Main issues

The foreign exchange market

Conventions for quoting the spot exchange rate

Bid-ask spreads and transaction costs

Arbitrage and the law of one price

The Spot Market for Foreign Exchange

The foreign exchange market

Conventions for quoting the spot exchange rate

Bid-ask spreads and transaction costs

Arbitrage and the law of one price

Decentralized, global, over-the-counter (OTC) market for exchanging currencies

The largest financial market in the world

Open nearly 24 hours — follows the sun:

Sydney → Tokyo → London → New York

Three questions:

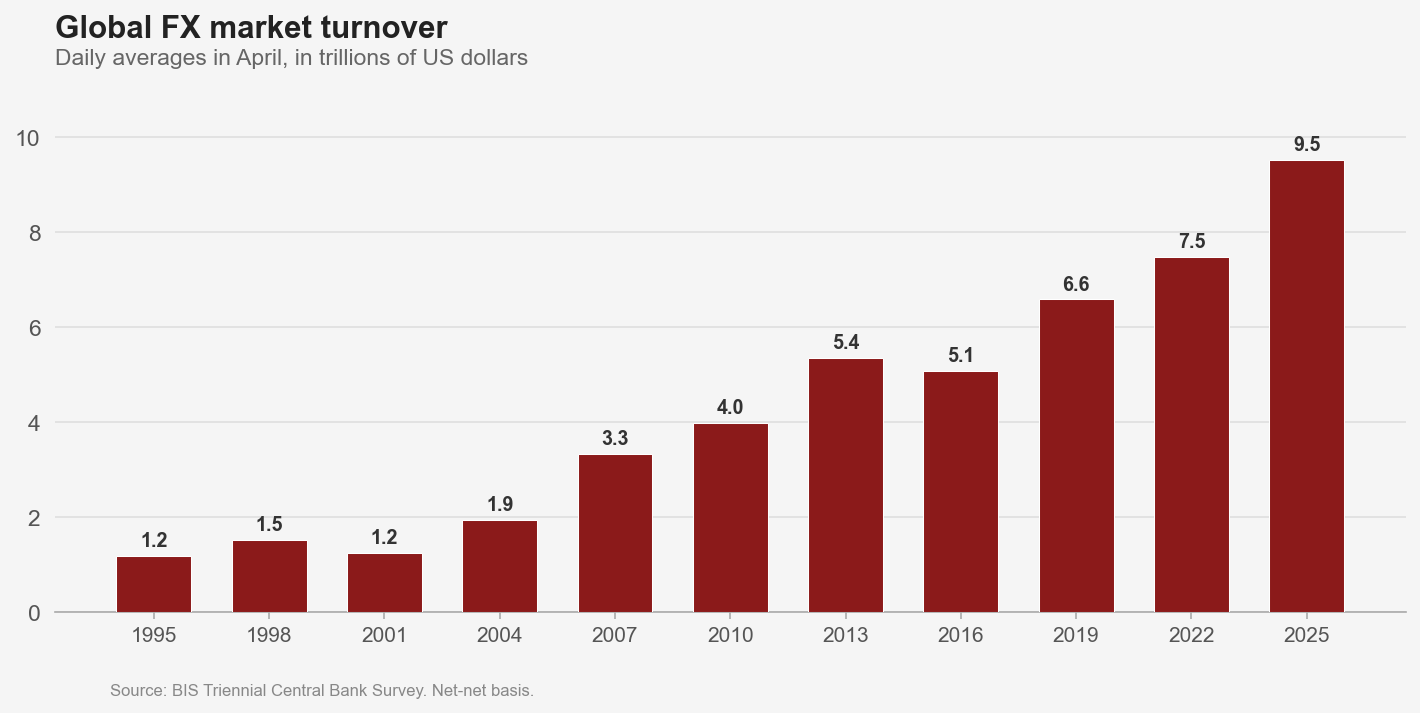

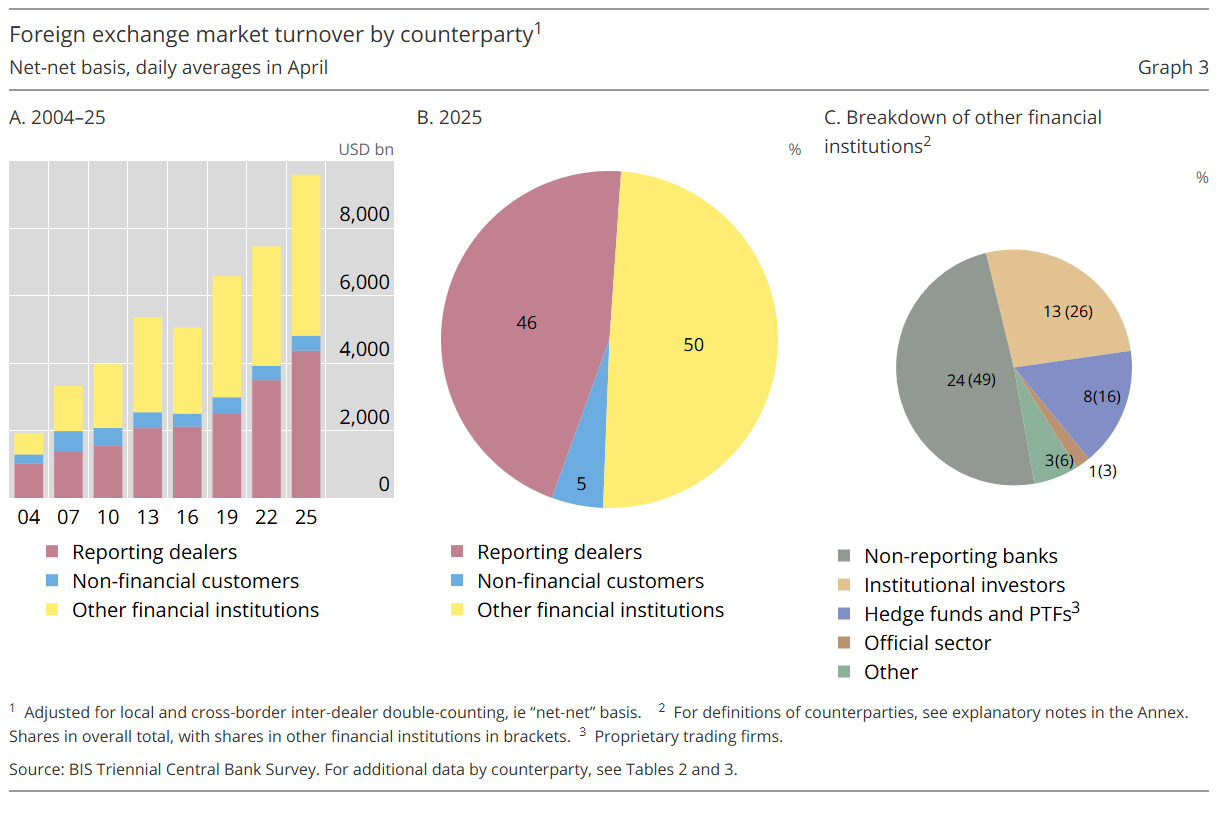

Source: BIS Triennial Central Bank Survey (2025)

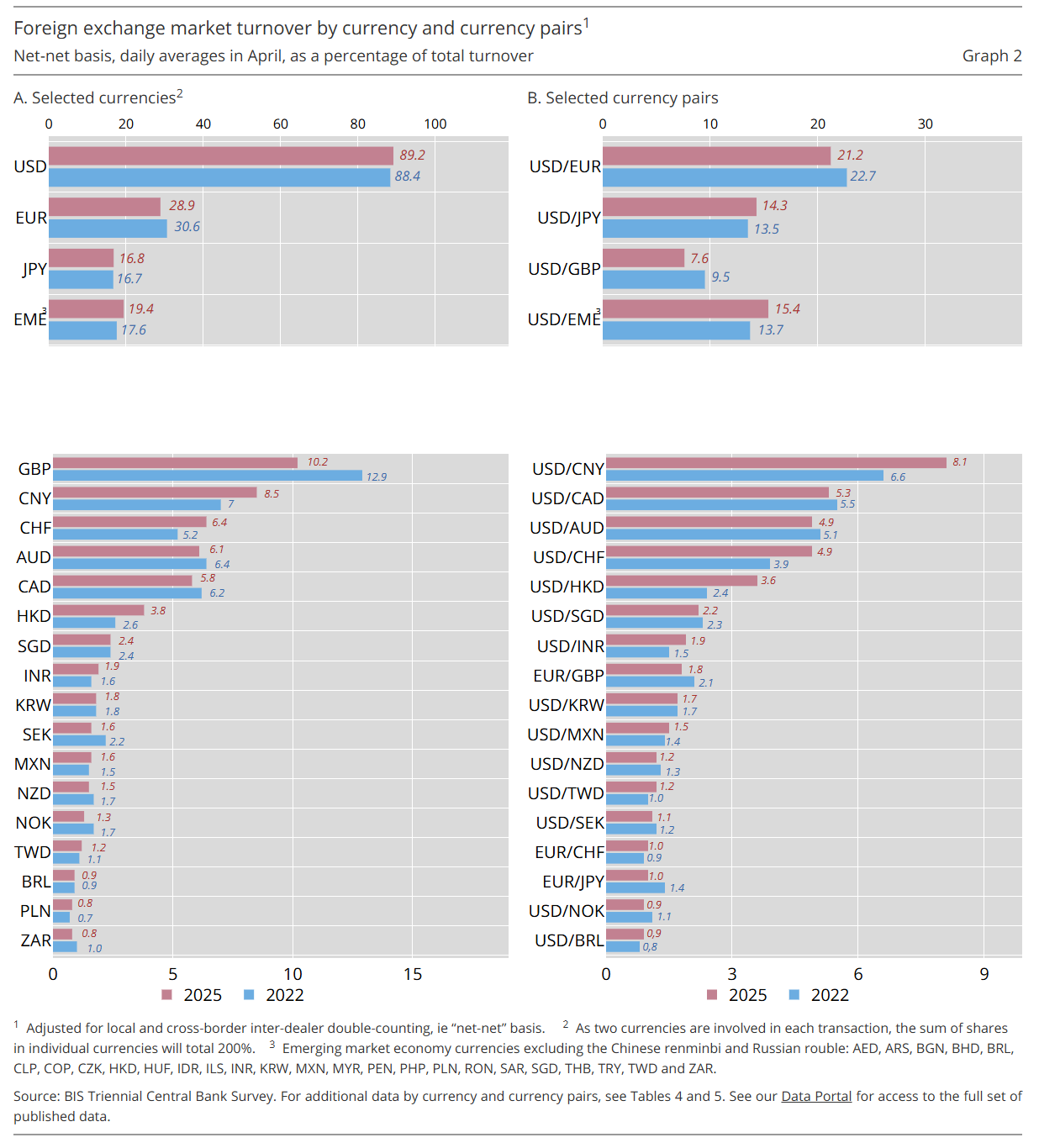

Source: BIS Triennial Central Bank Survey (2025)

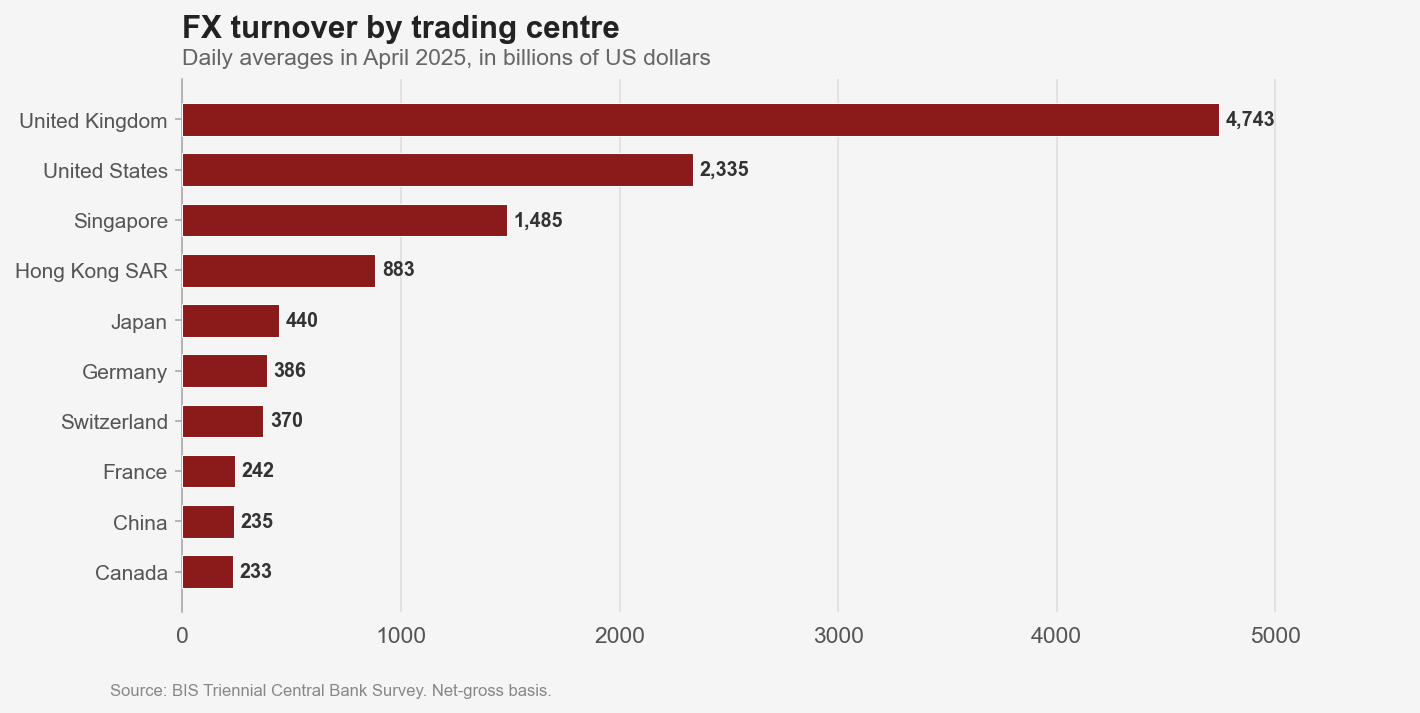

Source: BIS Triennial Central Bank Survey (2025)

Reporting dealers (banks): Make markets, warehouse risk, provide liquidity

Other financial institutions: Asset managers, hedge funds, central banks, pension funds

Non-financial corporations: Hedging commercial FX exposures

Retail: Small fraction; mostly via online platforms

The market has shifted heavily toward electronic trading (EBS, Reuters Matching, multi-dealer platforms).

Source: BIS Triennial Central Bank Survey (2025)

Source: BIS Triennial Central Bank Survey (2025)

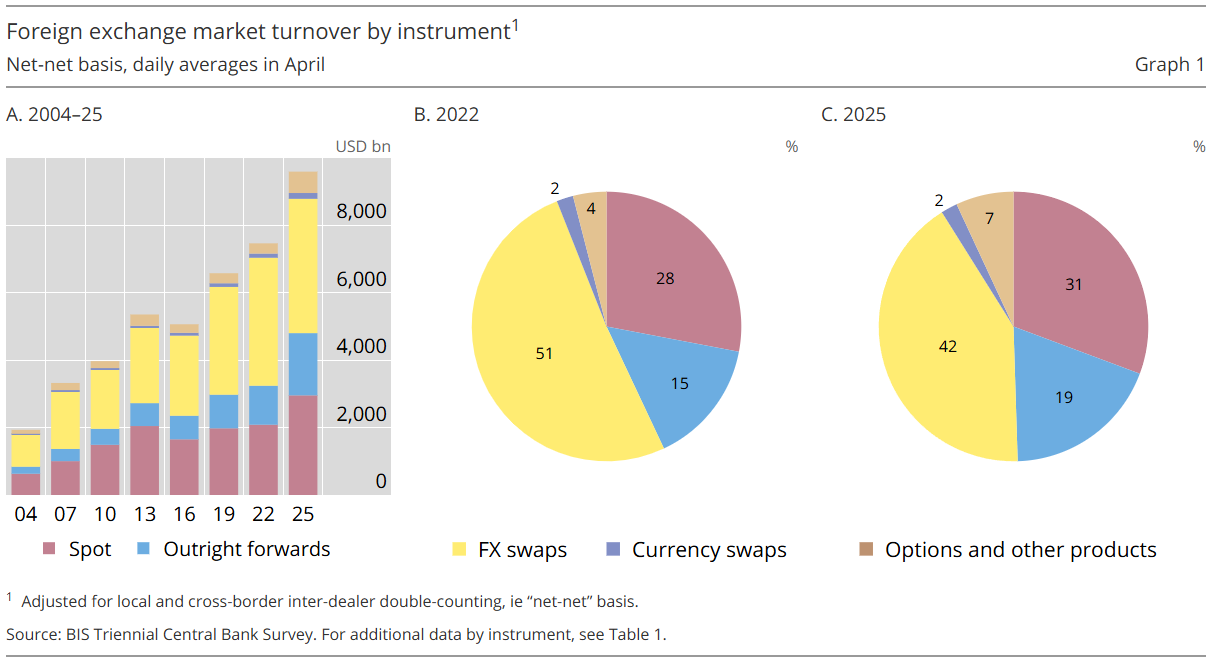

| Instrument | Share of turnover |

|---|---|

| FX swaps | ~42% |

| Spot | ~31% |

| Outright forwards | ~18% |

| Options & other | ~8% |

The forward and swap markets are larger than spot.

We cover forwards in Lecture 3, swaps in Lecture 6.

Spot market:

Forward market:

We need to understand spot first — forward prices are derived from spot plus interest rates.

The spot rate \(S_t\) is the amount of home currency (HC) per one unit of foreign currency (FC):

\[S_t = \frac{\text{HC}}{\text{FC}}\]

Think of it as a price:

Direct (natural) quote — our convention:

Indirect quote:

Warning: Market convention is inconsistent. “EUR/USD = 1.10” means USD per EUR in practice. We always use HC/FC.

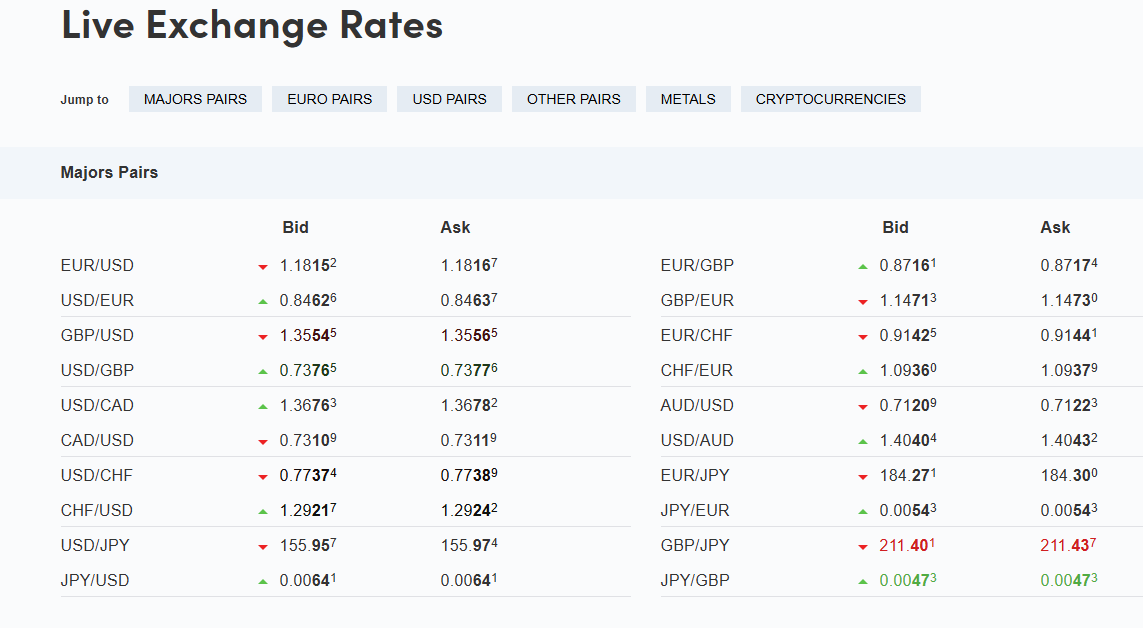

Source: OANDA

To find the cross rate between two non-USD currencies, go through USD:

\[\frac{\text{FC}_1}{\text{FC}_2} = \frac{\text{FC}_1}{\text{USD}} \times \frac{\text{USD}}{\text{FC}_2}\]

Example: Find CHF/GBP given CHF/USD = 0.88 and USD/GBP = 1.27

\[\text{CHF/GBP} = 0.88 \times 1.27 = 1.118\]

Why? USD is the vehicle currency — almost all FX transactions go through USD, even when neither party wants dollars. USD liquidity is the spine of the FX market.

The % appreciation of currency A against B does not equal the % depreciation of B against A.

Example:

| Calculation | Result | |

|---|---|---|

| USD appreciated by | \((1.50 - 1.00)/1.00\) | +50% |

| CAD depreciated by | \((1/1.50 - 1/1.00)/(1/1.00)\) | −33.3% |

The discrepancy grows with the size of the move.

Rule: Always define which currency is the “asset” and compute changes consistently.

When you trade FX, you face two prices:

Always: \(\text{Ask} > \text{Bid}\)

The bid-ask spread = Ask − Bid

This is the dealer’s compensation for providing liquidity and warehousing risk.

| Factor | Effect on spread |

|---|---|

| Liquidity | Major pairs (EUR/USD): 1–2 pips. Exotic pairs (USD/TRY): 50+ pips |

| Volatility | Spreads widen during stress (2008, 2020) |

| Trade size | Institutional spreads < retail spreads |

| Time of day | Spreads widen outside major session overlaps |

Spreads are a transaction cost — they directly affect hedging costs and arbitrage bounds.

Source: OANDA

To convert HC/FC quotes to FC/HC quotes:

\[(\text{FC/HC})_{\text{bid}} = \frac{1}{(\text{HC/FC})_{\text{ask}}}\]

\[(\text{FC/HC})_{\text{ask}} = \frac{1}{(\text{HC/FC})_{\text{bid}}}\]

Why? The bid must always be the smaller number. Inverting the larger direct quote gives the smaller inverse quote.

Given: USD/EUR bid = 1.0950, ask = 1.0955

Find: EUR/USD bid and ask

\[(\text{EUR/USD})_{\text{bid}} = \frac{1}{1.0955} = 0.91282\]

\[(\text{EUR/USD})_{\text{ask}} = \frac{1}{1.0950} = 0.91324\]

Check: bid < ask ✓

Use the law of the worst possible combination:

\[(\text{FC}_1/\text{FC}_2)_{\text{ask}} = (\text{FC}_1/\text{USD})_{\text{ask}} \times (\text{USD}/\text{FC}_2)_{\text{ask}}\]

\[(\text{FC}_1/\text{FC}_2)_{\text{bid}} = (\text{FC}_1/\text{USD})_{\text{bid}} \times (\text{USD}/\text{FC}_2)_{\text{bid}}\]

Example: CHF/USD 1.1520–1.1530, USD/EUR 1.2840–1.2850

Arbitrage:

Shopping around:

Quotes:

Trade:

This cannot persist — massive trading eliminates the opportunity instantly.

No-arbitrage condition: Dealer quotes must overlap.

Quotes:

No arbitrage (X’s bid < Y’s ask). But:

Can be intentional — inventory management. But unsustainable for both banks if they want to stay active in the market.

Rates: EUR/USD = 0.9, CHF/USD = 1.5, EUR/CHF = 0.66

Implied EUR/CHF = EUR/USD × USD/CHF = 0.9 × (1/1.5) = 0.60

Market EUR/CHF = 0.66 → CHF is too expensive in EUR

Trade (start with EUR 0.9m):

Profit: EUR 0.09m — riskless, no net capital. In practice, electronic trading closes these gaps in milliseconds.