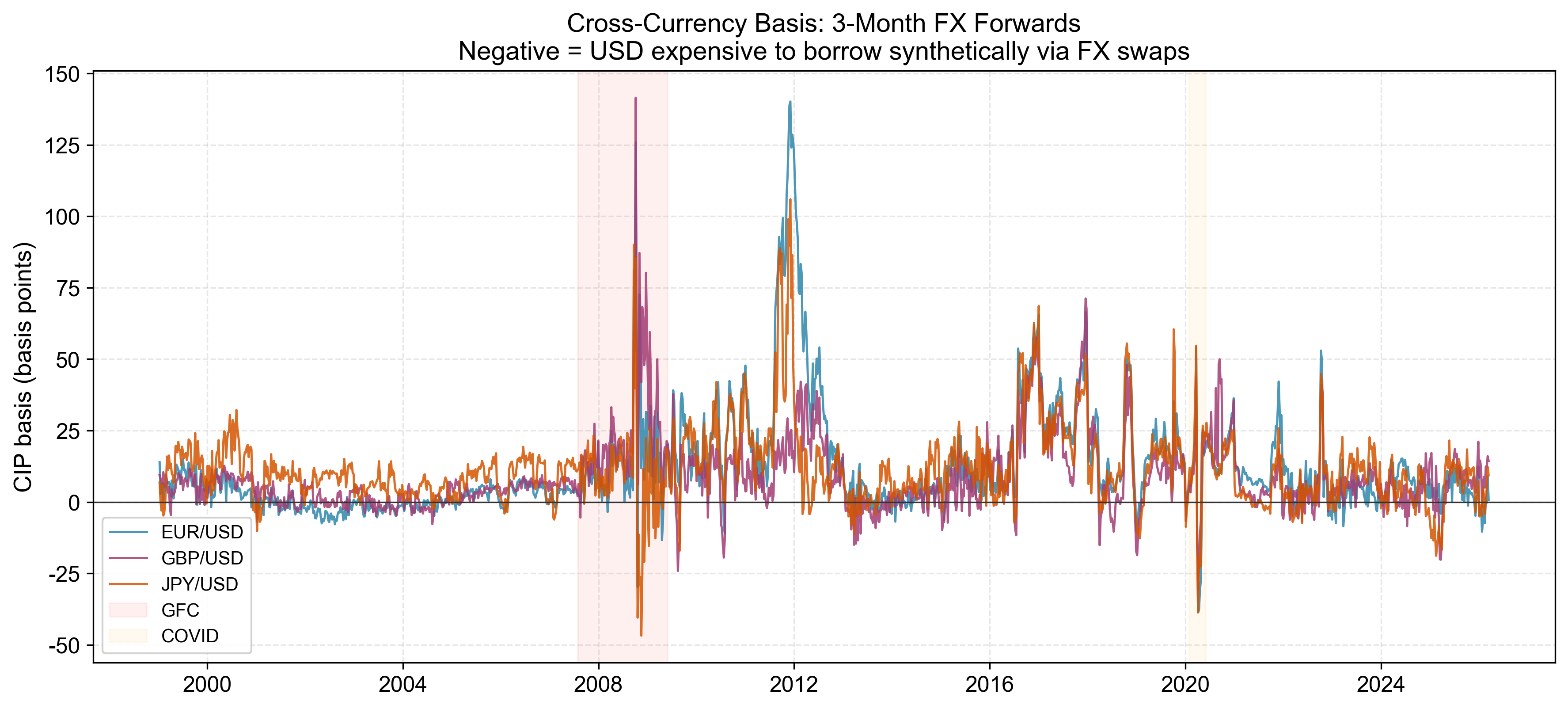

The basis in practice

3M FX-swap-implied USD basis for EUR, GBP, JPY. \(\text{basis} = r^{USD}_{\text{direct}} - r^{USD}_{\text{synthetic}}\) (negative \(=\) synthetic USD funding more expensive). Computed from spot, 3M forward points, and 3M deposit rates in SpotAndForward.xlsx; \(\tau = 0.25\).

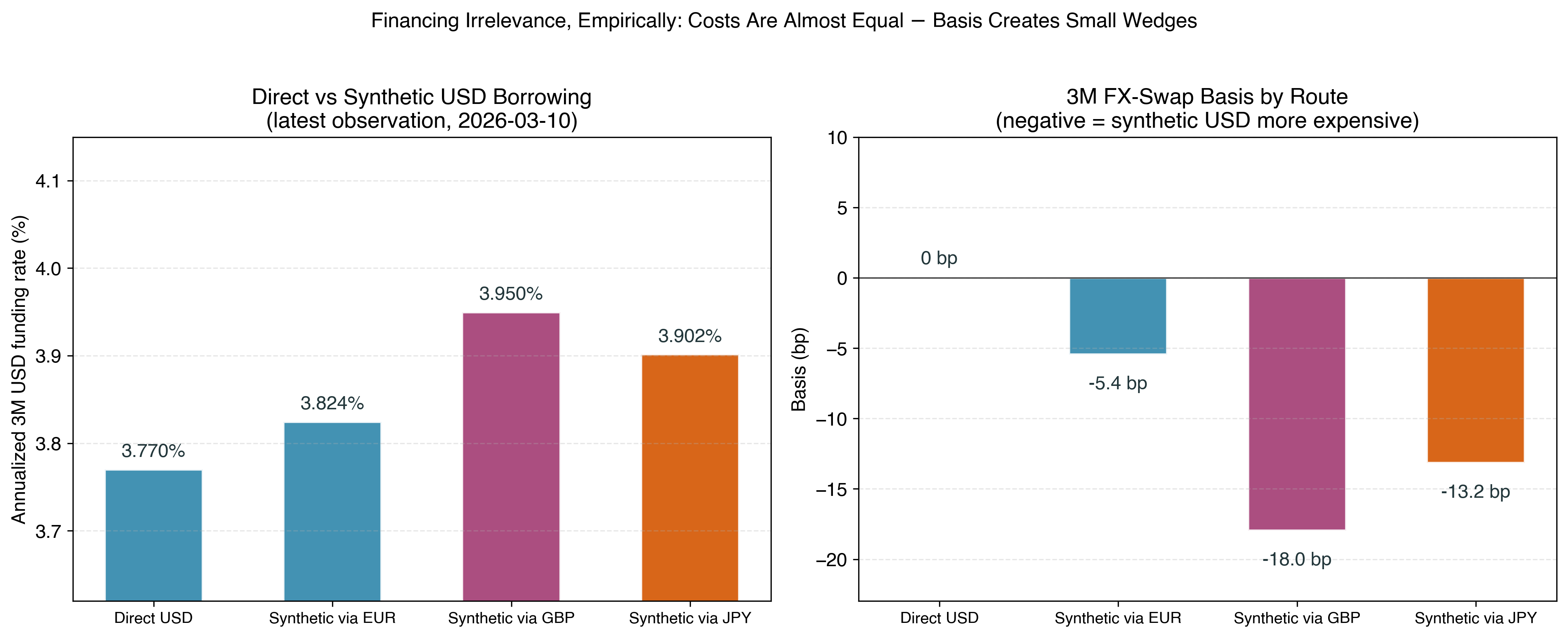

Synthetic USD borrowing: latest snapshot

Latest joint observation in SpotAndForward.xlsx (2026-03-10). The annualized 3M synthetic USD rate via foreign currency \(f\) is \(\;r^{USD}_{\text{synthetic}} = \bigl[(F/S)\,(1 + r_f\,\tau) - 1\bigr] / \tau,\;\) where \(r_f\) is the foreign money-market rate, \(F/S\) is the 3M forward conversion factor, and \(\tau = 0.25\) is the year fraction.

Friction 2: Tax asymmetries

Even when CIP holds, the tax treatment of the two routes may differ.

Interest payments on direct borrowing are tax-deductible in the borrower’s jurisdiction.

FX gains/losses on foreign-currency debt may be taxed differently from interest.

The forward contract in Route 2 may generate gains/losses taxed at a different rate or in a different period.

Tax asymmetries can arise because interest, FX gains/losses, and derivative gains/losses may differ in character, timing, source, or hedge-accounting / tax designation across jurisdictions. The exact treatment is jurisdiction- and instrument-specific.

Bottom line: after-tax financing costs can differ even when pre-tax CIP holds.

Friction 3: Natural hedging

If the firm has revenues in EUR, borrowing in EUR creates a natural hedge.

EUR revenues service EUR debt directly

May reduce the need for forward contracts or swaps, though residual mismatches in timing, amount, or certainty may still need hedging

Reduces transaction costs, basis risk, and counterparty exposure

This is an operational benefit, not a financial arbitrage.

The logic: Match the currency of your liabilities to the currency of your assets.

A European subsidiary generating EUR revenue should be funded in EUR

A US exporter with JPY receivables might borrow in JPY

Friction 4: Market access and comparative advantage

Firms may face different credit spreads in different markets.

Why?

Information advantage: Local banks know local firms better

Regulatory barriers: Some bond markets restrict foreign issuers

Investor base: US market is deepest; EUR market has grown rapidly

Name recognition: Known issuers get tighter spreads at home

If each firm borrows where it has an advantage and swaps into its desired currency, both can gain. This is the comparative advantage argument for swaps.

Summary: why financing currency matters

Friction

Mechanism

Cross-currency basis

CIP deviations create cost wedges

Tax asymmetries

Different tax treatment of interest vs. FX gains

Natural hedging

Currency matching reduces hedging needs

Market access

Comparative advantage in credit markets

Under pure CIP with no frictions: currency choice is irrelevant.

With real-world frictions: currency choice affects firm value.

Instruments for the Financing Decision

The corporate treasurer’s toolkit

The financing decision requires instruments that transform the currency and interest rate profile of debt.

Three key instruments:

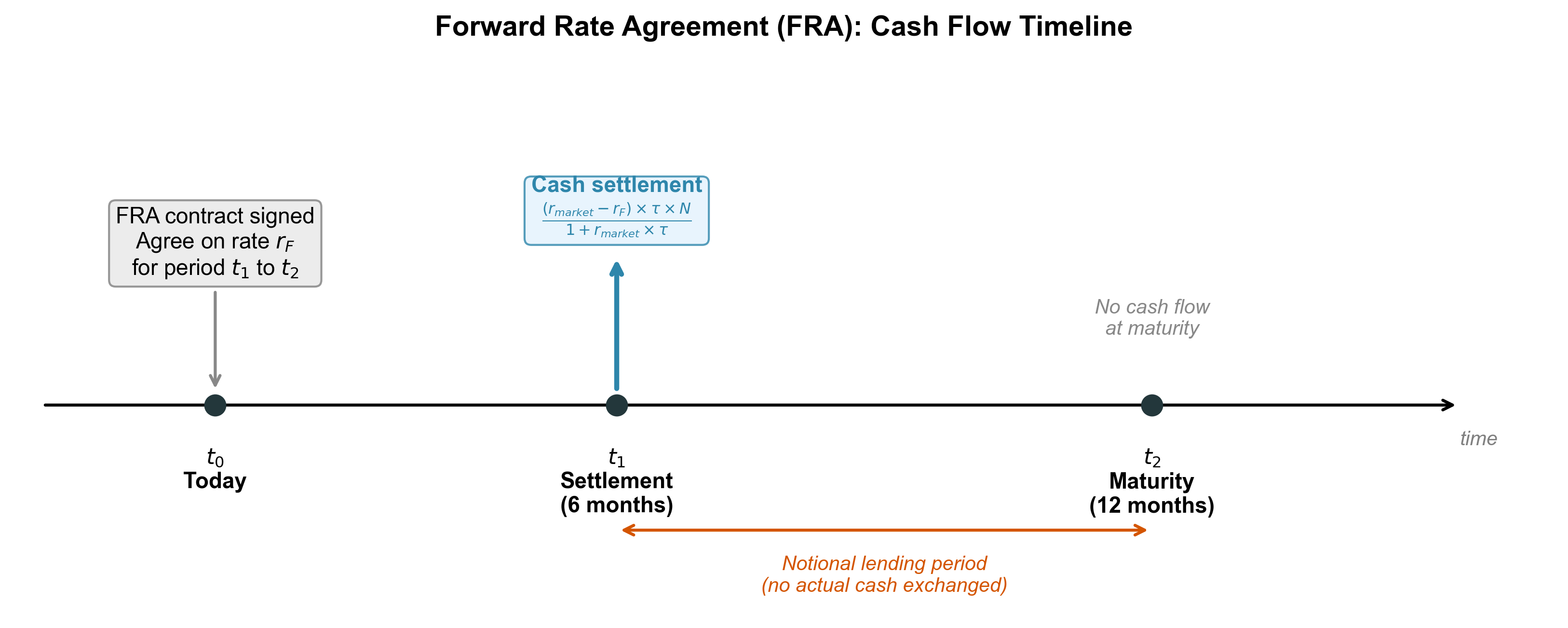

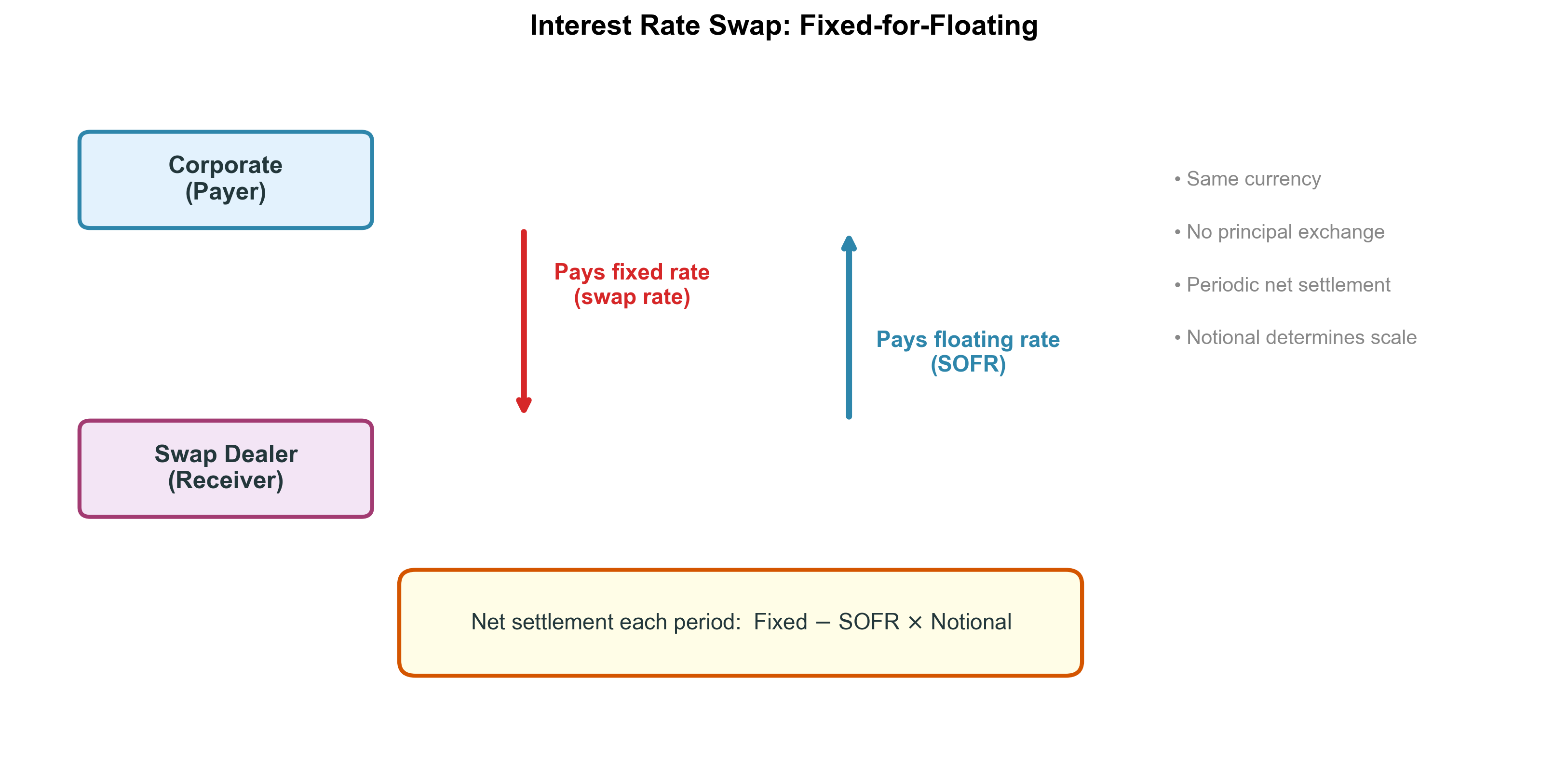

Forward Rate Agreements (FRAs): Lock in a future borrowing rate

If rates rise: fixed payer gains (locked in a lower rate; floating payments received increase)

If rates fall: fixed payer loses (locked in a higher rate; floating payments received decrease)

The mark-to-market value matters for:

Counterparty risk management (collateral calls)

Accounting (hedge effectiveness testing)

Unwinding the swap before maturity

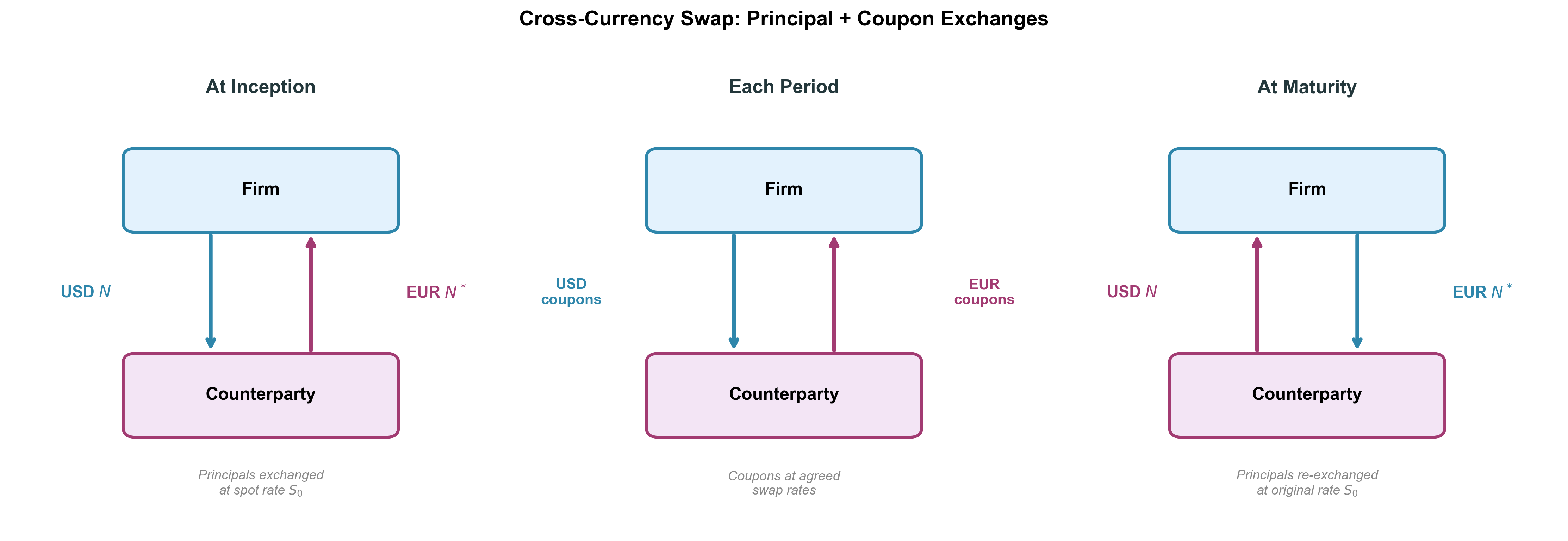

Cross-currency swaps

The problem: “We can borrow cheaply in EUR, but we need USD funding.”

A cross-currency swap (CCS) exchanges:

Principals in two currencies (at inception and maturity)

Periodic coupons in two currencies (during the life)

Key difference from IRS: Principal IS exchanged, because the currencies differ.

The same nominal principal amounts are exchanged at inception and re-exchanged at maturity using the original agreed exchange rate. This fixes the contractual principal cash flows, but it does not make the swap risk-free: its mark-to-market value still changes over time with exchange rates, interest rates, and the basis.

The Reverse Yankee setup later in the lecture uses exactly this framing: a US firm issues EUR debt, then uses a CCS to receive EUR coupons (servicing the EUR bond) and pay USD coupons (its desired liability).

CCS cash flows

CCS: where the basis enters

In a CCS, one (or both) legs trade at the local swap rate plus a basis spread that quotes the wedge from CIP. For a US firm that issues EUR debt and swaps the proceeds into USD (a Reverse Yankee), comparing the two routes as spreads over the USD risk-free rate:

Recall basis \(= r^{USD}_{\text{direct}} - r^{USD}_{\text{synthetic}}\), so a negative basis means synthetic USD is more expensive and raises the all-in cost.

Reverse Yankee savings require the EUR credit-spread advantage (and/or other market-access benefits) to outweigh any negative-basis cost.

The basis is not a free lunch: it is a price for intermediation and balance-sheet capacity.

This is why the basis is the primary friction in the financing decision.

CCS valuation over time

At inception: Value \(= 0\) (principals have equal market value; coupon streams are set to offset).

Over time, value changes with:

Spot exchange rate (affects the relative value of the two principal amounts)

Interest rates in both currencies (affects the PV of remaining coupons)

Basis (affects the relative value of the two legs)

CCS valuation: a numerical example

A US firm enters a CCS to pay USD 10M at 5% and receive EUR 8M at 3%, with spot \(S^{USD/EUR}_0 = 1.25\) (so EUR 8M \(\times\) 1.25 \(=\) USD 10M). The EUR receivable leg services the EUR bond the firm just issued.

Two years later: \(S^{USD/EUR} = 1.333\) (EUR has appreciated), EUR rates fall to 2%, USD rates fall to 4%.

Swap value to the firm \(\approx +\)USD 0.6M: EUR appreciation made the EUR-receivable leg more valuable in USD.

The IBM–World Bank swap (1981)

The birth of the modern swap market.

IBM had existing debt in CHF and DEM but wanted USD exposure; it had strong credit in European markets.

World Bank wanted CHF and DEM for its lending operations; it had already borrowed heavily there and investors wanted diversification.

The solution. World Bank issued new USD bonds. IBM and World Bank then swapped payment obligations: IBM paid USD coupons (on World Bank’s bonds); World Bank paid CHF/DEM coupons (on IBM’s bonds).

Both gained. Each borrowed where they had a comparative advantage, then swapped into the desired currency.

The Eurocurrency Market and the LIBOR \(\to\) SOFR Transition

The Eurocurrency market

Definition: Deposits and loans denominated in a currency outside its home country.

Eurodollars: USD deposits outside the US (e.g., in London)

Euroyen: JPY deposits outside Japan

“Euro” in Eurocurrency\(\neq\) the EUR currency

Why it grew. Historically, offshore deposits often faced lighter reserve, deposit-insurance, and regulatory burdens than comparable domestic deposits, with large transactions between high-grade counterparties. Cold-War origins: Soviet USD holdings kept in London to avoid US seizure.

The Eurocurrency market was historically central to offshore interbank funding and LIBOR-style benchmarks. Today, USD reference rates such as SOFR are based on secured overnight repo transactions, not Eurodollar deposits.

From LIBOR to SOFR

LIBOR (London Interbank Offered Rate) was the dominant benchmark for decades.

Panel of banks submitted estimates of their borrowing costs

Published daily for multiple currencies and tenors

Referenced in trillions of dollars of contracts (swaps, FRAs, loans, mortgages)

What went wrong:

The underlying market (unsecured interbank lending) shrank after 2008

Banks were increasingly guessing, not reporting actual transactions

Manipulation scandal (2012): traders colluded to move LIBOR for profit

SOFR is an overnight rate computed from actual Treasury repo transactions (>USD 1T notional daily).

Term SOFR (1M, 3M, 6M, 12M) is a separate, forward-looking benchmark derived from SOFR futures, administered by CME Group. Term SOFR is widely used in fixed-tenor cash products, especially many business loans.

Transition. New use of USD LIBOR largely stopped after 2021; the remaining USD LIBOR panel settings ceased after 30 June 2023 (some synthetic legacy settings continued temporarily for legacy contracts only). Replacements: SOFR (USD), SONIA (GBP), €STR (EUR), TONA (JPY).

LIBOR vs SOFR at a glance

Feature

LIBOR

SOFR

Basis

Survey (expert judgment)

Transactions (Treasury repo, >USD 1T daily)

Security

Unsecured (interbank)

Secured (Treasury collateral)

Native tenor

Overnight to 12 months

Overnight (term rates built from SOFR futures)

Credit component

Yes (bank credit risk)

No (effectively risk-free)

Manipulation risk

High (small panel)

Low (massive volume)

What changed for corporate treasurers

USD products now reference SOFR, but the SOFR variant differs by product: many loans use Term SOFR or daily simple SOFR; derivatives and floating-rate notes commonly use overnight or compounded SOFR.

FRAs and swaps reference SOFR — mechanics unchanged, benchmark different.

No credit component in SOFR. In bank-credit stress, SOFR need not spike like LIBOR because it is secured by Treasury collateral; it can behave differently depending on repo-market conditions and flight-to-quality dynamics.

Term structure. LIBOR had built-in term rates (3M, 6M). SOFR is overnight — term rates are constructed (CME Term SOFR).

For this course: the instruments we’ve discussed (FRAs, IRS, CCS) work identically with SOFR. The economics are unchanged; only the reference rate is different.

Putting It Together: The Reverse Yankee Trade

Why are US firms borrowing in EUR?

By May 2025, US corporate Reverse Yankee issuance had reached about EUR 42B, a very strong year-to-date pace. Full-year rankings depend on issuer universe and data source.

Why would a US firm with USD costs borrow in EUR?

The setup: A US firm needs USD 1 billion for 5 years.

Three routes:

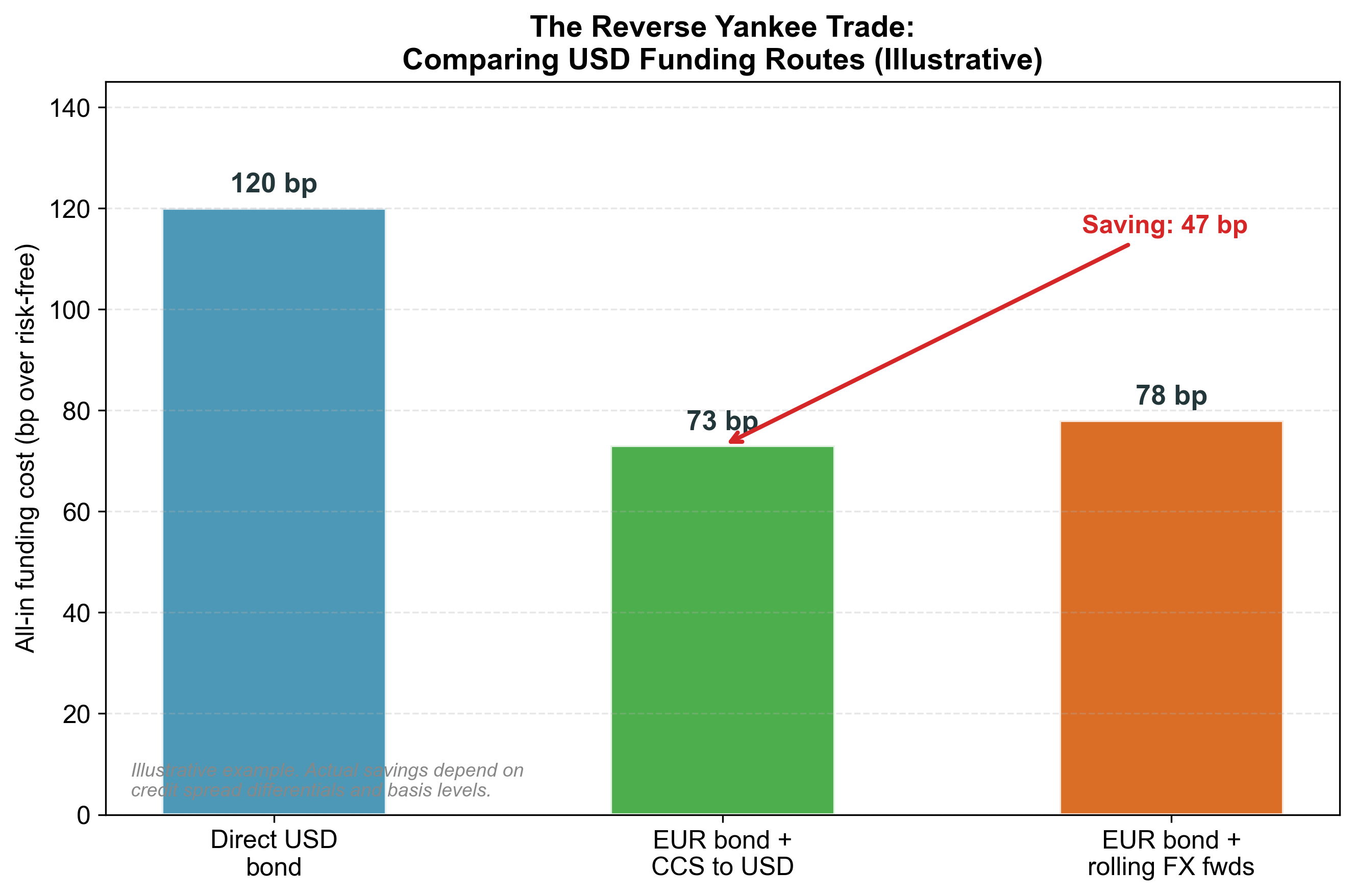

Issue USD bonds directly

Issue EUR bonds + enter a cross-currency swap to USD

Saving: \(120 - 97 = 23\) bp vs. direct USD issuance. On USD 1B that is USD 2.3M per year for 5 years \(\approx\) USD 11.5M over the life of the bond.

Under our convention, \(\text{basis} = r^{USD}_{\text{direct}} - r^{USD}_{\text{synthetic}}\). A negative basis means synthetic USD funding is more expensive and raises the all-in cost. The EUR credit-spread advantage (35 bp) more than offsets the 12 bp basis cost here.

The comparison

Illustrative numbers: USD direct \(=\) Treasury \(+\) 120 bp; EUR \(+\) CCS to USD \(=\) Treasury \(+\) 97 bp (saving 23 bp); EUR \(+\) rolling FX forwards \(=\) Treasury \(+\) 102 bp (saving 18 bp). Actual savings depend on credit spread differentials, basis levels, and balance-sheet / roll costs.

Why does this opportunity exist?

The Reverse Yankee trade is not a free lunch. It bundles several distinct, compensated risks:

Market access / spread differentials. EUR vs USD credit spreads for the same name can diverge, but this advantage is name-specific and can reverse.

Cross-currency basis. The USD basis is a price of intermediation, not a free arbitrage — it persists because of regulatory and balance-sheet costs.

Balance-sheet constraints. Banks that would arbitrage the basis face Basel III leverage and NSFR limits.

Counterparty risk. A 5-year CCS creates significant bilateral exposure (offset only partly by collateral).

Roll risk (Route 3). Rolling 3M FX forwards re-prices the basis every quarter.

The Reverse Yankee window

The window opened post-2014 because three conditions came together:

EUR rates fell toward (and below) zero — ECB rate cuts and quantitative easing.

The basis became more negative (more demand for USD funding, fewer arbitrageurs) — raising synthetic USD funding costs.

The US investment-grade credit market became relatively more expensive.

Recent strong issuance reflects the persistence of all three conditions.

Market context

Metric

Value

Source

FX daily turnover

USD 9.6T

BIS 2025

CCS notional (2024)

>USD 7T

Clarus 2024

CCS volume growth

+21% notional

Clarus 2024

Reverse Yankee issuance, 2025 YTD by May

EUR 42B

ECB/ING 2025

EUR/USD 3M basis (Mar 2026)

\(\approx\) –5 bp

SpotAndForward.xlsx

GBP/USD 3M basis (Mar 2026)

\(\approx\) –18 bp

SpotAndForward.xlsx

JPY/USD 3M basis (Mar 2026)

\(\approx\) –13 bp

SpotAndForward.xlsx

Japanese insurer FX hedge ratio

declined from \(\approx\) 60% to \(\approx\) 40%

BIS 2025

The swap and basis markets are among the largest and most active in global finance.

Internal Financing: A Brief Note

Moving cash within the multinational

Multinational firms also have internal mechanisms for moving funds across borders:

Intercompany loans: Parent lends to subsidiary (or vice versa)

Transfer pricing: Prices on intra-firm goods/services shift profits between jurisdictions

Royalties and management fees: Payments for IP or services between affiliates

Dividend policy: Timing and size of subsidiary-to-parent dividends

These tools serve financing, liquidity management, tax planning, and political-risk management, but they are constrained by transfer-pricing, withholding-tax, thin-capitalization, and anti-avoidance rules.

Full treatment is beyond this course, but corporate treasurers should know these mechanisms exist alongside external instruments.

Summary and Connections

Key takeaways

Financing irrelevance: Under CIP in frictionless markets, borrowing currency doesn’t matter. This is the financing analog of Modigliani–Miller for hedging.

Four frictions break irrelevance: Cross-currency basis (primary), tax asymmetries, natural hedging, and market access.

Instruments transform debt: FRAs lock in future rates, interest rate swaps convert fixed/floating, cross-currency swaps convert currencies. Each solves a specific corporate problem.

LIBOR is dead; SOFR lives: USD markets now use SOFR-based rates, but the exact convention differs by product — overnight or compounded SOFR for derivatives and FRNs, Term SOFR or daily simple SOFR for many loans.

The Reverse Yankee trade demonstrates how spread differentials, market access, and basis conditions jointly affect all-in funding costs for US corporates borrowing in EUR.

Connections to the course

Lecture 4 (CIP/Basis): The basis we introduced there now drives the financing decision. Same data, new application.

Lecture 6 (Why Hedge?): The MM-style irrelevance argument is identical in structure. Frictions break irrelevance; the question is always which frictions matter most.

Lecture 7 (Exposure): Natural hedging connects financing to exposure management. Currency matching is simultaneously a financing choice and a risk management strategy.

Looking ahead: The financing decision feeds directly into cross-border valuation (Lecture 10). The cost of capital depends on how the firm funds itself — and the basis affects that cost.