Main issues

Should a multinational firm hedge exchange rate exposure?

The Modigliani-Miller irrelevance benchmark

When does hedging increase firm value?

The Slite case: what happens when you don’t hedge

Empirical evidence on corporate hedging

The Risk Management Decision: Why Hedge?

Should a multinational firm hedge exchange rate exposure?

The Modigliani-Miller irrelevance benchmark

When does hedging increase firm value?

The Slite case: what happens when you don’t hedge

Empirical evidence on corporate hedging

The course now moves from macroeconomic context to the firm’s perspective.

The firm faces three interconnected decisions:

The hedging / risk management decision \(\leftarrow\) this lecture

The financing decision

The capital budgeting (investment) decision

Nominal exchange rates are volatile.

Changes in nominal exchange rates are not offset by changes in relative prices (PPP fails).

Hence, changes in the nominal exchange rate have real effects.

It is difficult to forecast future exchange rates (UIP/UEH fail).

Exchange rate risk premia exist — hedging is not “free.”

The firm cannot forecast its way out of exposure. Should it hedge?

Nominal and real exchange rates are volatile and difficult to predict.

If firms do not hedge, their future revenues and costs are more volatile and more difficult to predict.

Hence, designing hedging strategies that reduce the uncertainty of future revenues and costs should increase value…

…or shouldn’t it?

Setup:

Unhedged value today:

\[V_0^{UH} = \frac{\text{EUR } 500{,}000}{1 + 10\%} \times \frac{\text{USD}}{\text{EUR}} \; 1.10 = \text{USD } 500{,}000\]

Forward rate (from CIP):

\[F_{0,1} = S_0 \times \frac{1 + r^{USD}}{1 + r^{EUR}} = 1.10 \times \frac{1.05}{1.10} = 1.05\]

Hedged value today:

\[V_0^{H} = \text{EUR } 500{,}000 \times \frac{\text{USD}}{\text{EUR}} \; 1.05 \times \frac{1}{1 + 5\%} = \text{USD } 500{,}000\]

Hedging does not change the value!

This is not a coincidence — it is CIP at work. The forward rate adjusts so that hedged and unhedged positions have the same present value.

The value of the firm is independent of its hedging policy when:

There are no taxes

There are no transaction costs in financial markets

Shareholders and firms have the same information

Shareholders and firms have equal access to financial markets

There are no costs of financial distress

Under these conditions, hedging cannot add value.

Hedging is a purely financial decision.

Corporate managers cannot increase the value of the firm by undertaking financial transactions that shareholders can make themselves.

If a firm decides not to hedge an exposure that shareholders dislike, shareholders can hedge it personally (“home-made hedging”).

This shifts the hedging from the corporate level to the personal level, at no cost.

Same logic as capital structure irrelevance: financial policy doesn’t matter in frictionless markets.

\[\text{Value of firm} = \frac{E[\text{Cash Flows}]}{\text{Required Return}}\]

For hedging to increase firm value, it must:

Increase expected cash flows, and/or

Decrease the required return (discount rate)

Under MM, hedging does neither. The question becomes: which real-world frictions cause hedging to affect CFs or DR?

Hedging can increase firm value because:

Costs of financial distress — hedging reduces the probability and expected cost of distress

Tax convexity — hedging reduces expected tax liability when the tax function is convex

Agency costs — hedging reduces conflicts between managers, shareholders, and bondholders

Information asymmetries — “home-made” hedging is a poor substitute for corporate hedging

Financial distress = income insufficient to cover fixed obligations.

Direct costs: Liquidation, legal fees, courts.

Indirect costs (often larger):

Hedging reduces CF volatility \(\Rightarrow\) reduces probability of distress \(\Rightarrow\) reduces expected distress costs \(\Rightarrow\) increases firm value.

This is a cash flow effect: \(E[\text{CF}]\) rises because the probability-weighted cost of bad states falls.

Slite — a Swedish shipping company running ferries between Sweden and Finland.

Management confused the forward premium with the cost of hedging.

September 1992: Sweden abandons the link between SEK and DEM.

By end of 1992: SEK/DEM had depreciated by 30%.

Slite could no longer afford the ship.

The vessel was leased by a competitor (Silja).

Spring 1993: Slite went bankrupt.

Lesson: Without hedging, a single adverse FX move destroyed the firm. The bankruptcy costs — liquidation, loss of business, competitor advantage — are exactly the distress costs that justify hedging.

Progressive tax rates and loss limitations create a convex tax function:

With a convex tax function, expected taxes are higher with volatile income than with stable income (Jensen’s inequality):

\[E[\text{Tax}(\tilde{\Pi})] > \text{Tax}(E[\tilde{\Pi}])\]

Hedging smooths income \(\Rightarrow\) reduces expected tax liability \(\Rightarrow\) increases after-tax cash flows.

Setup:

Unhedged:

Hedged (\(F = 1.05\)): \(\Pi^{H} = 500\text{K} \times 1.05 - 525\text{K} = 0\)

Hedging increases value because the tax asymmetry penalizes volatility.

Manager vs. shareholder conflict:

Shareholder vs. bondholder conflict:

Both are primarily cash flow effects: better investment decisions, lower agency-driven costs.

M&M assumes shareholders can hedge themselves. But:

Shareholders have far less information about firm exposures than managers. Home-made hedging is imprecise.

Individuals face higher transaction costs, margin requirements, and short-sale constraints.

Economies of scale allow firms to obtain better terms for forwards and swaps than individual shareholders.

Forward positions may be prohibitively large for retail investors.

Home-made hedging is a poor substitute for corporate hedging.

This violates M&M’s “equal access to financial markets” assumption.

Expected cash flow effects (primary):

Discount rate effects (secondary):

The CF channel is primary. When evaluating whether a firm should hedge, first ask: “Does hedging change expected cash flows?”

Transaction costs: Bid-ask spreads on forwards, option premia, commissions

Cost of expertise: Risk management staff, systems, monitoring

Operational risk: Hedging errors, unauthorized trading, model risk

These costs must be weighed against the benefits. For most large firms with significant FX exposure, the benefits dominate.

Hedging operating exposure is difficult: Long-term, uncertain amounts, competitive effects are hard to capture with financial instruments

Bad incentives: Hedging programs can become speculative (“we’ll hedge only when we think the rate is going against us”)

Shareholder diversification: Some investors may prefer unhedged exposure for portfolio diversification purposes

Signaling: Hedging may signal to the market that the firm has significant exposure, drawing attention to risks

These are real concerns, but they argue for careful hedging, not for no hedging.

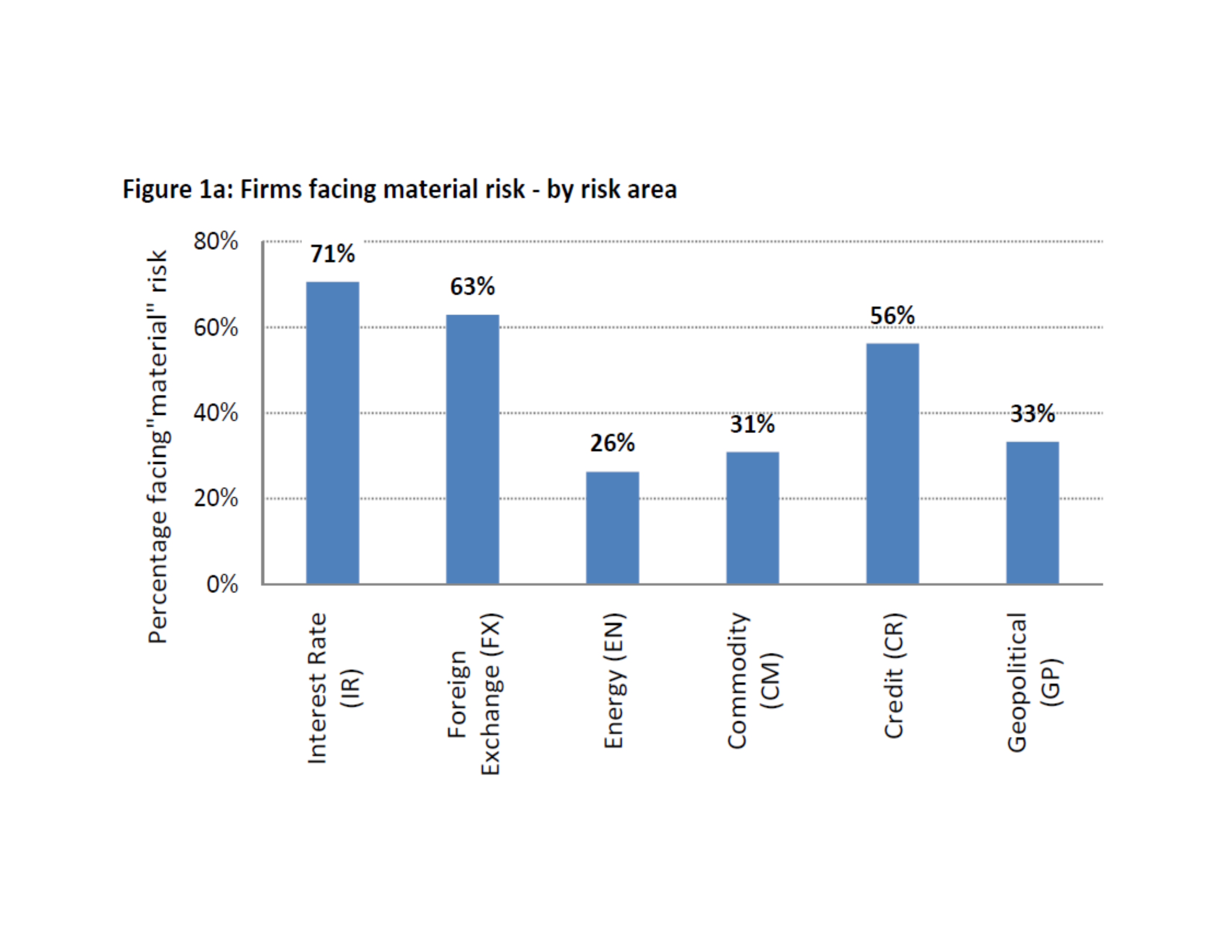

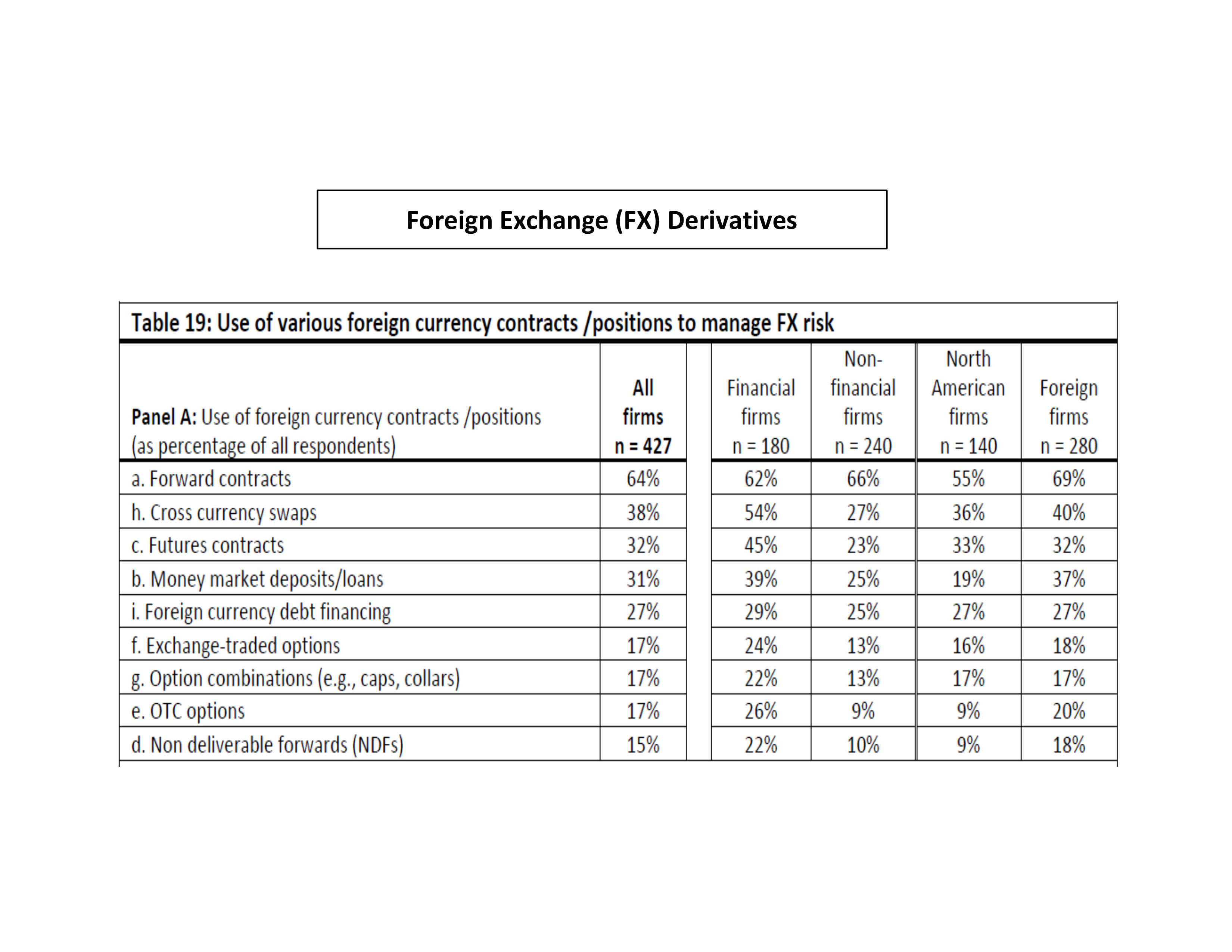

Source: “Managing Risk Management” by Bodnar, Graham, Harvey, and Marston (2011).

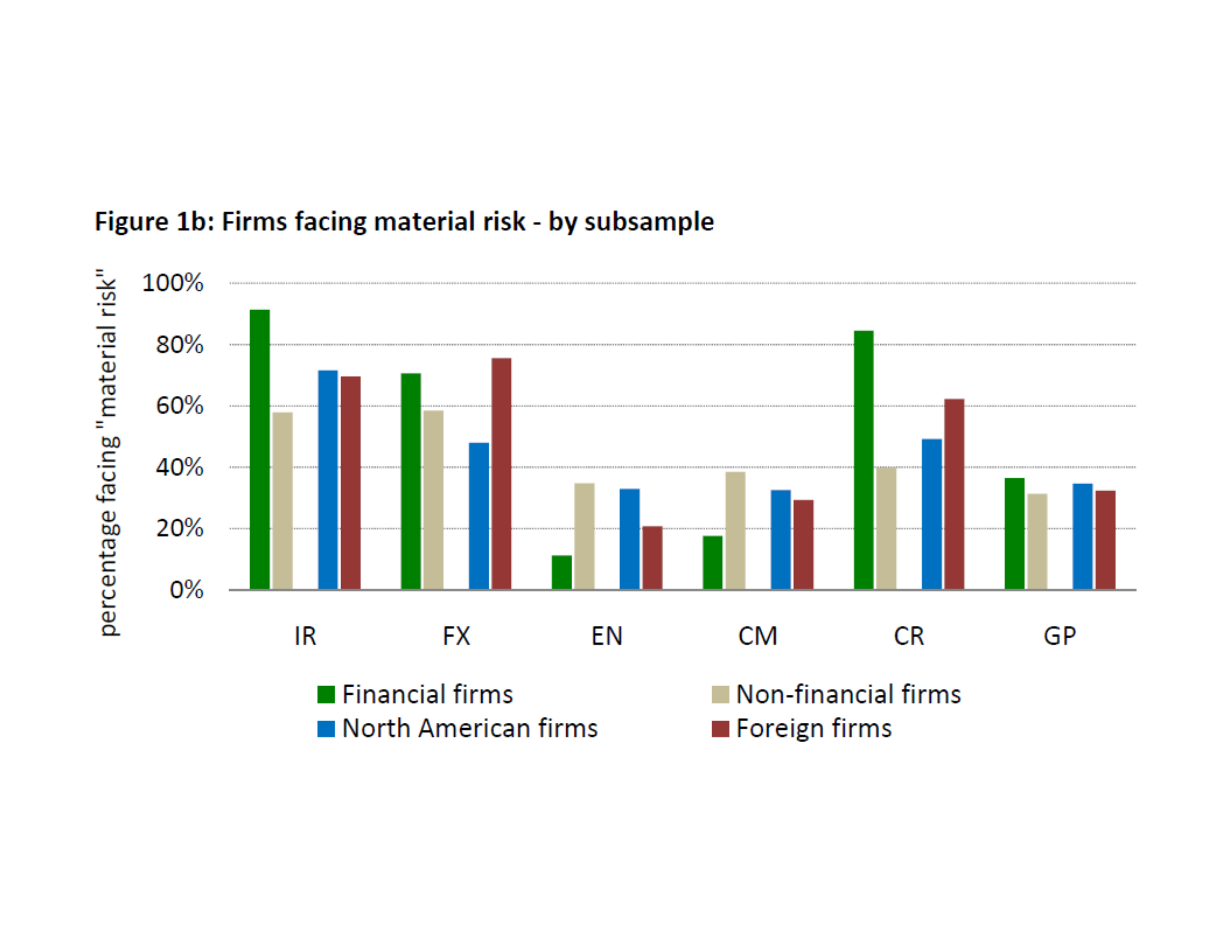

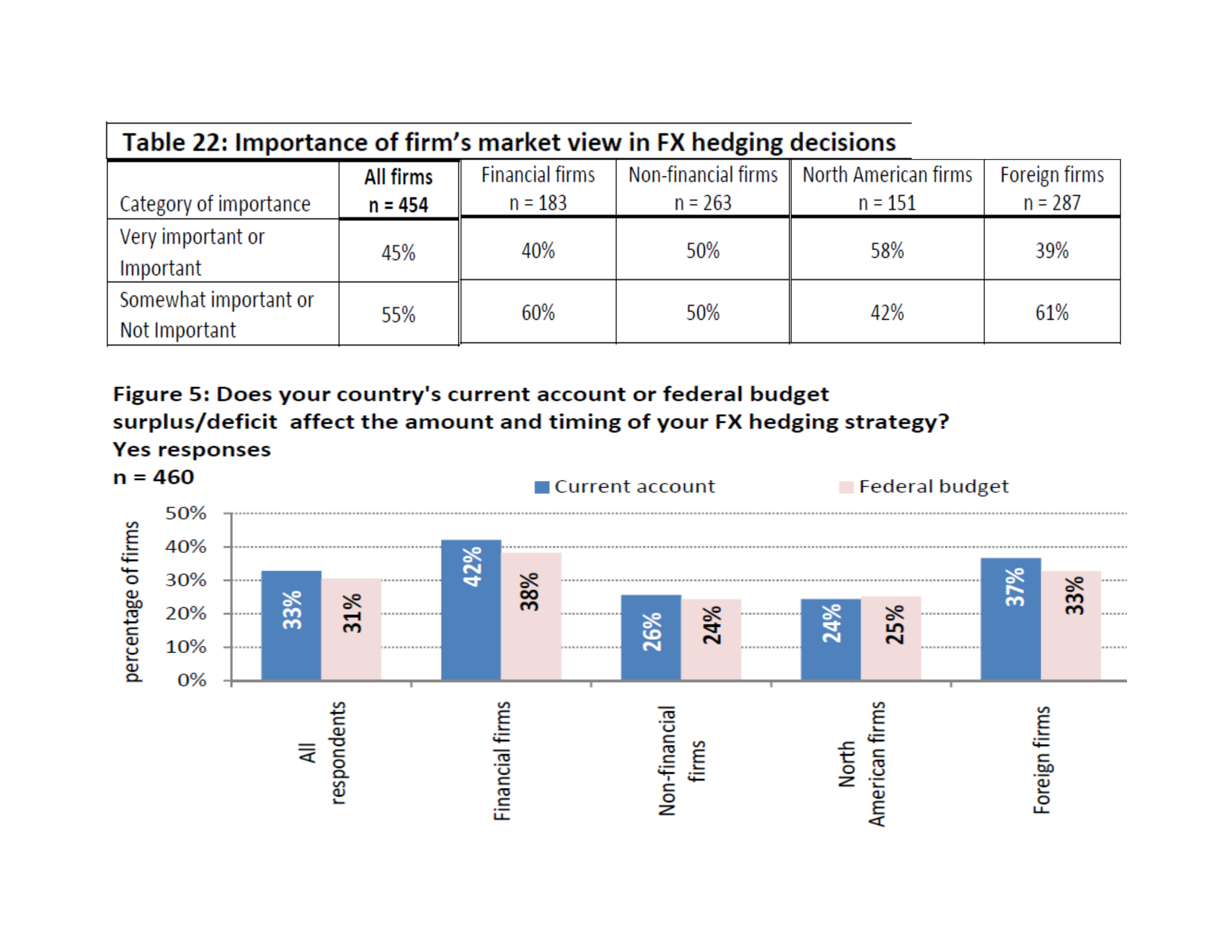

Source: Bodnar, Graham, Harvey, and Marston (2011).

Source: Bodnar, Graham, Harvey, and Marston (2011).

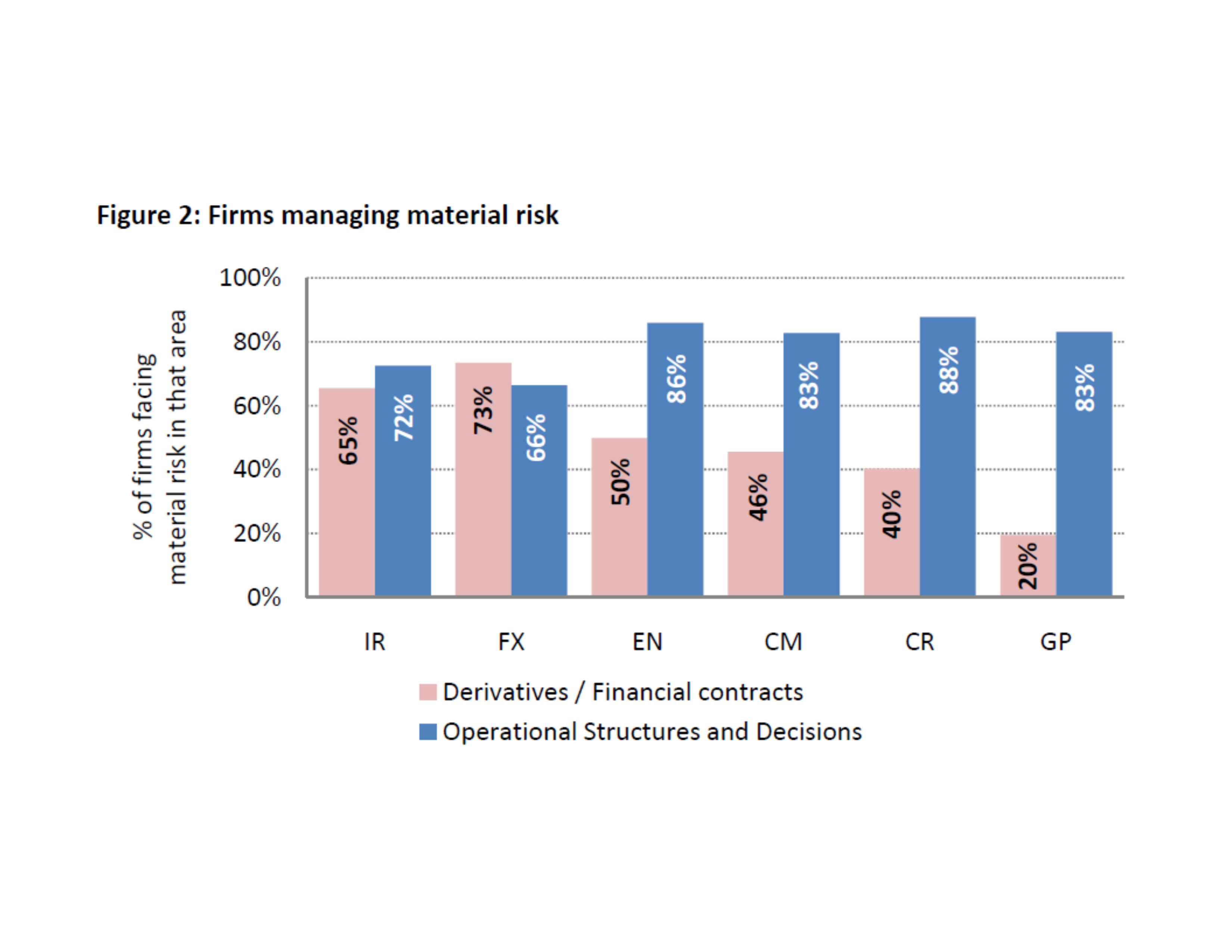

Source: Bodnar, Graham, Harvey, and Marston (2011).

Source: Bodnar, Graham, Harvey, and Marston (2011).

Under M&M, hedging does not affect firm value — shareholders can hedge themselves.

In reality, frictions make hedging valuable:

Hedging primarily increases \(E[\text{CF}]\) (and may reduce the discount rate).

The majority of firms hedge in practice. FX is the #1 risk managed with derivatives.

Next: How to measure exposure — transaction, translation, and operating — and how to design hedging strategies.