Main issues

Does exchange rate risk exist?

Purchasing power parity: absolute and relative

Empirical evidence across horizons

The real exchange rate and why PPP failure matters for firms

Purchasing Power Parity and Real Exchange Rates

Does exchange rate risk exist?

Purchasing power parity: absolute and relative

Empirical evidence across horizons

The real exchange rate and why PPP failure matters for firms

Is there exchange rate risk?

Most likely — but not necessarily.

If all prices adjust immediately and fully to exchange rate changes, then nominal FX movements have no real effect.

This is what Purchasing Power Parity claims.

Does this actually happen?

June 2016: GBP depreciates $$15% after Brexit referendum.

Apple raises UK prices weeks later:

| GBP Price | USD/GBP | Implied USD Price | |

|---|---|---|---|

| May 2016 (pre-Brexit) | £499 | 1.45 | $724 |

| Sep 2016 (post-Brexit) | £549 | 1.33 | $730 |

Some pass-through happened — but it took weeks, was incomplete, and was a discrete jump. Not the smooth continuous adjustment PPP assumes.

Define the real exchange rate:

\[e_t = S_t \cdot \frac{P^*_t}{P_t}\]

where \(S_t\) is the nominal rate (HC/FC), \(P_t\) is the HC price level, \(P^*_t\) is the FC price level.

If PPP holds: \(e_t = 1\) (or constant)

If \(e_t\) moves: there is real exchange rate risk

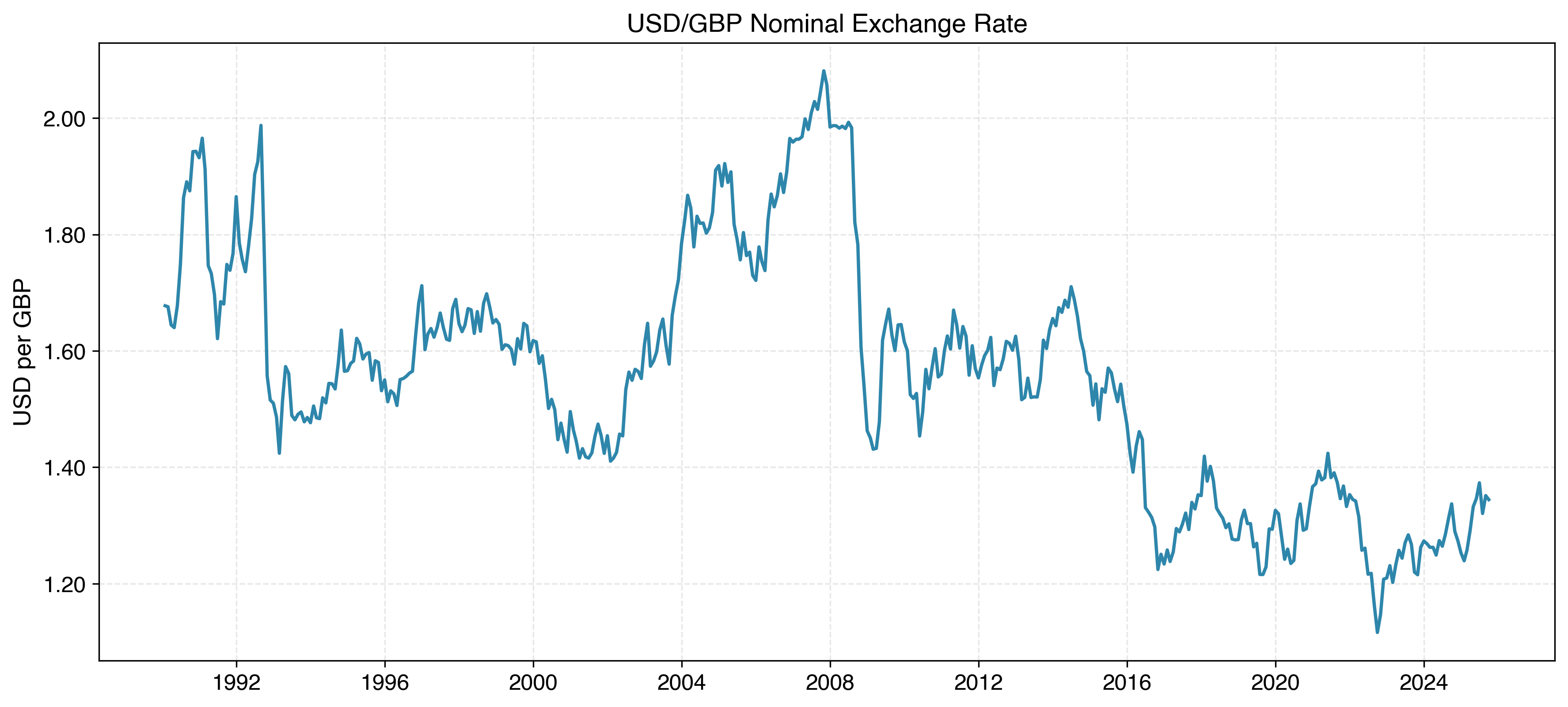

Preview: \(e_t\) is not constant. Not even close.

The exchange rate equals the ratio of price levels:

\[S_t = \frac{P_t}{P^*_t}\]

Rationale: If the equality does not hold, one could exploit “real” arbitrage on physical goods. Prices should be the same once converted to a common currency.

Example: If a good costs $0.50 in the US and NOK 1.50 in Norway:

\[\text{USD/NOK} = \frac{0.50}{1.50} = \frac{1}{3}\]

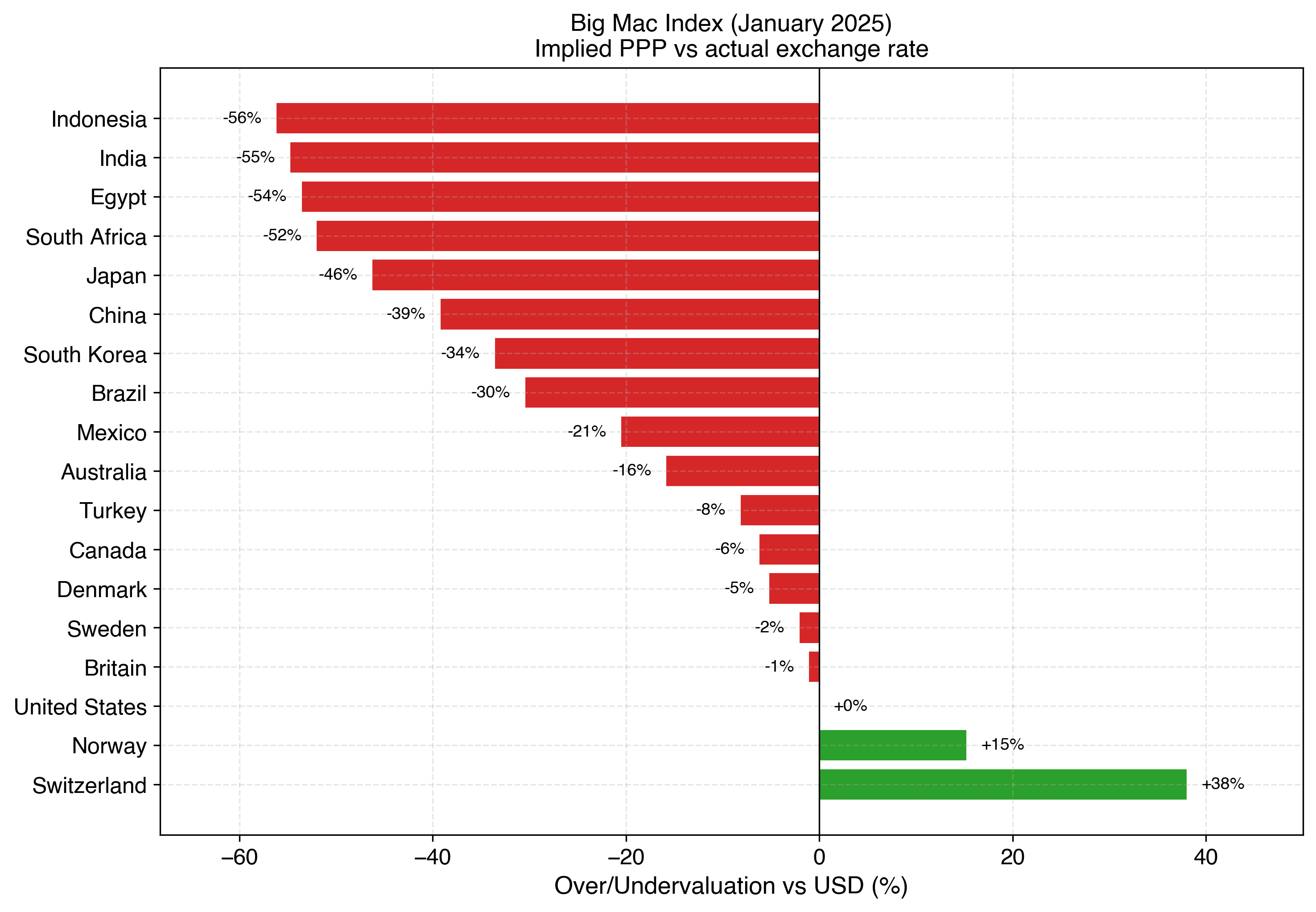

Source: The Economist, Big Mac Index (January 2025)

Many goods are non-traded: high transport costs (cement, bricks), services (haircuts, healthcare)

Even for traded goods: transport costs, tariffs, trade barriers create bands around PPP

Only considers goods and services, not capital flows

Balassa-Samuelson effect creates systematic deviations (next slide)

Conclusion: Absolute PPP — \(e_t = 1\) always — is too strong. We need to relax it.

Productivity in traded goods is higher in developed countries than emerging economies

Productivity in non-traded services is similar everywhere (haircuts, taxis)

But wages equalize within a country across sectors — so non-traded goods are expensive in rich countries

Example: A haircut costs $40 in Oslo and $15 in São Paulo — but the barbers are equally skilled.

Implication: Price levels are systematically higher in richer countries. Absolute PPP is biased.

This is exactly what the Big Mac Index shows.

Exchange rate changes should be proportional to relative inflation:

\[S_1 = \frac{P_1/P_0}{P^*_1/P^*_0} \cdot S_0\]

Log-differenced version:

\[\Delta s_t \approx \pi_t - \pi^*_t\]

This relaxes the level condition — only requires changes to offset.

Rationale:

Higher inflation at home \(\rightarrow\) home currency depreciates

Depreciation compensates foreign buyers for higher domestic prices

Prediction:

What it does NOT require: That price levels are equalized across countries (unlike absolute PPP)

Does not account for structural changes (wars, regime shifts, financial crises)

Balassa-Samuelson applies here too: if one country is growing faster, its non-traded prices rise faster, creating a secular trend

Works better at very long horizons (decades) but poorly at business-cycle frequencies

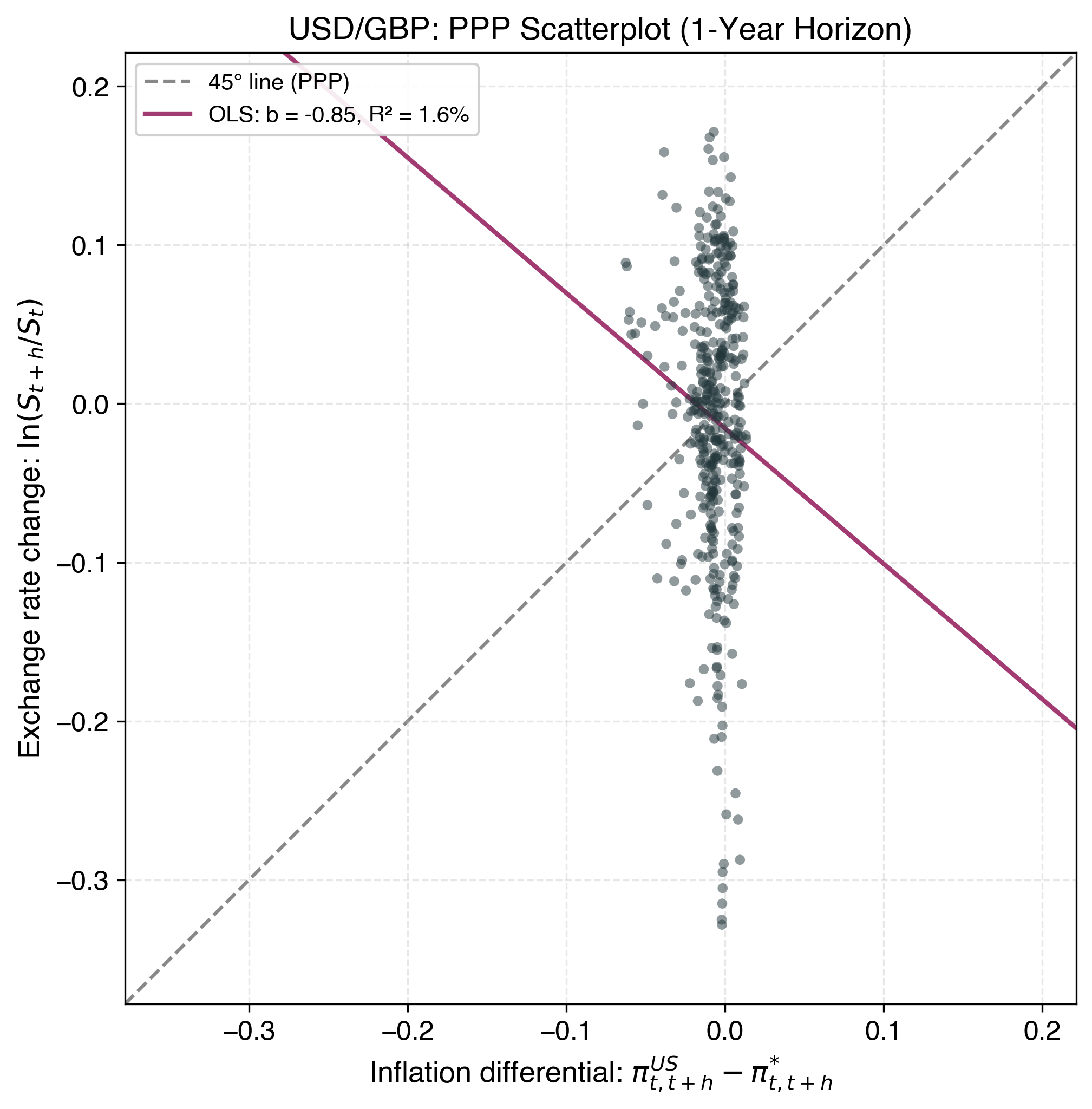

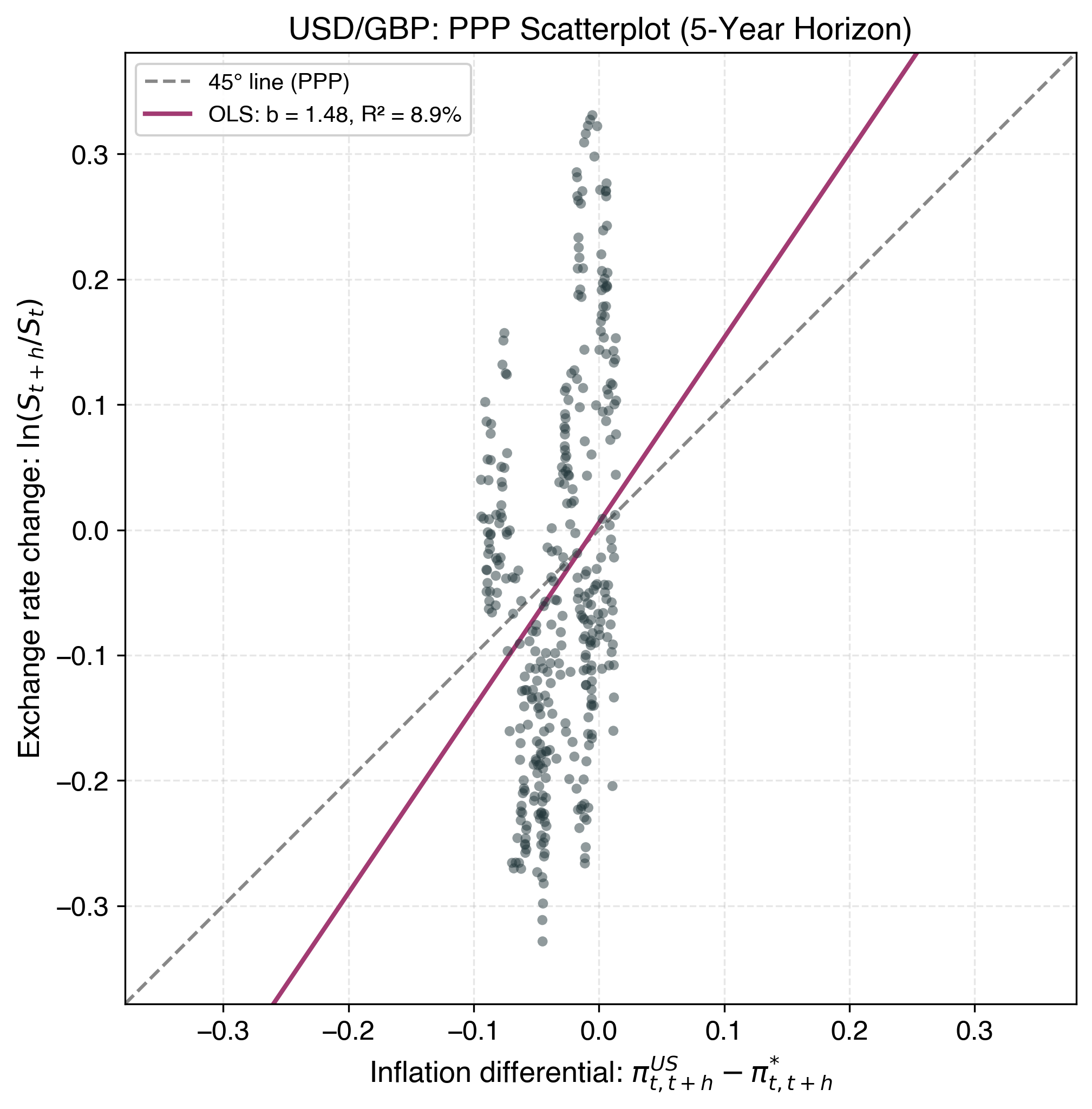

How badly does it fail? Let’s look at the data.

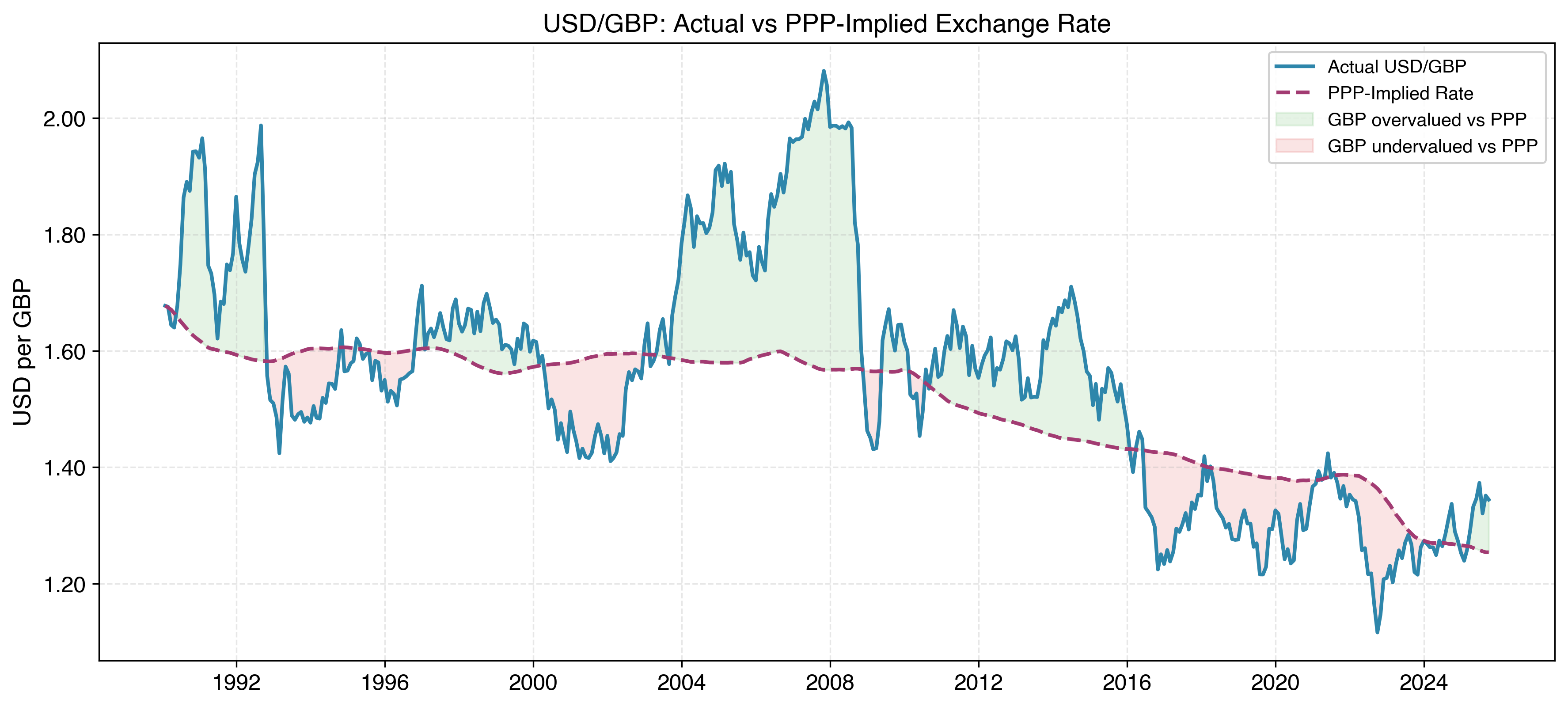

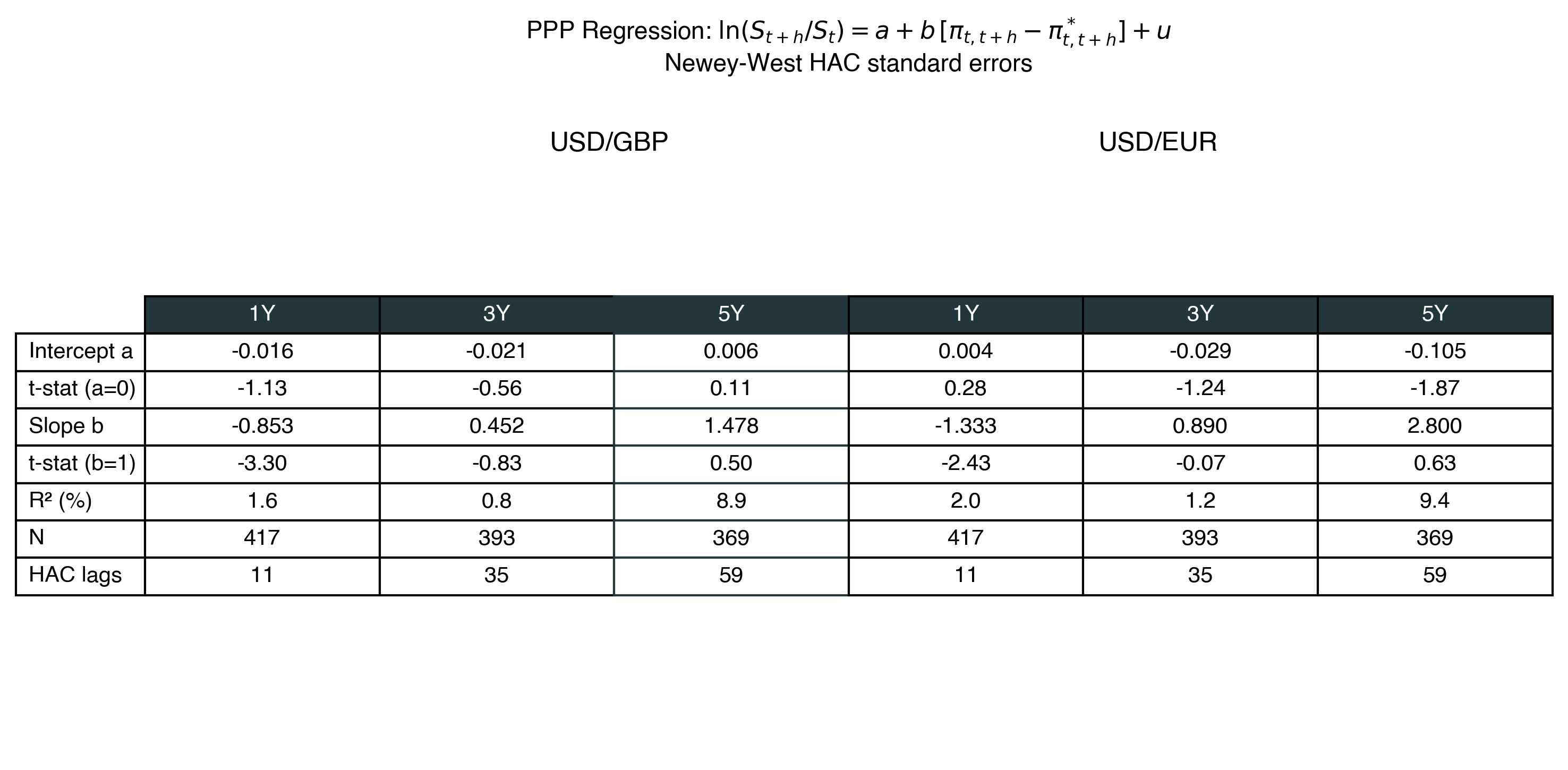

Data: 1990–2025. PPP-implied rate uses cumulative US vs UK inflation from base period.

Regression:

\[\ln\frac{S_{t+h}}{S_t} = a + b\left[\pi^{US}_{t,t+h} - \pi^{UK}_{t,t+h}\right] + u_{t+h}\]

PPP null hypothesis: \(a = 0\) and \(b = 1\)

Test at multiple horizons: \(h \in \{1, 3, 5\}\) years

Forward-looking inflation: \(\pi_{t,t+h} = \ln(P_{t+h}/P_t)\)

Newey-West HAC standard errors (overlapping observations)

Short horizon (1Y): \(R^2 \approx 0\), slope far from 1 \(\rightarrow\) PPP has no predictive power

Medium horizon (3Y): \(R^2\) improves, slope moves toward 1 \(\rightarrow\) slow convergence

Long horizon (5Y): \(R^2\) rises further \(\rightarrow\) PPP gains explanatory power but remains noisy

Same pattern for USD/EUR — this is not a GBP-specific result.

The PPP puzzle (Rogoff 1996): Deviations have half-life of 3–5 years. Too slow for nominal rigidities alone. Too fast for purely real shocks.

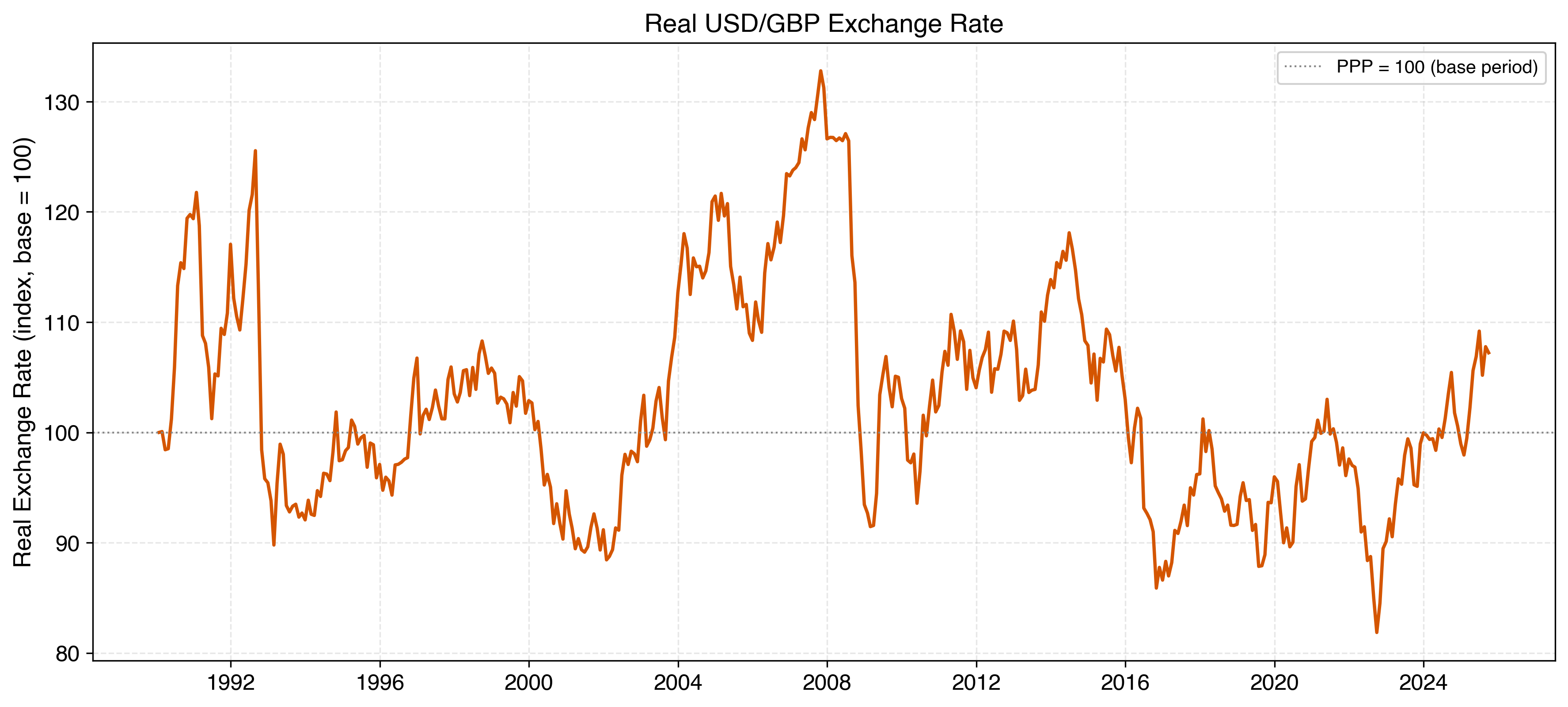

Real USD/GBP = \(S_t \cdot P^{UK}_t / P^{US}_t\), indexed to 100 at start of sample.

Swings of \(\pm 30\%\) lasting years — not noise

Mean-reverting over decades but not at business-cycle frequencies

Each swing represents a period where goods are genuinely cheaper or more expensive across countries

When the real rate rises: Foreign goods become expensive relative to domestic. Domestic exporters gain competitiveness.

When the real rate falls: The reverse. Domestic firms face margin compression from foreign competition.

PPP failure means nominal FX changes have real effects:

Revenue in FC may not be offset by cost changes

Competitive position shifts with the real exchange rate

Margin compression, volume changes, supply chain costs

This is the bridge from Layer 1 to Layer 3:

Absolute PPP fails: non-traded goods, transport costs, Balassa-Samuelson

Relative PPP works only at very long horizons (decades, not years)

Real exchange rate risk is persistent and economically large (\(\pm 30\%\))

For the firm: FX exposure is real, not just nominal — this is why hedging, financing, and investment decisions are hard

PPP failure motivates the entire corporate block:

Other exchange rate models exist (monetary approach, Dornbusch overshooting, portfolio balance) — they all perform poorly at short horizons. We focus on what matters for the firm.