Main issues

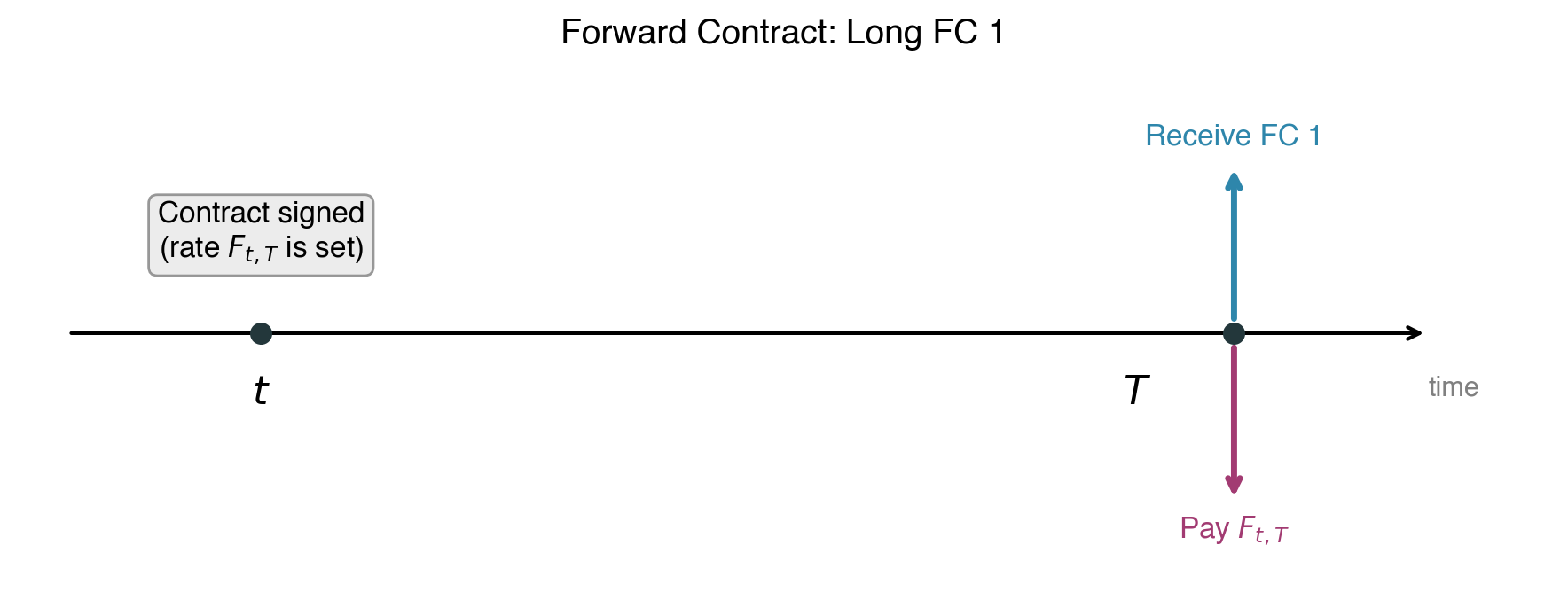

Understanding forward exchange contracts

Hedging with forward contracts

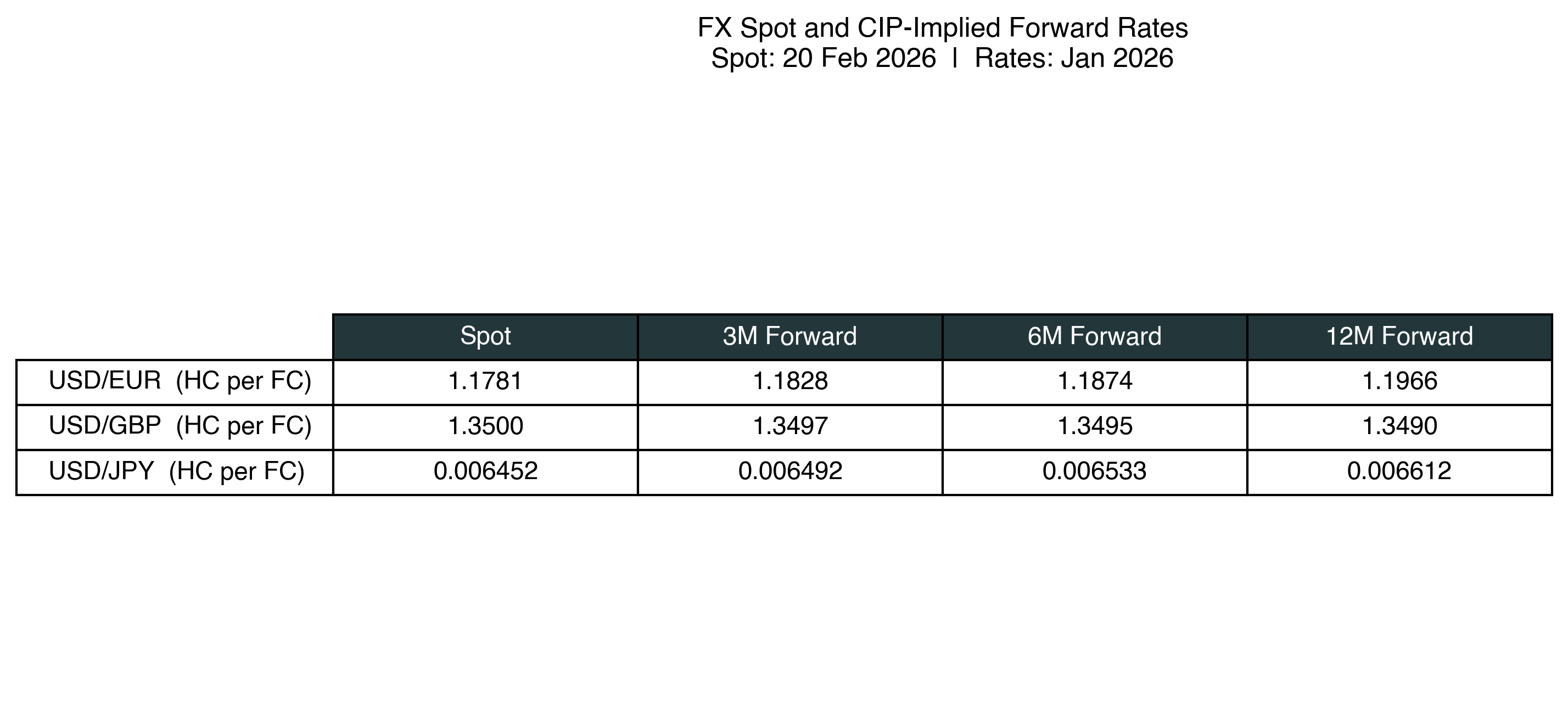

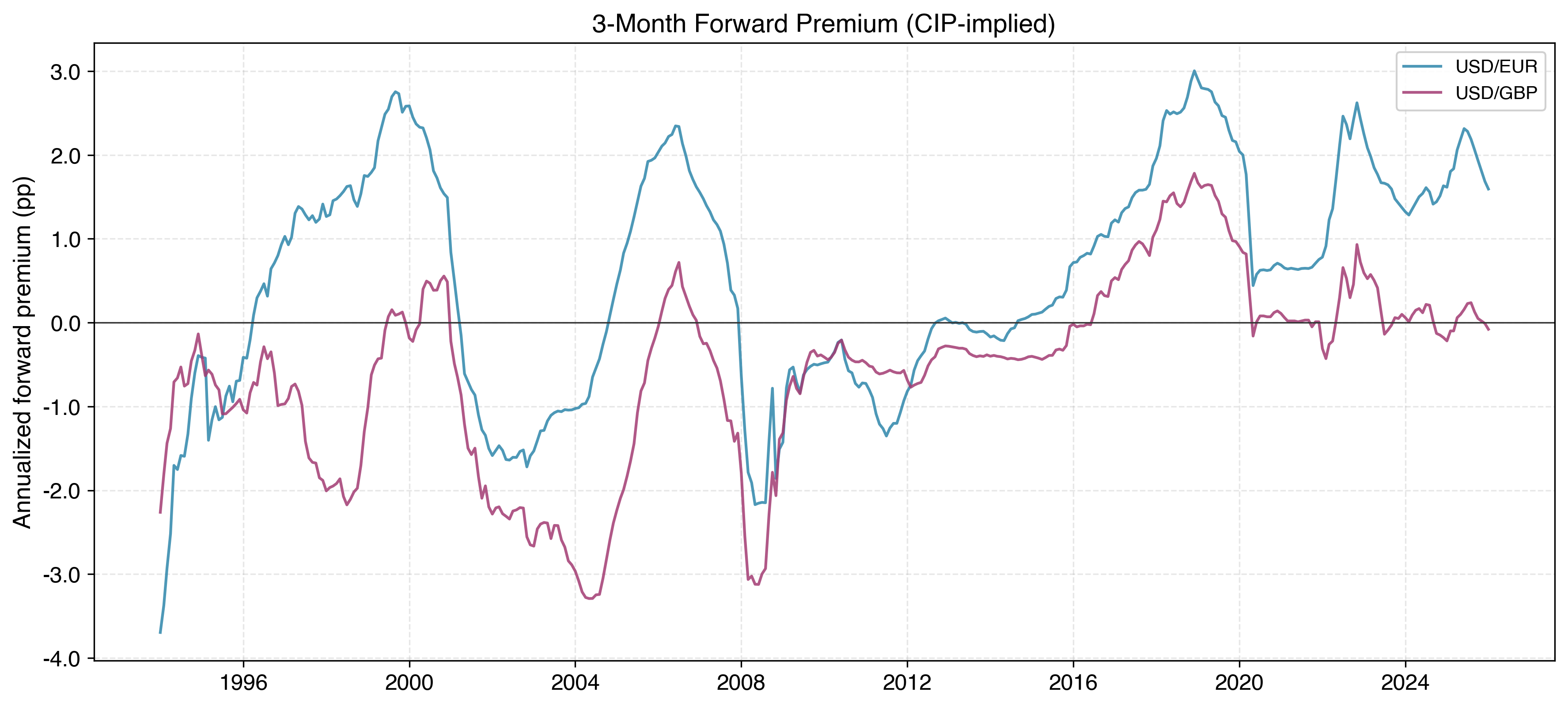

Covered interest rate parity (CIP)

Valuation of forward contracts

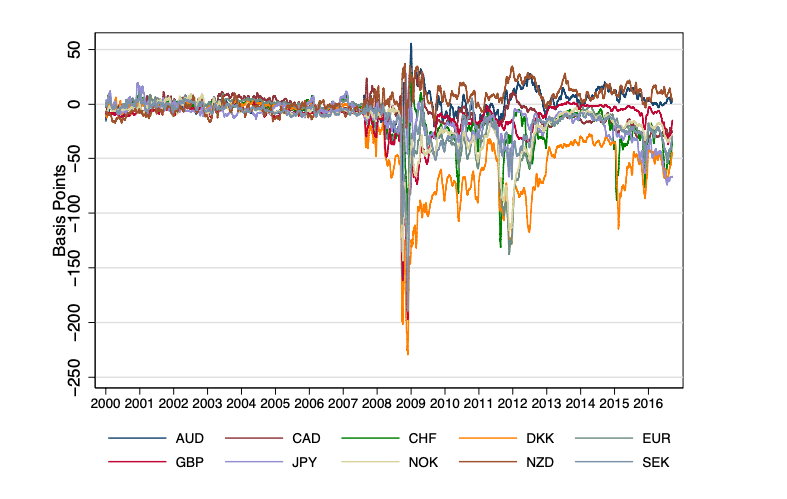

The cross-currency basis: when CIP “fails”

The Forward Market for Foreign Exchange

Understanding forward exchange contracts

Hedging with forward contracts

Covered interest rate parity (CIP)

Valuation of forward contracts

The cross-currency basis: when CIP “fails”

The forward exchange rate \(F_{t,T}\) is the price agreed upon today (\(t\)) at which one currency can be exchanged for another at a future date (\(T\)).

CIP-implied from spot rates and 3M interbank interest rates. Source: FRED.

FC inflows at a future date \(\rightarrow\) sell FC forward

FC outflows at a future date \(\rightarrow\) buy FC forward

Hedging translates:

A future FC cashflow whose HC value depends on the random \({\tilde S}_T\)

Into a known HC amount equal to \(F_{t,T}\)

The forward contract eliminates exchange rate uncertainty.

Suppose:

Questions:

In frictionless markets:

\[F_{t,T} = S_t \frac{1 + r_{t,T}}{1 + r^*_{t,T}}\]

where

Where does this formula come from? We prove it via a replication argument.

Given:

| \(S_0\) (USD/GBP) | 1.26 |

| \(r^{USD}_{0,1}\) | 4.3% |

| \(r^{GBP}_{0,1}\) | 4.5% |

| \(T\) | 1 year |

CIP gives us:

\[F_{0,1} = 1.26 \times \frac{1.043}{1.045} = 1.2576\]

GBP is at a forward discount: \(F < S\).

Why? Because \(r^{GBP} > r^{USD}\).

We compare two strategies that both deliver GBP 1 at time \(T\) with zero cash flow today:

Strategy A: Buy GBP 1 forward.

Strategy B:

| Strategy | Cashflow at \(t\) | Cashflow at \(T\) |

|---|---|---|

| A: Forward | 0 | Pay \(F_{t,T}\); Receive GBP 1 |

| B: Replication | Borrow USD \(\frac{S_t}{1+r^*}\) | Pay USD \(S_t \frac{1+r}{1+r^*}\) |

| Buy GBP \(\frac{1}{1+r^*}\) spot | ||

| Invest GBP at \(r^*\) | Receive GBP 1 | |

| Net: 0 |

Both strategies: zero cost at \(t\), deliver GBP 1 at \(T\). No arbitrage \(\Rightarrow\) same cost at \(T\):

\[F_{t,T} = S_t \frac{1 + r_{t,T}}{1 + r^*_{t,T}}\]

A forward contract can be replicated using three markets:

Practical consequence: If you cannot trade forwards (e.g., restricted currency), you can create a synthetic forward using spot and money markets.

Conversely: If you observe spot, forward, and two interest rates, CIP pins down the relationship among all four. Any deviation is an arbitrage opportunity.

We can write CIP as:

\[\frac{F_{t,T}}{S_t} = \frac{1 + r_{t,T}}{1 + r^*_{t,T}}\]

\(F > S\) \(\Rightarrow\) FC is at a forward premium \(\Rightarrow\) \(r > r^*\) (HC rate is higher)

\(F < S\) \(\Rightarrow\) FC is at a forward discount \(\Rightarrow\) \(r < r^*\)

Strong currencies offer low interest rates; weak currencies compensate with high rates.

Source: 3M interbank rates from OECD via FRED, 1994–2026.

The CIP can be rewritten as:

\[\underset{\text{cost of borrowing HC 1 abroad}}{S_t^{-1}(1 + r^*_{t,T}) \, F_{t,T}} \;=\; \underset{\text{cost of borrowing HC 1 at home}}{(1 + r_{t,T})}\]

In frictionless markets, you cannot save money by borrowing in one currency rather than another (once you hedge the FX risk).

The low interest rate in JPY does not make JPY borrowing “cheap” — the forward premium offsets it exactly.

In the ratio \(\frac{1 + r_{t,T}}{1 + r^*_{t,T}}\), the numerator interest rate belongs to the numerator currency of \(S_t\).

Example: If \(S_t\) is quoted as EUR/JPY:

\[F_{t,T} = S_t \frac{1 + r^{EUR}_{t,T}}{1 + r^{JPY}_{t,T}}\]

EUR is in the numerator of the exchange rate \(\Rightarrow\) EUR rate goes in the numerator.

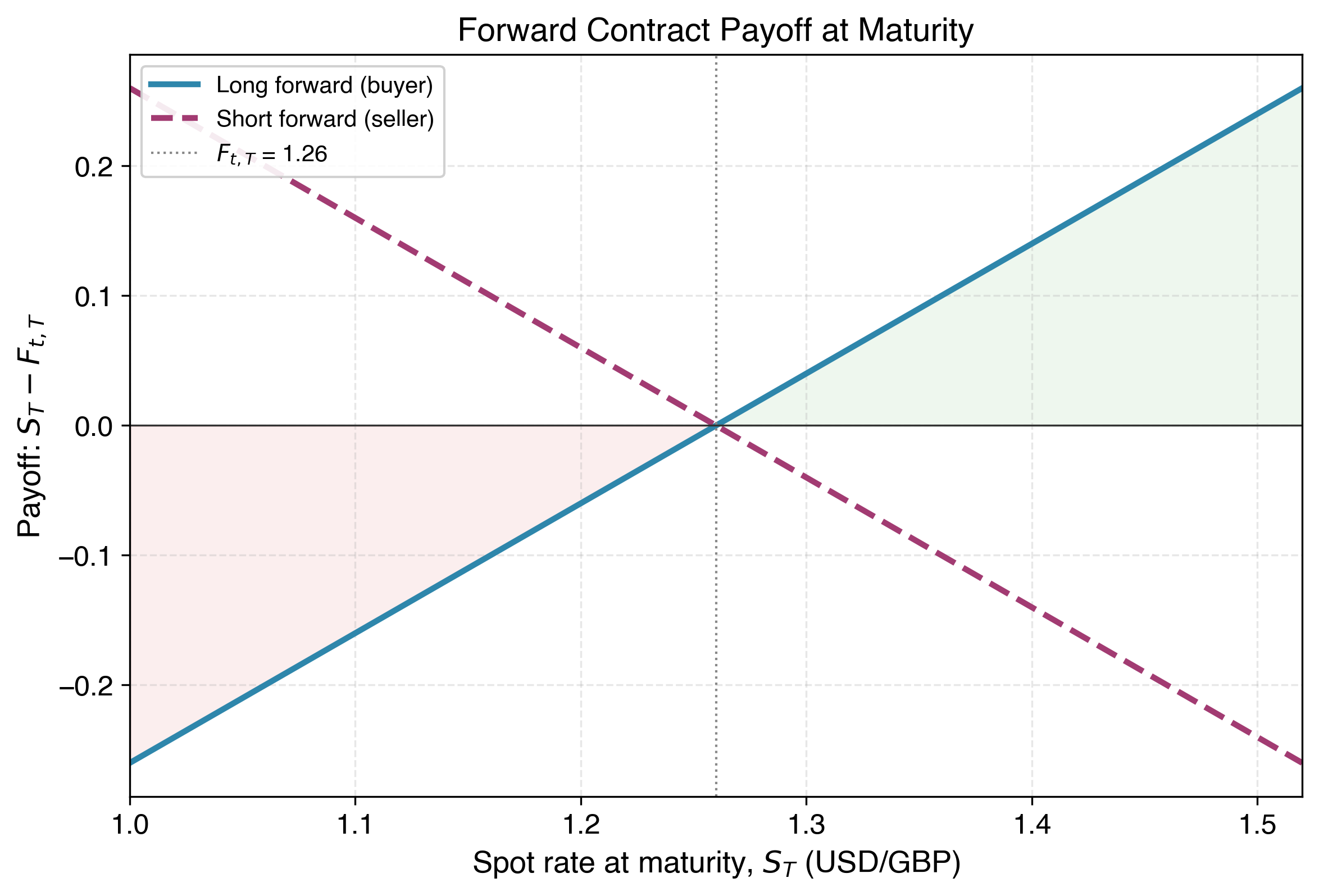

At \(t+1\), value a forward initiated at \(t\) (maturity \(T\), rate \(F_{t,T}\)) to buy FC 1.

Cashflows at \(T\): Receive FC 1, Pay HC \(F_{t,T}\). Present value at \(t+1\):

\[V_{t+1} = \frac{S_{t+1}}{1 + r^*_{t+1,T}} - \frac{F_{t,T}}{1 + r_{t+1,T}}\]

Using CIP: \(\frac{S_{t+1}}{1+r^*_{t+1,T}} = \frac{F_{t+1,T}}{1+r_{t+1,T}}\), so:

\[V_{t+1} = \frac{F_{t+1,T} - F_{t,T}}{1 + r_{t+1,T}}\]

\[V(T) = S_T - F_{t,T}\]

At the initiation date \(t\):

\[V(t) = \frac{S_t}{1 + r^*_{t,T}} - \frac{F_{t,T}}{1 + r_{t,T}}\]

But CIP tells us \(F_{t,T} = S_t \frac{1 + r_{t,T}}{1 + r^*_{t,T}}\), which means \(\frac{S_t}{1 + r^*_{t,T}} = \frac{F_{t,T}}{1 + r_{t,T}}\).

Therefore: \(V(t) = 0\).

The forward rate is chosen so the contract is fair at initiation — neither party pays the other.

3M forward for GBP at \(F_{0,T}\) = USD/GBP 1.26. At initiation: \(V_0 = 0\).

After 1 month, spot is \(S_{t+1}\) = 1.28:

\[V_{t+1} = \frac{1.28}{1 + r^*_{t+1,T}} - \frac{1.26}{1 + r_{t+1,T}} \approx 0.02 > 0 \quad \text{(positive value to buyer)}\]

At maturity, spot is \(S_T\) = 1.30:

\[V_T = 1.30 - 1.26 = 0.04 \text{ per GBP}\]

Suppose you are offered FC 1 at future date \(T\). The present value can be computed two ways:

\[PV = \underset{\text{risky CF at risk-adjusted rate}}{\frac{E_t[{\tilde S}_T]}{1 + {\tilde r}_{t,T}}} \;=\; \underset{\text{safe CF at riskless rate}}{\frac{F_{t,T}}{1 + r_{t,T}}}\]

Therefore: \(F_{t,T} = CEQ_t({\tilde S}_T)\)

The forward rate is the certainty equivalent of the future spot rate.

CIP links the current spot rate, the current forward rate, and interest rates.

CEQ links the future spot rate and the current forward rate.

Important: \(F_{t,T} = CEQ_t({\tilde S}_T)\) does not imply \(F_{t,T} = E_t[{\tilde S}_T]\).

Whether the forward rate equals the expected future spot rate is the question of the Unbiased Expectations Hypothesis (UEH). This is tested separately and generally fails — which we will cover in a later lecture.

In frictionless theory: CIP holds exactly, and forward rates are pinned by interest-rate differentials.

In practice: Small but persistent CIP deviations exist, especially since the 2008 financial crisis, and they can widen sharply in stress periods.

The cross-currency basis measures the deviation:

\[\text{basis} = \text{actual USD money-market rate} - \text{synthetic USD rate implied by the FX swap}\]

A negative basis means it is more expensive to obtain USD synthetically through FX swaps than to borrow USD directly.

Source: Du, Tepper and Verdelhan (2018), “Deviations from Covered Interest Rate Parity,” Figure 2.

Balance-sheet constraints: Banks need scarce balance-sheet capacity to intermediate FX swaps. Basel III leverage-ratio rules can limit supply.

Funding stress: Dollar shortages can force foreign institutions to pay a premium for synthetic USD funding, as during the GFC and COVID stress periods.

Regulatory/reporting costs: Quarter-end leverage-ratio and balance-sheet reporting can create predictable spikes.

Segmentation: Not all market participants can arbitrage freely, including some insurers, central banks, and real-money investors.

For the firm: The basis is a hedging-cost and funding-risk signal. When the relevant basis moves against the firm, hedging costs rise.

Forward contracts allow hedging of future FC cashflows at a known rate.

CIP: \(F_{t,T} = S_t \frac{1 + r}{1 + r^*}\), where \(S_t\) is domestic currency per unit of foreign currency, \(r\) is the domestic interest rate, and \(r^*\) is the foreign interest rate — proved via replication (no arbitrage).

Forward valuation: An at-market forward has \(V_0 = 0\) at initiation. For a long forward to buy one unit of FC, the maturity payoff is \(V_T = S_T - F_{0,T}\). The value can change between initiation and maturity.

Under textbook CIP, you cannot save money by borrowing in another currency once the FX exposure is fully hedged. In practice, cross-currency basis, credit, collateral, and balance-sheet costs can make all-in hedged funding costs differ across currencies.

Forward rate = no-arbitrage hedging price, sometimes interpreted as a certainty-equivalent price, but \(\neq\) the expected future spot rate.

Cross-currency basis: Real-world frictions create persistent CIP deviations. The basis matters for hedging cost and funding decisions.