What UIP says: High interest rate currencies should depreciate to offset the interest rate advantage.

If UK rates are 2% higher than US rates, UIP predicts GBP will depreciate by approximately 2% against USD — so that investing in either currency earns the same expected return.

The Fama regression

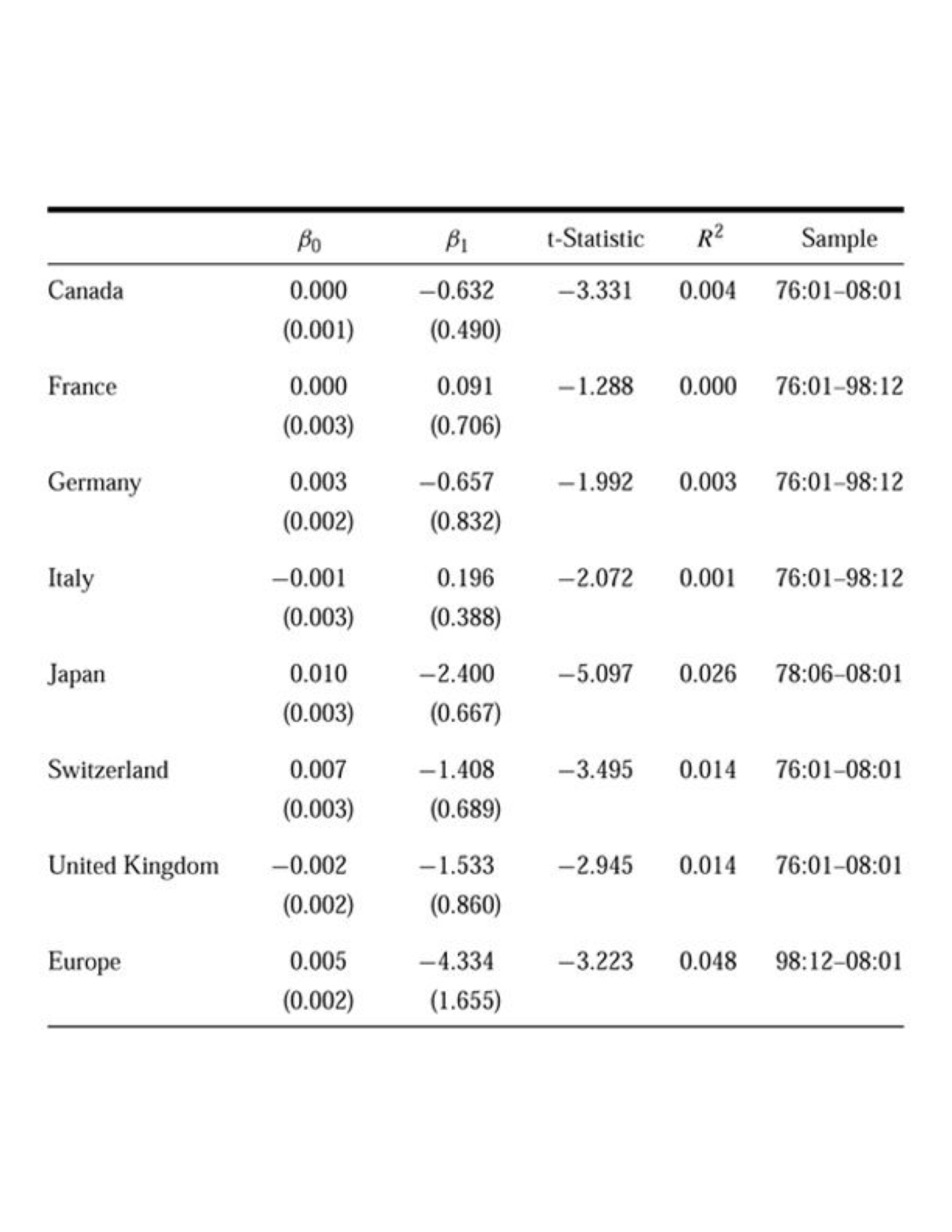

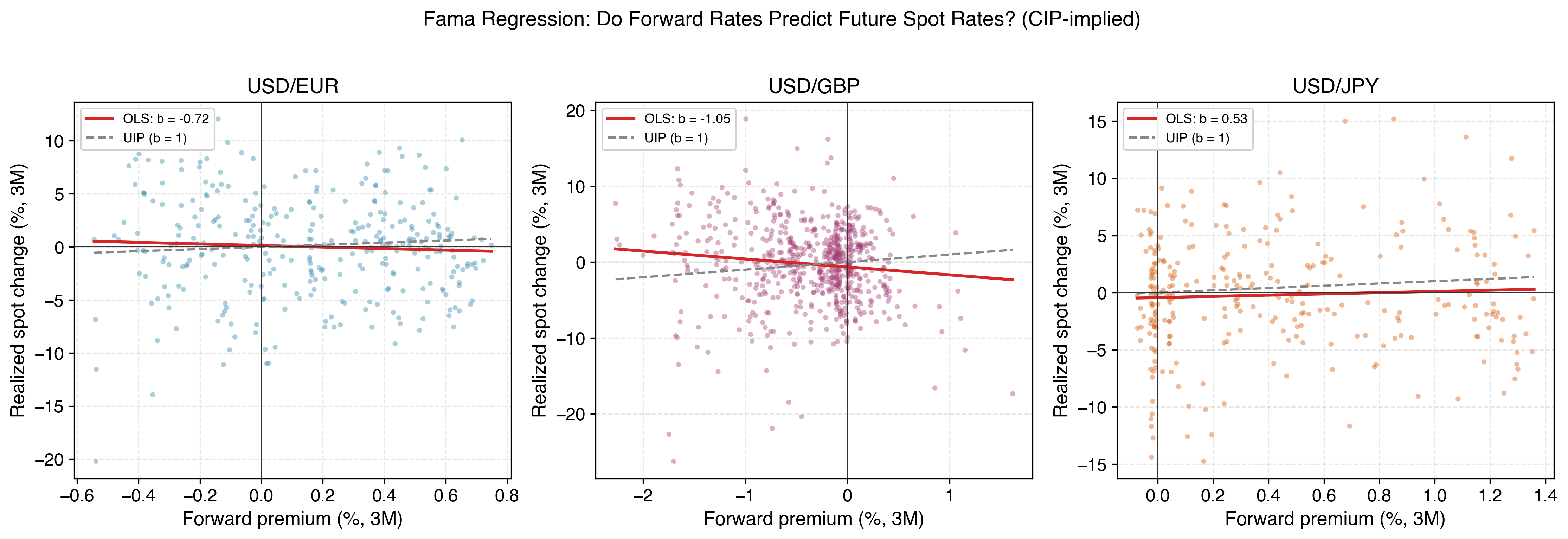

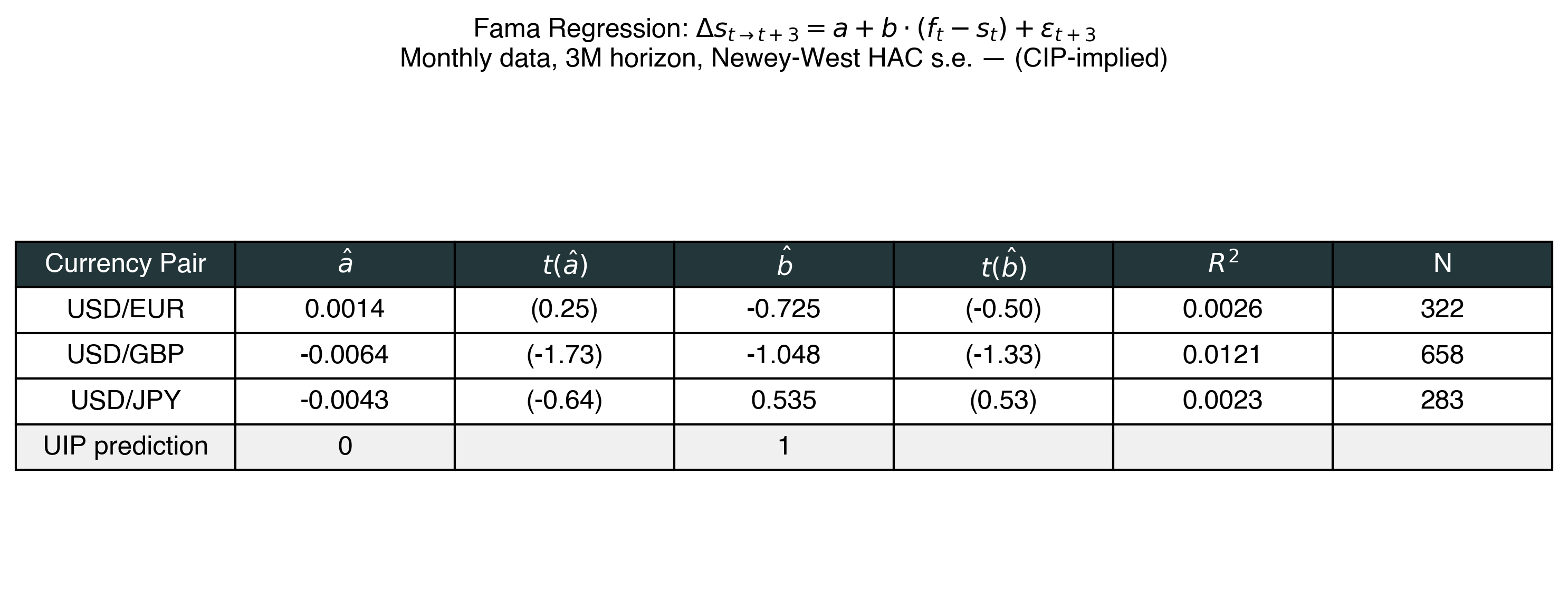

The standard test of UIP is the Fama (1984) regression:

\[\Delta s_{t \to t+k} = a + b \cdot (f_t - s_t) + \varepsilon_{t+k}\]

where \(\Delta s = \ln(S_{t+k}/S_t)\) and \(f_t - s_t = \ln(F_{t,t+k}/S_t) \approx r_t - r^*_t\).

Under UIP:\(a = 0\), \(b = 1\).

This is the most important empirical test in international finance.

Empirical Evidence: UEH and UIP Fail

The evidence

Source: Exchange Rate Dynamics, Martin D. D. Evans.

UIP predicts \(b = 1\): high interest rate currencies depreciate.

The data show \(b < 0\): high interest rate currencies tend to appreciate.

The forward premium predicts the wrong direction of spot rate changes.

Implication: An investor who borrows in low-rate currencies and invests in high-rate currencies earns positive excess returns on average. This is the carry trade — and it works precisely because UIP fails.

Why is \(b\) negative?

Three leading explanations:

Risk premium — investors require compensation for bearing FX risk. The forward rate embeds a risk premium: \(F_t = E_t[{\widetilde{S}}_{t+1}] + \text{risk premium}\)

Peso problems — rare but large events (currency crashes, regime changes) that are rationally anticipated but haven’t occurred in the sample

Key insight for the course

UIP fails → currency risk premia exist.

Risk management: Forwards transfer FX risk at market prices.

Financing: Unhedged FX debt is a carry exposure. Fully swapped debt is mostly a CIP/basis question.

Investment: Currency exposure affects the cost of capital.

Do not double count: changing the hedge changes both cash-flow risk and the discount rate.

Broader Predictability

Forecasting with macroeconomic variables

Several theories relate exchange rates to macroeconomic fundamentals:

Purchasing Power Parity (covered in Lecture 3)

Balance of payments models

Monetary models

Real business cycle models

Portfolio balance models

These are covered in international macroeconomics. For this course, the key question is: do they forecast?

The exchange rate disconnect puzzle

Empirical evidence:

Correlations between exchange rate changes and fundamentals are low

Regression coefficients are insignificant

\(R^2\) values are near zero

Exchange rates appear disconnected from observable macroeconomic variables in the short run.

This is one of the major puzzles in international finance (Meese and Rogoff, 1983): macroeconomic models cannot beat the random walk in out-of-sample forecasting.

Forecasting record of professionals

Technical forecasters:

Have a somewhat better record than fundamental models

But performance is not persistent: the best forecasters this year are not the best next year

Fundamental forecasters:

May predict the direction (\(S_{t+1} > F_t\) or \(S_{t+1} < F_t\)) slightly better than chance

But no service consistently outperforms

Central banks:

Claim to smooth exchange rates, not move them away from fundamentals

If true, they must predict well — but the empirical evidence is mixed

Private information: order flow

Order flow = net of buyer-initiated minus seller-initiated orders

Dealers who observe order flow can predict short-term (daily) movements

Order flow and exchange rates are strongly positively correlated: prices rise with buying pressure

But order flow has no predictive power for medium and long-term horizons

Private information helps at very short horizons but does not resolve the broader predictability puzzle.

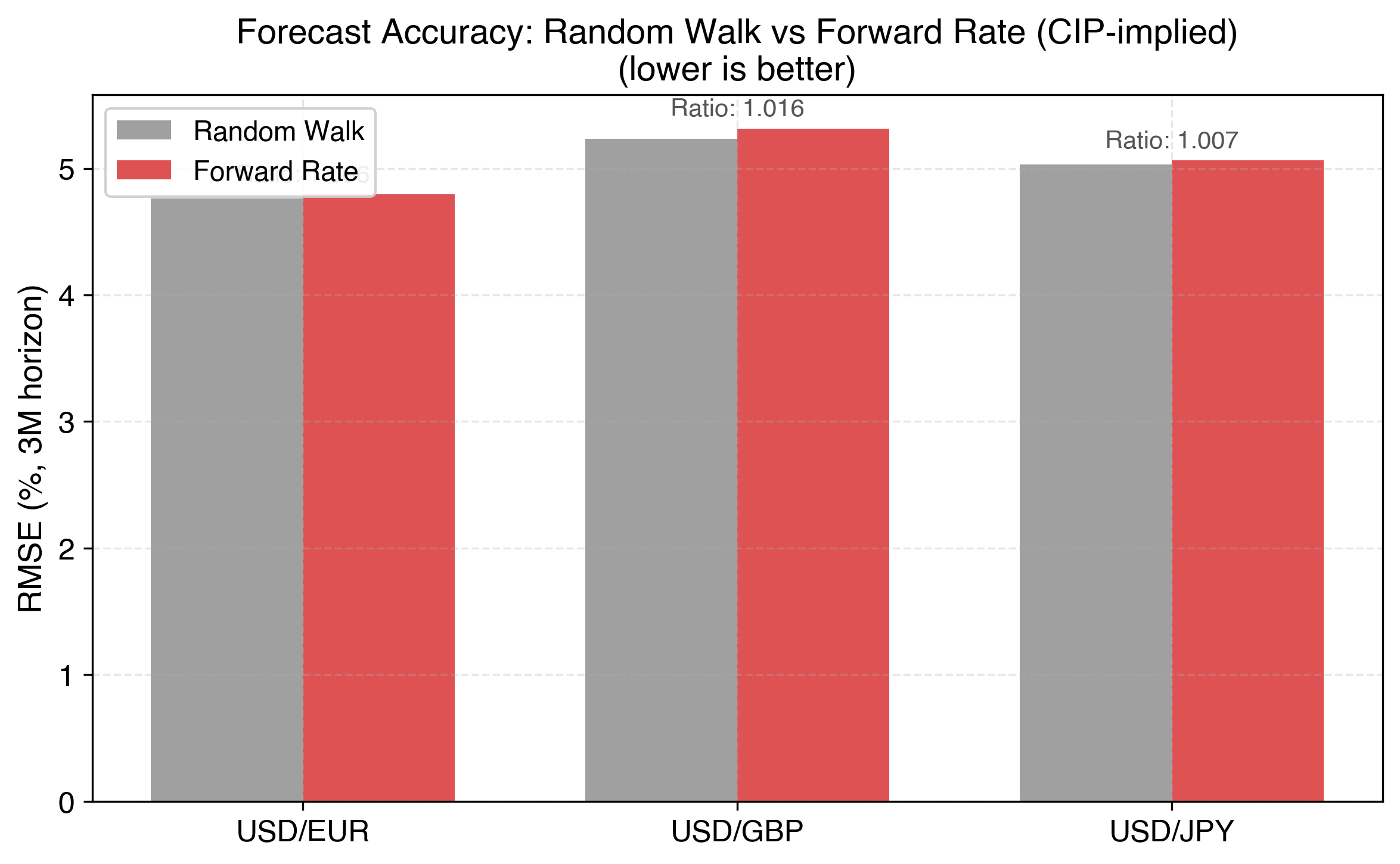

The random walk is hard to beat

3M forecast horizon. Ratio < 1 means the forward rate beats the random walk.

Summary of predictability

Weak form (past prices): Some short-run autocorrelation, but does not beat random walk out of sample.

Semi-strong form (public information): Macroeconomic models fail to beat random walk. Forward rates predict the wrong direction. Exchange rate disconnect puzzle.

Strong form (private information): Order flow predicts daily movements only.

Bottom line: Exchange rates are essentially unpredictable at short and medium horizons. The random walk is very hard to beat.

This is why FX risk matters for firms.

Cross-Section of Currency Returns

Currency returns have structure

Even though individual exchange rates are hard to predict, portfolios of currencies sorted by observable characteristics earn systematic returns:

Carry factor: Long high-interest-rate currencies, short low-interest-rate currencies. Positive average return but negative skewness (crash risk).

Dollar factor: Average return of all currencies vs. USD. Captures global risk appetite — goes up when the dollar weakens.

Momentum factor: Currencies that appreciated recently tend to continue appreciating.

Why the cross-section matters

These factors tell us that UIP failure is not random — it has structure:

High-rate currencies earn positive excess returns (carry) because they expose investors to crash risk

The dollar factor captures the price of global risk

Lustig, Roussanov, and Verdelhan (2011): high interest rate currencies load on a global risk factor. Carry returns are compensation for bearing systematic risk, not anomalies.

Preview: Full treatment of these factors and their implications for the cost of capital in Lecture 7.

Connection to firm decisions

Currency premia matter because firms have FX exposures.

Hedging: Forwards transfer FX risk at market prices.

Financing: Unhedged FX debt can be a carry exposure.

Investment: Systematic FX exposure affects discount rates.

Avoid double counting: hedging changes both cash-flow risk and the appropriate discount rate.

Summary

Summary

PPP fails \(\Rightarrow\) real FX risk exists (Lecture 3)