The Fragmented World: Geopolitical Threats, Asset Pricing, and the Three Decisions

Hedging, financing, and investment when global integration becomes state-contingent

Main Issues

What does “fragmentation” mean for international finance?

How do geopolitical acts and threats differ?

When does geopolitical risk enter cash flows , discount rates , or real options ?

How does fragmentation affect hedging, financing, and investment ?

Why should we use discount-rate sensitivities , not mechanical spreads?

What are the limits of APV / ICAPM under deep uncertainty?

This lecture follows the APV (L10), ICAPM (L11), and country-risk (L12) lectures. Country risk treated most exposures as a residual cash-flow / APV adjustment for a specific deal. Here we ask what changes when geopolitical risk is forward-looking, networked, and partly priced by markets — and we build a disciplined diagnostic for when it belongs in cash flows, in discount rates, or in flexibility. The central message: realized acts usually enter cash flows / APV; forward-looking threats can affect discount rates only when they are systematic, priced, and not already in the cash flows; deep uncertainty calls for flexibility, not false precision.

Where This Lecture Fits

Previous lectures:

APV (L10) gives the valuation architecture.ICAPM (L11) gives the systematic-risk discount rate.Country risk (L12) is mostly a residual cash-flow / APV adjustment.

This lecture:

What happens when geopolitical risk is no longer just country-specific?

How do threats , networks , and market access affect the three decisions?

L12 asked: “How risky is this deal in this country?”

We are extending, not replacing, the toolkit. The APV structure and the ICAPM discount rate still hold. What changes is the nature of the risk: country risk in L12 was largely a deal-specific residual; geopolitical fragmentation adds forward-looking, networked, and partly priced exposures that interact with all three firm decisions.

Part 1: From Integration to Fragmentation

We start with the benchmark our tools were built for — an integrated world — then show what fragmentation actually changes. The key idea is not autarky but state-contingency: the same link can be open in one state of the world and closed in another.

The Old Integrated-World Benchmark

Trade: lower tariffs, WTO rules, global supply chainsFinance: open capital flows, deep dollar markets, approximate CIPFirms: optimize globally for cost efficiencyValuation: ICAPM + APV works cleanly

This is the world our valuation tools were designed for: one integrated market, open access, and links that stay open.

For decades the working assumption was deepening integration: liberalized trade, free capital flows, a single global market portfolio, and CIP holding to a close approximation. APV and the ICAPM were developed in and for this world. Naming the benchmark explicitly makes it clear what fragmentation perturbs.

What Fragmentation Changes

Fragmentation means global links become state-contingent .

Market access can depend on:

Sanctions and export controls

Bloc alignment

Payment-system access

Capital controls

Technology restrictions

Industrial policy

The same cash flow can have different value depending on whether it remains legally tradable, hedgeable, financeable, and repatriable .

The point is not that the world reverts to autarky, but that access becomes conditional. A cash flow that is freely tradable, hedgeable, financeable, and repatriable in the good state may be none of those in the bad state — and that is a valuation question, not just a political one.

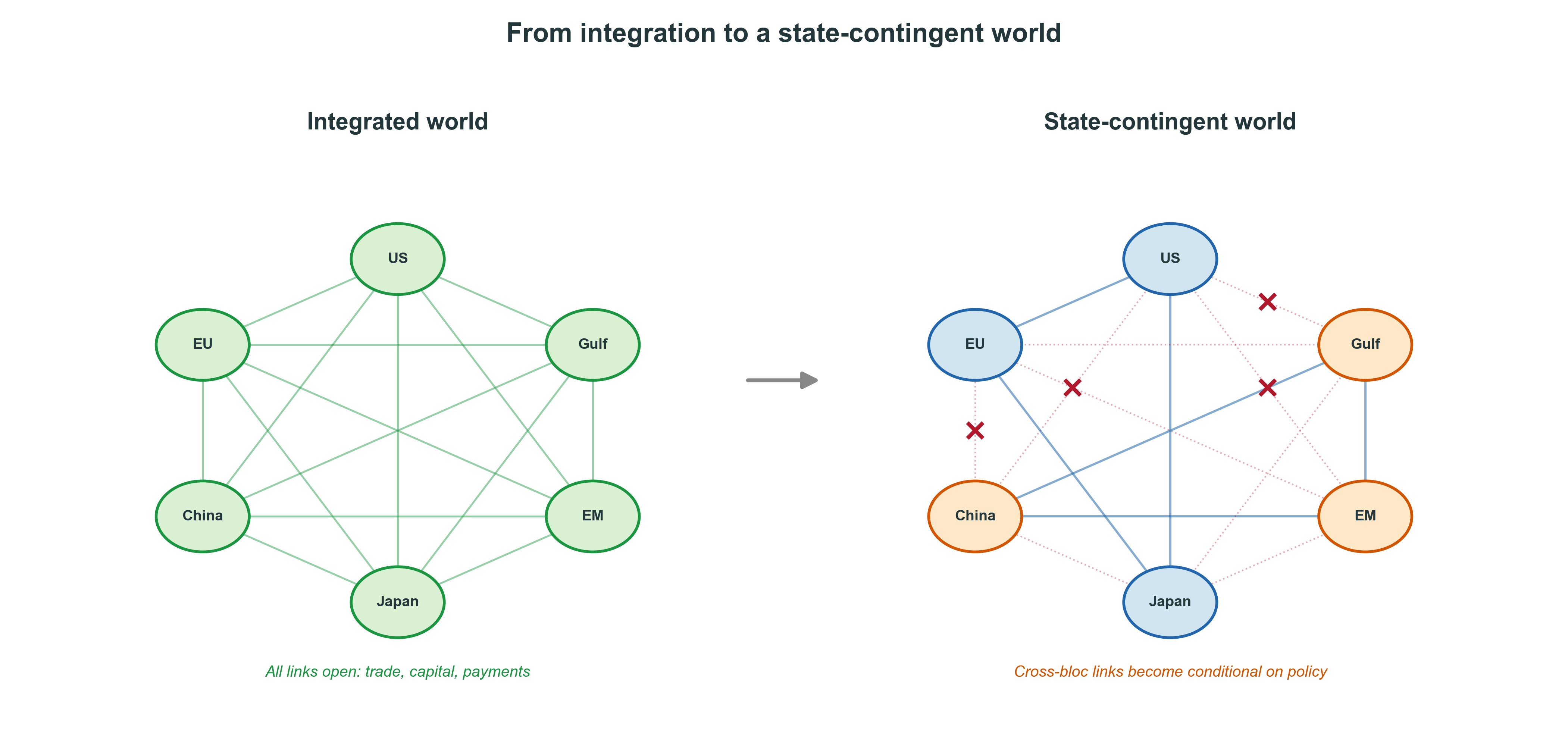

From Integration to a State-Contingent World

Within-bloc links tend to be less policy-contingent; cross-bloc links become more conditional on policy.

The schematic contrasts an integrated network (all links open) with a state-contingent one, where within-bloc links largely persist but cross-bloc links become conditional on sanctions, controls, and alignment. This is re-routing and conditionality, not a return to autarky. It motivates the rest of the lecture: the valuation question is what happens to a cash flow when the links it depends on close in the bad state.

Fragmentation Is Visible, Not Just Rhetoric

Trade and investment links have shifted along geopolitical lines .

Supply-chain resilience and national security now enter economic policy.

Fragmentation is less a return to autarky than a re-routing of global links.

The change is gradual and uneven — but it is measurable in trade and investment data, not just in speeches.

Source note: IMF / Gopinath et al. on geoeconomic fragmentation and changing global linkages.

The IMF work on geoeconomic fragmentation (Gopinath, Gourinchas, Presbitero, Topalova and coauthors) documents trade and FDI increasingly organizing along geopolitical blocs. The honest framing is re-routing and reconfiguration of links, not collapse of trade. We keep this conceptual rather than overloading the slide with a specific chart; the IMF trade/FDI fragmentation chart is an optional add if a clean, dated version is available.

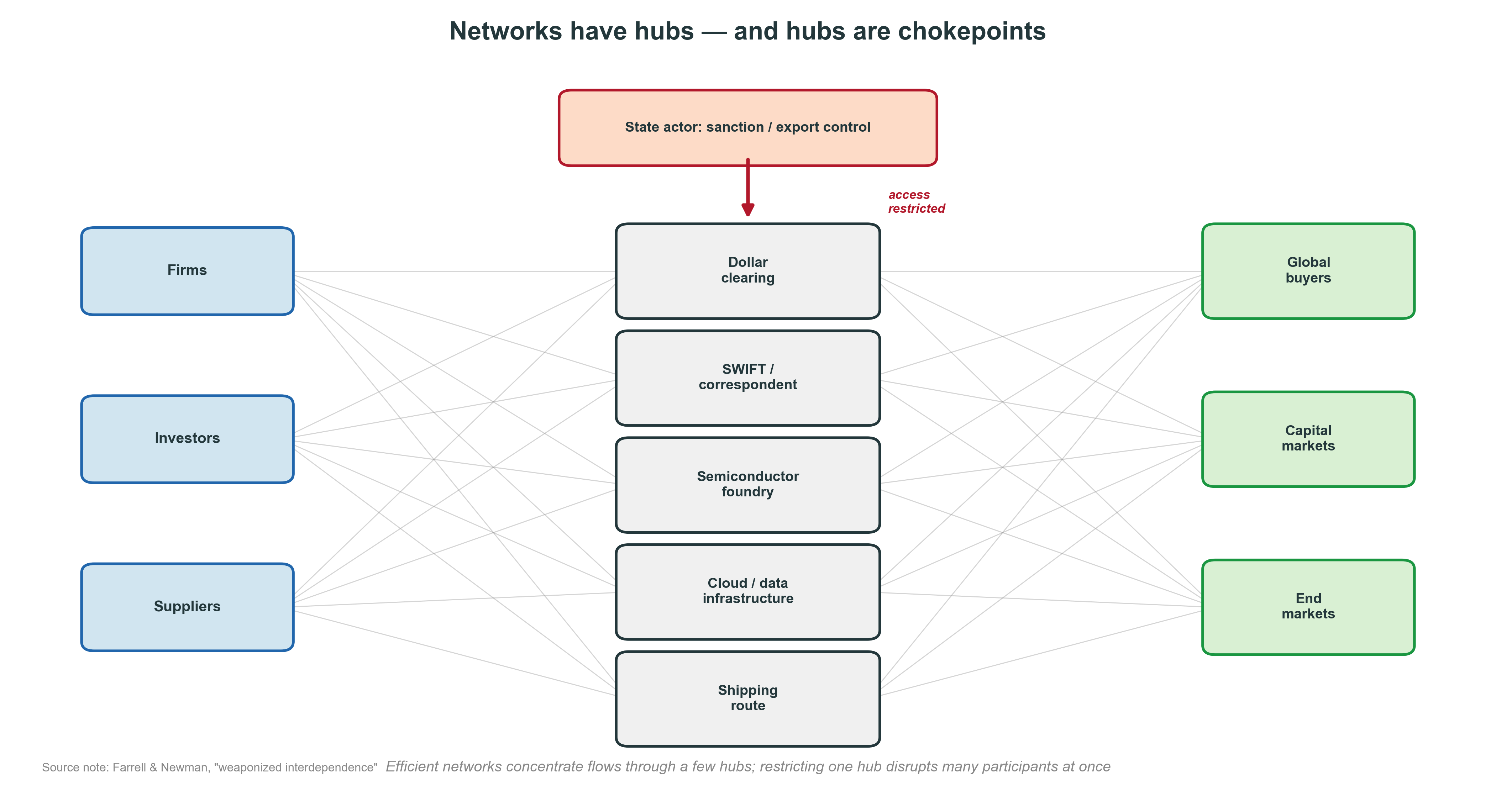

Fragmentation Is About Chokepoints, Not Just Borders

Global integration created efficient networks. But networks have hubs and chokepoints .

Fragmentation is partly the repricing of politically exposed networks .

Examples of chokepoints: dollar clearing; SWIFT / correspondent banking; semiconductor foundries; cloud, data, and telecom infrastructure; critical minerals; shipping routes. Farrell and Newman’s “weaponized interdependence” shows how states exploit network hubs (the “panopticon” and “chokepoint” effects). The valuation-relevant point: a single hub restriction hits many participants at once, so the exposure is networked, not purely country-by-country.

Part 2: Threats vs Acts — The Key Research Distinction

This is the research backbone of the lecture. We separate the measurement of geopolitical risk (Caldara & Iacoviello) from its pricing (Gonçalves, Melone & Ricciardi), and we draw the threats-versus-acts distinction that organizes the rest of the deck.

Geopolitical Risk Is Not One Object

Caldara–Iacoviello GPR decomposes geopolitical risk:

GPR = broad geopolitical riskGPT = geopolitical threats GPA = geopolitical acts

Threats (GPT):

military buildup

sanctions threat

blockade / escalation risk

Acts (GPA):

war begins

sanctions imposed

assets frozen

terrorist attack

Source note: Caldara & Iacoviello (GPR, GPT, GPA); Gonçalves, Melone & Ricciardi.

The Caldara-Iacoviello index is built from newspaper text and splits into a threats component (expectations and risks of adverse events) and an acts component (realizations). This is not a cosmetic split: the two components have different dynamics and, as the next slides show, different pricing properties.

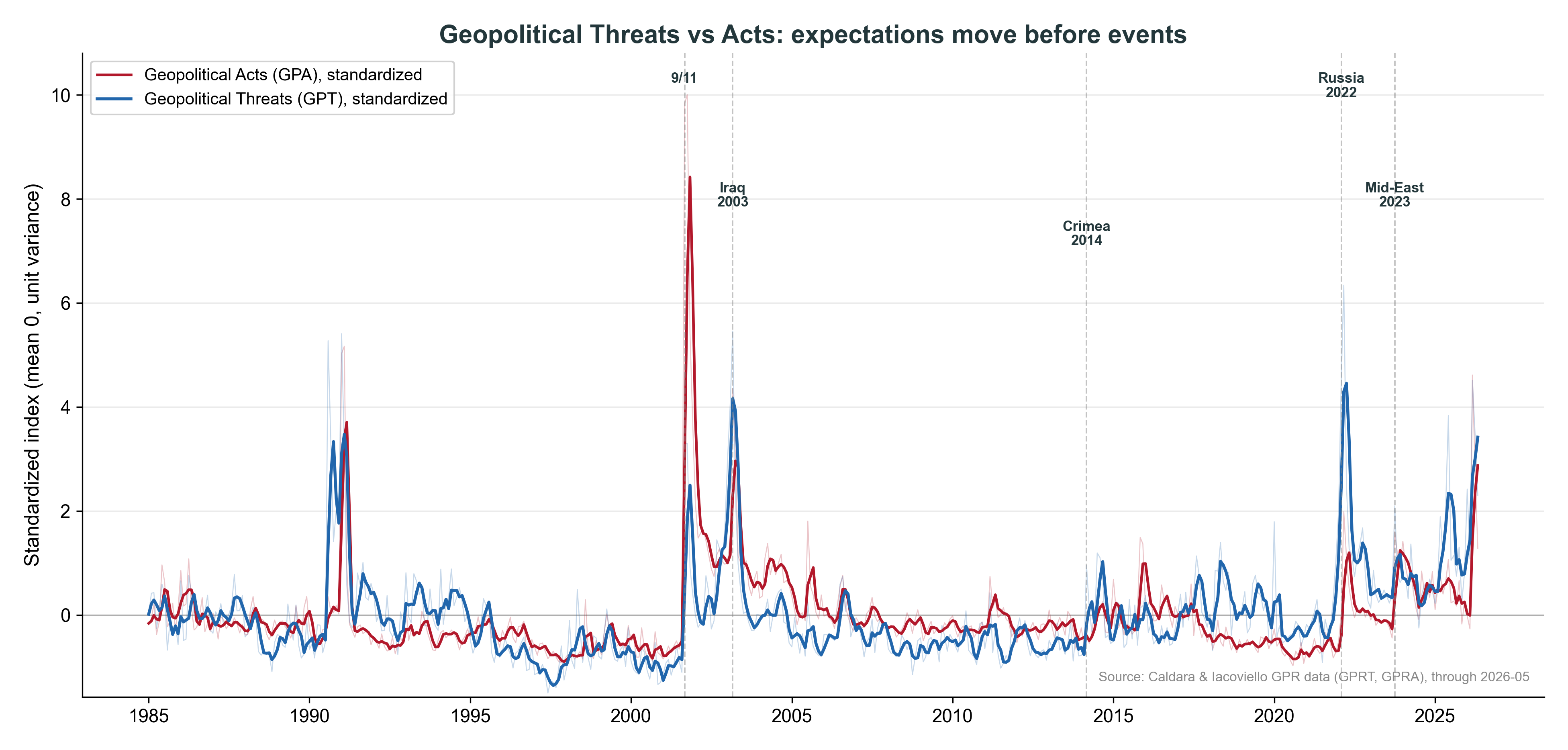

Geopolitical Threats vs Acts: Expectations Move Before Events

Acts are realized shocks. Threats are forward-looking state probabilities — and they often move first.

Real Caldara-Iacoviello data (GPRT and GPRA), standardized to mean zero and unit variance, monthly. Note the pattern: 9/11 is a large acts (GPA) spike; Crimea 2014 and the 2022 Russia invasion show threats (GPT) elevated relative to acts as expectations re-priced. The teaching point is exactly the title: expectations move before — and sometimes without — the event.

Research Frontier: Threats Price Differently from Acts

Recent evidence (Gonçalves, Melone & Ricciardi):

GPT tracks geopolitical-risk perceptions.GPT is linked to investor and firm capital allocation.GPT is priced across asset cross-sections .GPT predicts country-level equity premia .GPA has weaker and less stable links.

Markets price the shadow of conflict, not only conflict itself.

Source note: Gonçalves, Melone & Ricciardi, “The Pricing of Geopolitical Tensions over a Century.”

The frontier result: the threats component is the one that tracks beliefs, capital allocation, and risk premia, and it is priced in the cross-section and predicts country equity premia. The acts component has weaker and less stable links. The paper reports a portfolio-level GPT premium (on the order of ~4% per year on a threat-sorted portfolio) — but that is a portfolio result, NOT a project-WACC input, and it must not be translated into a universal geopolitical spread. The classroom takeaway is the existence and direction of a priced threat component, not a mechanical number.

Why Threats Matter Before Acts Occur

Forward-looking prices move before the event. If investors raise the probability of:

sanctions

conflict

capital controls

forced exit

supply-chain disruption

then valuations can change before any act is realized .

A threat can affect behavior and prices even if the threatened action never occurs .

Source note: Gonçalves, Melone & Ricciardi; Clayton, Maggiori & Schreger on geoeconomic pressure / off-path threats.

This is the mechanism behind the pricing result. A credible threat changes required returns and firm behavior through an off-path channel: the threatened action need never happen for the threat to move capital allocation and prices today. Clayton, Maggiori and Schreger formalize how off-path geoeconomic threats discipline behavior. This is also why threats — not just acts — can belong in the discount rate.

Part 3: The Valuation Diagnostic

This is the analytical heart of the lecture: one diagnostic that routes each exposure to the right valuation channel, and three buckets that follow from it.

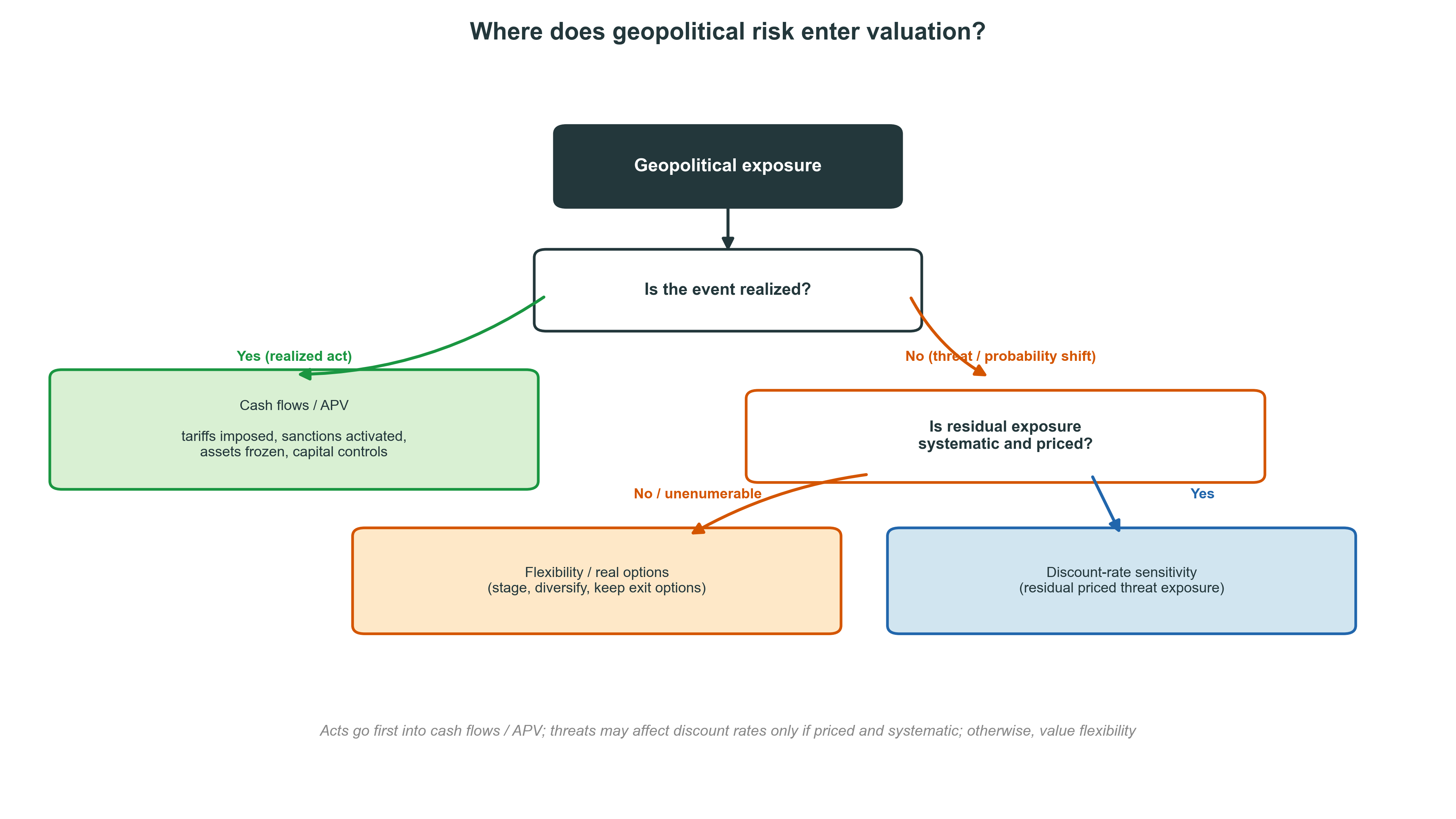

Where Does Geopolitical Risk Enter Valuation?

The decision tree: start from a geopolitical exposure. If the event is realized, it belongs in cash flows / APV (tariffs imposed, sanctions activated, assets frozen, capital controls). If it is a threat or probability shift, ask whether the residual exposure — after modeling direct cash-flow effects — is systematic and priced. If yes, it can justify a discount-rate sensitivity. If not, or if the states cannot be enumerated, the right response is flexibility / real options. This tree governs the three buckets that follow.

Bucket 1: Realized Acts → Cash Flows / APV

Examples: tariffs imposed; sanctions activated; assets frozen; capital controls; taxes changed; licenses revoked.

Valuation treatment:

Scenario cash flows

Trapped cash / transfer-risk adjustment

Insurance and guarantees

Exit or recovery value

Realized acts are, in valuation terms, the L12 country-risk problem: adjust the cash flows / APV , not the discount rate.

Bucket 1 is continuous with Lecture 12. A realized act is a cash-flow event: it changes revenues, costs, taxes, the ability to repatriate, and exit value. Handle it with scenario cash flows, transfer-risk adjustments, insurance/guarantee side effects in APV, and recovery/exit value — exactly the L12 methods.

Bucket 2: Threats → Possible Discount-Rate Sensitivity

Examples: sanctions threat; military buildup; blockade risk; trade-policy uncertainty; strategic chokepoint exposure.

Use a discount-rate sensitivity only if:

Direct cash-flow effects are already modeled .

Residual exposure is systematic .

Exposure is hard to hedge or diversify .

The threat affects marginal investors’ required returns .

DR adjustment = residual priced threat exposure , not a country-risk spread.

Bucket 2 is the genuinely new channel and the one most easily abused. The four conditions are cumulative guardrails: model the direct cash-flow effects first (so you do not double-count), require the residual to be systematic (only systematic risk is priced), require it to be hard to hedge or diversify, and require it to move the marginal investor’s required return. Only what survives all four is a candidate for a discount-rate sensitivity.

Bucket 3: Deep Uncertainty → Flexibility

When states cannot be enumerated :

Do not pretend precision.

Preserve exit options .

Stage investment.Keep supply chains modular .

Diversify across blocs, suppliers, and financing channels.

Deep uncertainty is not just high variance ; it is uncertainty about the model itself .

Bucket 3 is the Knightian case. When you cannot name the states or assign probabilities, neither a cash-flow scenario nor a discount-rate sensitivity is well defined. The disciplined response is flexibility / real options: stage, keep exits open, keep capacity modular, and diversify. We return to this in Part 7.

Part 4: Worked Applications

We now run the diagnostic on three applications: tariffs and industrial policy (mostly Bucket 1), supply-chain chokepoints (Buckets 1 and 2), and financial fragmentation (hedging and financing frictions).

Application 1: Tariffs and Industrial Policy

Tariffs affect:

Revenue volume

Input costs Margins and pass-throughRetaliation risk

Treatment: mostly cash-flow / APV scenario analysis.

Tariff threats may affect timing and option value.imposed affect cash flows.

Tariffs are the cleanest Bucket 1 case: revenue volumes, input costs, margins, and retaliation all flow through cash flows. The threat of a tariff mainly affects timing and the option value of waiting or relocating; the imposed tariff is a cash-flow event. The next slide makes this concrete.

German Automaker Tariff Example

A German automaker sells $400M/year in the US. Tariff as a cash-flow scenario:

No tariff

25%

$400M

8%

$32.0M

15% tariff

40%

$340M

5%

$17.0M

25% tariff

25%

$280M

2%

$5.6M

Severe + retaliation

10%

$200M

\(-1\%\) \(-\$2.0\) M

Expected EBIT $16.0M

Base-case EBIT: $32M . Expected EBIT: $16M — a 50% haircut .

This cash-flow adjustment beats a generic WACC spread.

Verify: 0.25(32) + 0.40(17) + 0.25(5.6) + 0.10(-2.0) = 8.0 + 6.8 + 1.4 - 0.2 = 16.0M. The scenario approach reveals a 50% haircut to expected operating income and forces explicit thinking about volumes, margins, and retaliation. A flat WACC add-on would hide all of that structure and would not distinguish a hard-currency exporter from a domestically exposed firm. Probability weights are subjective, but they are auditable and deal-specific.

Application 2: Supply-Chain Chokepoints

A chokepoint is not just a country exposure — it is a network exposure .

Examples: leading-edge chips; critical minerals; shipping canals; cloud / data infrastructure; defense supply chains.

Taiwan example:

Taiwan is a critical node in advanced semiconductor manufacturing.

A severe Taiwan Strait disruption would affect firms far beyond Taiwan .

Severe scenarios imply global macro losses , but estimates vary widely across studies — treat magnitudes with caution.

The chokepoint framing matters because diversifying across firms or countries does not help much when they all depend on the same node. Taiwan’s role in leading-edge logic is the canonical example. We deliberately avoid a hard “global GDP falls X%” claim: credible studies span a very wide range, and the pedagogical point is the networked, systematic character of the exposure, not a spurious point estimate. This case has both a Bucket 1 element (supply-disruption scenarios) and a Bucket 2 element (residual systematic threat exposure).

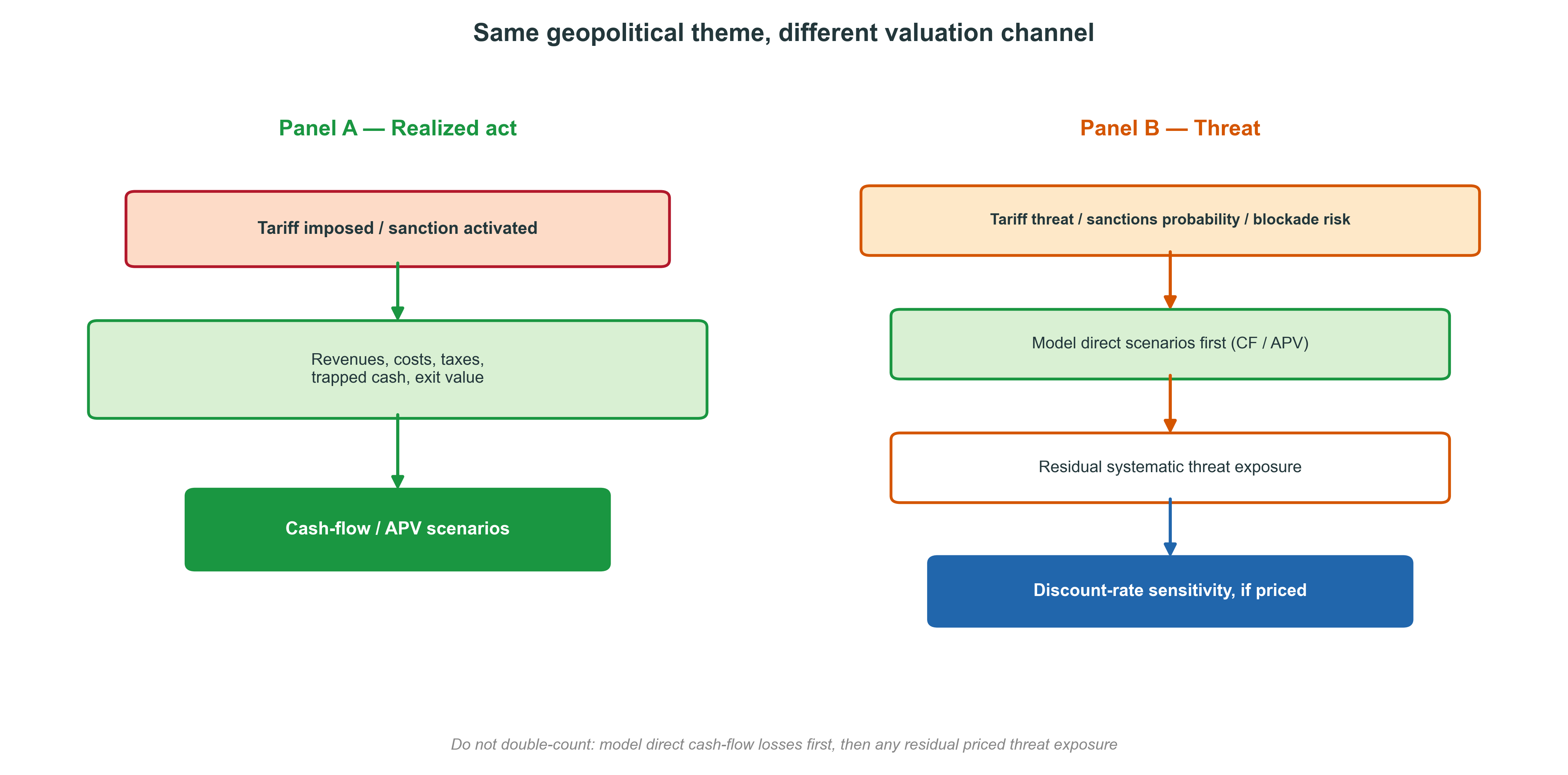

Same Geopolitical Theme, Different Valuation Channel

Do not double-count: model direct cash-flow losses first , then any residual priced threat exposure.

Two panels for the same theme. Panel A — a realized act flows through revenues, costs, taxes, trapped cash, and exit value into cash-flow / APV scenarios. Panel B — a threat is handled by modeling direct scenarios first, then asking whether a residual systematic threat exposure remains that the market prices; only that residual can justify a discount-rate sensitivity. The discipline is to avoid charging the firm twice for the same risk.

Application 3: Financial Fragmentation

Fragmentation can affect:

Payment-system access

Settlement risk

Capital controls

Dollar funding

Cross-currency basis

NDF liquidity

Alternative rails may reduce some frictions over time , but they are not full substitutes .

CIPS = cross-border RMB clearing, not a general SWIFT replacement; SPFS is Russia-focused and limited internationally; mBridge reached MVP stage but remains experimental, not a mature substitute. Source: BIS / Reuters on mBridge; CIPS as RMB clearing infrastructure.

Financial fragmentation shows up as access, settlement, and funding frictions rather than as outright disconnection. On the alternatives: CIPS is an RMB clearing and messaging system, not a general SWIFT replacement; SPFS is largely domestic to Russia with limited international reach; mBridge reached minimum-viable-product stage but is not a mature commercial system. The careful wording avoids overclaiming either collapse or substitution. The next slide develops the hedging-cost angle.

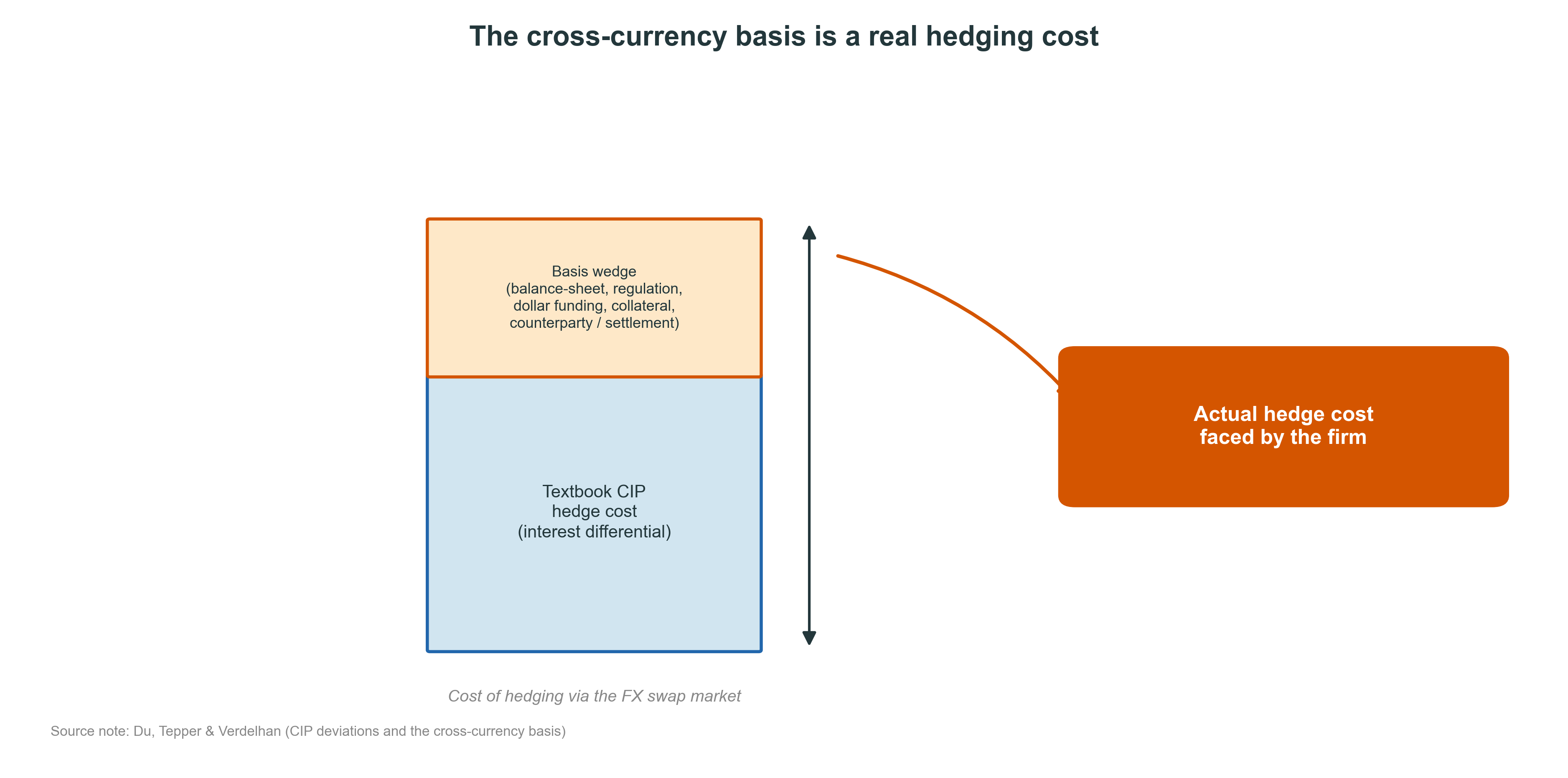

CIP and the Cost of Implementing Hedges

Textbook: CIP links spot, forwards, and interest-rate differentials.

In practice: the hedge also carries a basis — from balance-sheet limits, regulation, dollar-funding pressure, collateral, and counterparty / settlement frictions.

For firms, the cross-currency basis is a real hedging cost , not a free arbitrage.

Post-GFC, covered interest parity holds only approximately: a persistent cross-currency basis reflects balance-sheet costs, regulation, dollar-funding demand, and collateral/counterparty frictions (Du, Tepper & Verdelhan). For a treasurer the basis is not an arbitrage to harvest but a real, sometimes structural, cost of implementing a hedge — and fragmentation-related dollar-funding pressure can keep it elevated. The wedge diagram: textbook cost plus the basis wedge equals the actual hedge cost the firm faces.

Part 5: Discount Rates Without Overclaiming

This part handles the discount rate with discipline. We replace the old “diversification” framing with investability, state the conditions under which threats may move the discount rate, and insist on sensitivities rather than a single point estimate.

Investable Diversification, Not Just Low Correlation

Diversification only works if the asset remains investable .

Questions to ask:

Can investors legally hold the asset?

Can cash be repatriated ?

Can the exposure be hedged ?

Can ownership survive sanctions, delisting, or capital controls ?

Can benchmarks and mandates continue to include it?

Low correlation is useful only if the position remains accessible . Investability can deteriorate even when statistical diversification remains.

This deliberately replaces any “correlation” story. Lower statistical correlation normally improves diversification; the real issue under fragmentation is investable diversification — legal access, liquidity, repatriation, hedgeability, sanctions/delisting survival, and benchmark eligibility. A position that is statistically diversifying but legally or practically inaccessible in the bad state provides no real diversification. The US-China rolling-correlation chart is intentionally excluded from the main deck; if shown at all it belongs in an appendix with the warning that statistical correlation is not investability.

When Threats Can Affect Discount Rates

A discount-rate sensitivity may be appropriate when:

The exposure is to threats , not just realized acts.

Direct cash-flow losses have already been modeled .

The residual exposure is systematic .

The project depends on cross-bloc access or chokepoints .

The exposure is hard to hedge .

The horizon is long enough for regime shifts to matter.

Use DR only for residual systematic threat exposure .

These conditions operationalize Bucket 2. They are intentionally demanding: most exposures fail one or more and should stay in cash flows. The conditions also connect to the research — the priced object is the threat component (GPT), systematic and cross-sectional, which is exactly what a discount-rate channel requires.

Use Sensitivities, Not a Mechanical Spread

Do not report “the” geopolitical premium. Run a sensitivity :

Base: 0 bps

no residual priced threat exposure

Moderate: +50 bps

modest systematic residual

High: +150 bps

material cross-bloc / chokepoint exposure

Extreme stress: +200 bps

severe, hard-to-hedge residual

Report: the valuation range , the exposure narrative , what is already in cash flows , and what remains as priced threat exposure .

Sensitivity, not point estimate.

This slide replaces the old “add a mechanical fragmentation premium” approach, which is explicitly rejected. The numbers here are illustrative classroom sensitivities, presented as a range to be reported alongside the exposure narrative — never as a calibrated universal spread. The discipline is to show how value moves with the assumed residual premium, and to be explicit about what has already been captured in the cash flows so nothing is double-counted.

Policy Uncertainty: Useful, but Secondary

Policy uncertainty can be priced when it is:

aggregate persistent concentrated in bad states

hard to diversify

But mapping an uncertainty index into a project WACC is not mechanical .

EPU and TPU support the uncertainty-premium logic; GPT is more directly geopolitical .

Source note: Baker, Bloom & Davis; Caldara et al. (trade-policy uncertainty); Pástor & Veronesi.

Policy-uncertainty measures (EPU; trade-policy uncertainty, TPU) and the political-uncertainty asset-pricing literature (Pástor & Veronesi; Kelly, Pástor & Veronesi) support the general logic that persistent, aggregate, hard-to-diversify uncertainty can carry a premium. But these are indices, not discount rates: there is no mechanical map from an index level to a project WACC. We treat policy uncertainty as supporting evidence and keep the directly geopolitical GPT channel as the primary one.

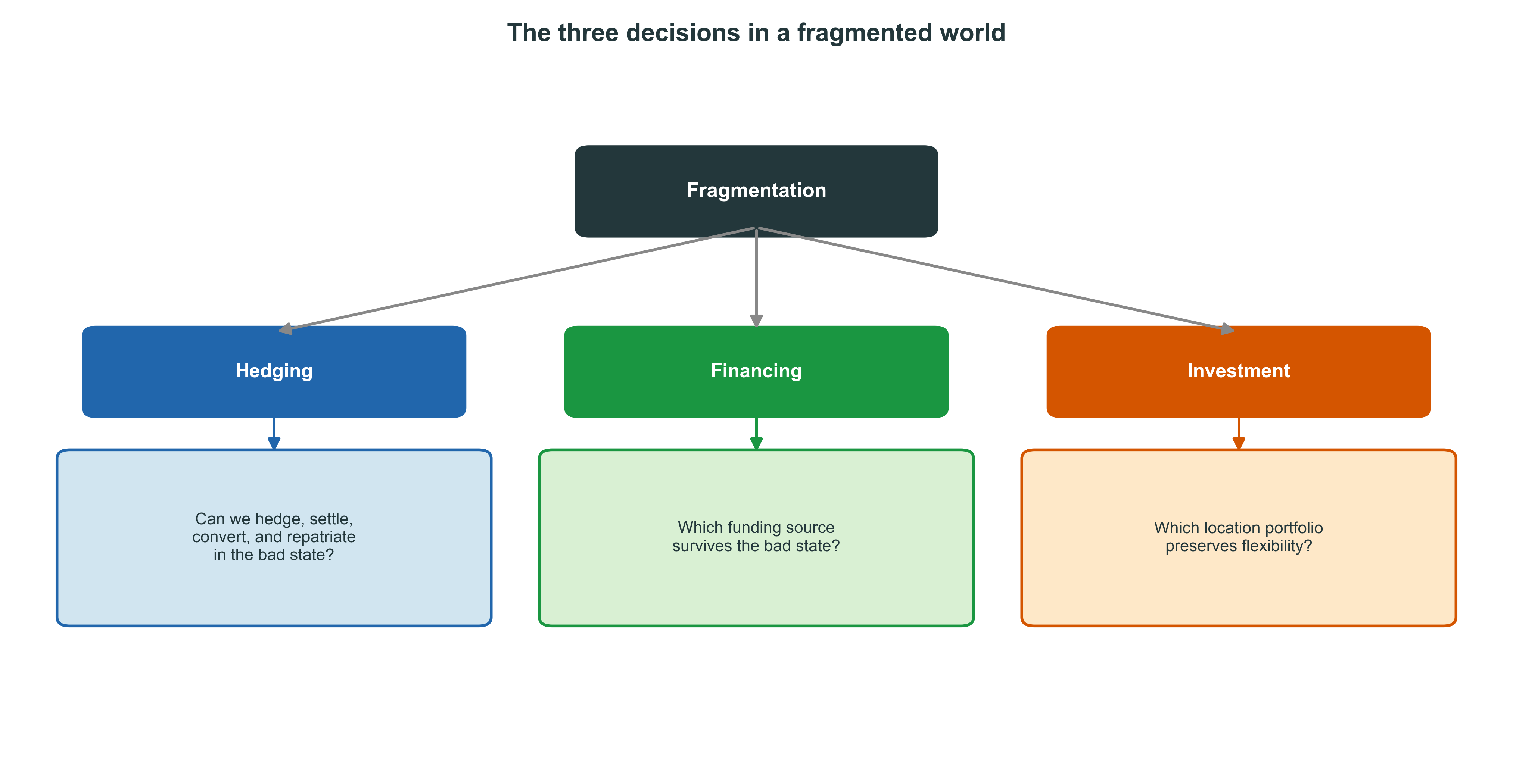

Part 6: The Three Firm Decisions

We now map the analysis onto the course’s three firm decisions. The recurring move is to replace the integrated-world question with its state-contingent counterpart.

The Three Decisions in a Fragmented World

Each decision must be robust to the bad geopolitical state , not just optimized for the good one.

This redraws the old lecture’s “the firm makes three decisions” framing in the current deck style. The unifying theme: in an integrated world each decision is an optimization for the good state; in a fragmented world each must also be robust to the bad state. The next three slides take them one at a time.

Decision 1: Hedging

Traditional question: Should we hedge FX?

Fragmented-world question: Can we hedge, settle, convert, and repatriate in the bad state?

New concerns:

NDF liquidity

Capital controls

Sanctions

Payment-system access

Cross-currency basis

Counterparty location

Hedging is no longer just about the FX level. The binding questions become whether the hedge can be executed, settled, converted, and repatriated when access is restricted — NDF liquidity, capital controls, sanctions, payment-system access, the basis as a real cost (Du, Tepper & Verdelhan), and where the counterparty sits. Operating hedges (diversified production) increasingly complement financial hedges, because no forward protects against loss of market access.

Decision 2: Financing

Traditional question: Where is capital cheapest?

Fragmented-world question: Which funding source survives the bad state ?

Currency of debt

Investor base

Local vs offshore financing

State-contingent market access

Dollar-funding dependence

Sanctions exposure

De-dollarization is gradual, not collapse: reserve-currency shares move slowly and should always be date-stamped.

Financing shifts from “cheapest” to “most resilient.” Currency of debt, investor base, local versus offshore access, and dollar-funding dependence all determine which sources remain available under stress. On de-dollarization: the dollar’s reserve share has drifted down only gradually (IMF COFER), and the RMB faces capital-control and rule-of-law constraints — so the practical advice is to diversify funding access, not to bet on a dollar collapse. Any COFER figure cited in class should be date-stamped.

Decision 3: Investment

Traditional question: Where is production cheapest?

Fragmented-world question: What portfolio of locations gives resilience ?

Tools:

Dual sourcing

Nearshoring / friendshoring

Modular capacity

Staged investment

Exit options

Redundant suppliers

Investment moves from cost minimization to a location-portfolio problem. The tools are real-options levers: dual sourcing, nearshoring/friendshoring, modular capacity, staged investment, exit options, redundant suppliers. The next slide prices the trade-off as an option premium for resilience.

Nearshoring as a Real Option

China only

lowest cost

high geopolitical tail risk

low flexibility

China + Mexico

higher cost

lower tail risk

high flexibility

Mexico only

highest cost / product-specific

lower China exposure

medium flexibility

Any cost premium is illustrative and product-specific .

The extra cost can be interpreted as an option premium for resilience .

The pure cost ranking favors single-sourcing in the lowest-cost location; that ignores tail risk and flexibility. Dual sourcing (China + Mexico) costs more but buys the option to shift production if tariffs, sanctions, or disruptions hit — valuable precisely when uncertainty is high and horizons are long. We deliberately do not assert a specific cost premium (e.g., “+15%”): premia are product-specific and illustrative. The framing is option premium for resilience, not a point forecast.

Part 7: Limits and Humility

We close honestly: the framework is powerful for enumerable risks and silent on truly novel ones. The response to the latter is flexibility and humility, not false precision or paralysis.

What the Framework Does Well

The framework works when we can:

Name the states.Assign probabilities .

Estimate state cash flows .

Identify hedge / insurance / financing effects.

Separate direct losses from priced residual threats .

When these hold, the diagnostic routes each exposure cleanly to cash flows / APV, a discount-rate sensitivity, or flexibility.

For enumerable risks — tariff scenarios, supply-disruption scenarios, modellable threat exposures — the framework gives a disciplined, auditable valuation. The five capabilities listed are exactly the inputs the diagnostic needs.

Where the Framework Struggles

Deep uncertainty:

Unknown states

Model uncertainty

Regime breaks

Non-repeatable events

Political discontinuities

This is not just high variance . It is uncertainty about the model itself .

Russia 2022 was, for most firms, not in the scenario set: “SWIFT restrictions plus central-bank asset freeze plus forced exit within months” was unmodeled. Scenario analysis requires naming the states; deep uncertainty is precisely the case where you cannot. This is a limitation of any analytical method, not a defect of this one.

The Response: Flexibility and Humility

When precision is false, preserve optionality :

Shorter commitments

Modular investments

Exit clauses

Staged investment

Diversified suppliers and financing channels

Operating hedges, not only financial hedges

For deep uncertainty, value flexibility / real options rather than pretending to know the premium.

The response to Knightian uncertainty is neither false precision nor paralysis. It is to buy and preserve optionality: shorter commitments, modular and staged investment, contractual exits, diversified suppliers and funding channels, and operating hedges that protect against access loss (which no forward can hedge). Flexibility has the most value exactly when uncertainty is deepest.

Key Takeaways

Fragmentation makes global exposures state-contingent .

Realized geopolitical acts usually enter cash flows / APV .

Geopolitical threats can affect discount rates if priced and systematic .

Do not use a mechanical geopolitical spread.

Use discount-rate sensitivities only for residual systematic threat exposure .

Investability and access matter more than raw return correlations.Hedging, financing, and investment must be robust to bad geopolitical states .

For deep uncertainty, value flexibility / real options .

The eight takeaways summarize the diagnostic and its disciplined use. The single most important message: acts into cash flows, threats into discount rates only when priced and systematic, and flexibility when the model itself is uncertain — with sensitivities, never a mechanical spread, and investability rather than raw correlation as the diversification test.

Appendix: Research Anchors

Measurement: Caldara & Iacoviello — GPR, GPT, GPA.

Pricing: Gonçalves, Melone & Ricciardi — GPT priced, GPA weaker; Pástor & Veronesi / Kelly, Pástor & Veronesi — political-uncertainty premia; Hirshleifer, Mai & Pukthuanthong — war discourse and disaster premia.

Firm exposure: Hassan et al. — firm-level political and country risk.

Fragmentation: Gopinath et al. / IMF — trade and investment fragmentation; Farrell & Newman — weaponized interdependence.

Financial plumbing: Du, Tepper & Verdelhan — CIP deviations and the cross-currency basis.

Optional: Caldara et al. (trade-policy uncertainty); Baker, Bloom & Davis (economic policy uncertainty).

A single consolidated anchors slide so the main deck stays uncluttered. These are the references behind the lecture’s claims: measurement (Caldara-Iacoviello), pricing of threats vs acts (Gonçalves, Melone & Ricciardi; the political-uncertainty literature), firm-level exposure (Hassan et al.), the fragmentation evidence (IMF; Farrell & Newman), and the financial-plumbing frictions (Du, Tepper & Verdelhan).