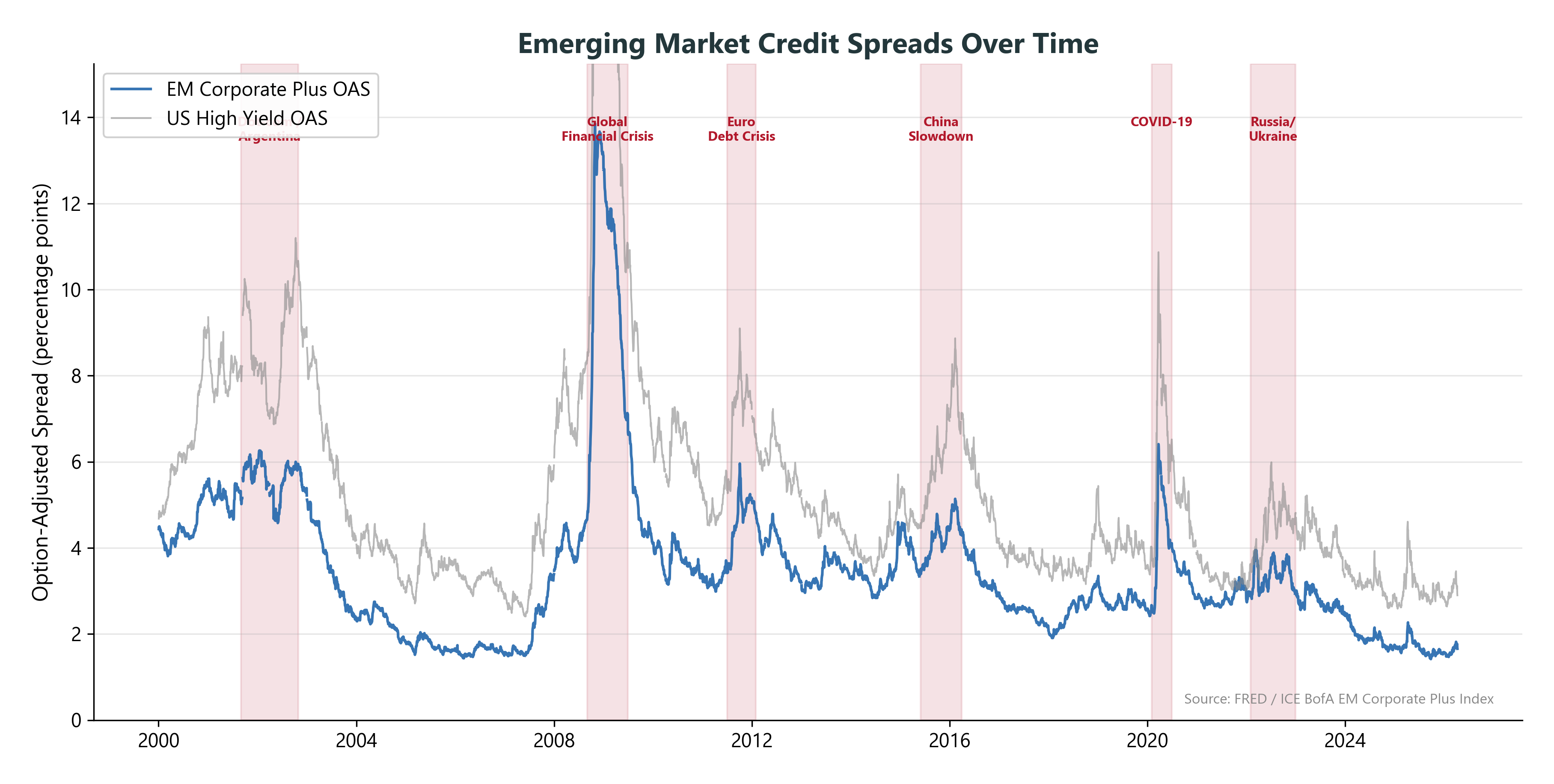

Note: this is an emerging-market corporate OAS series (ICE BofA EM Corporate Plus). It is a high-frequency proxy for EM credit conditions and risk appetite, not a pure sovereign default spread.

From Spreads to Default Probability

The spread implies a market-priced default probability:

Sovereign bond promises \(\$113\) (at 13% yield)

Market values it at \(\$106\) (= \(\$100 \times 1.06\), the Treasury return)

Covers book value, not market value; sudden events covered best

Summary: Measurement Tools

Tool

Pros

Cons

Sovereign spreads

Market-based, real-time

Volatile, credit + liquidity mixed

Credit ratings

Standardized, stable

Lag events, coarse

Political risk indices

Granular, forward-looking

Subjective, infrequent

Insurance premiums

Deal-specific, market-priced

Book value, limited coverage

In practice, use multiple measures together

No single measure captures all dimensions of country risk

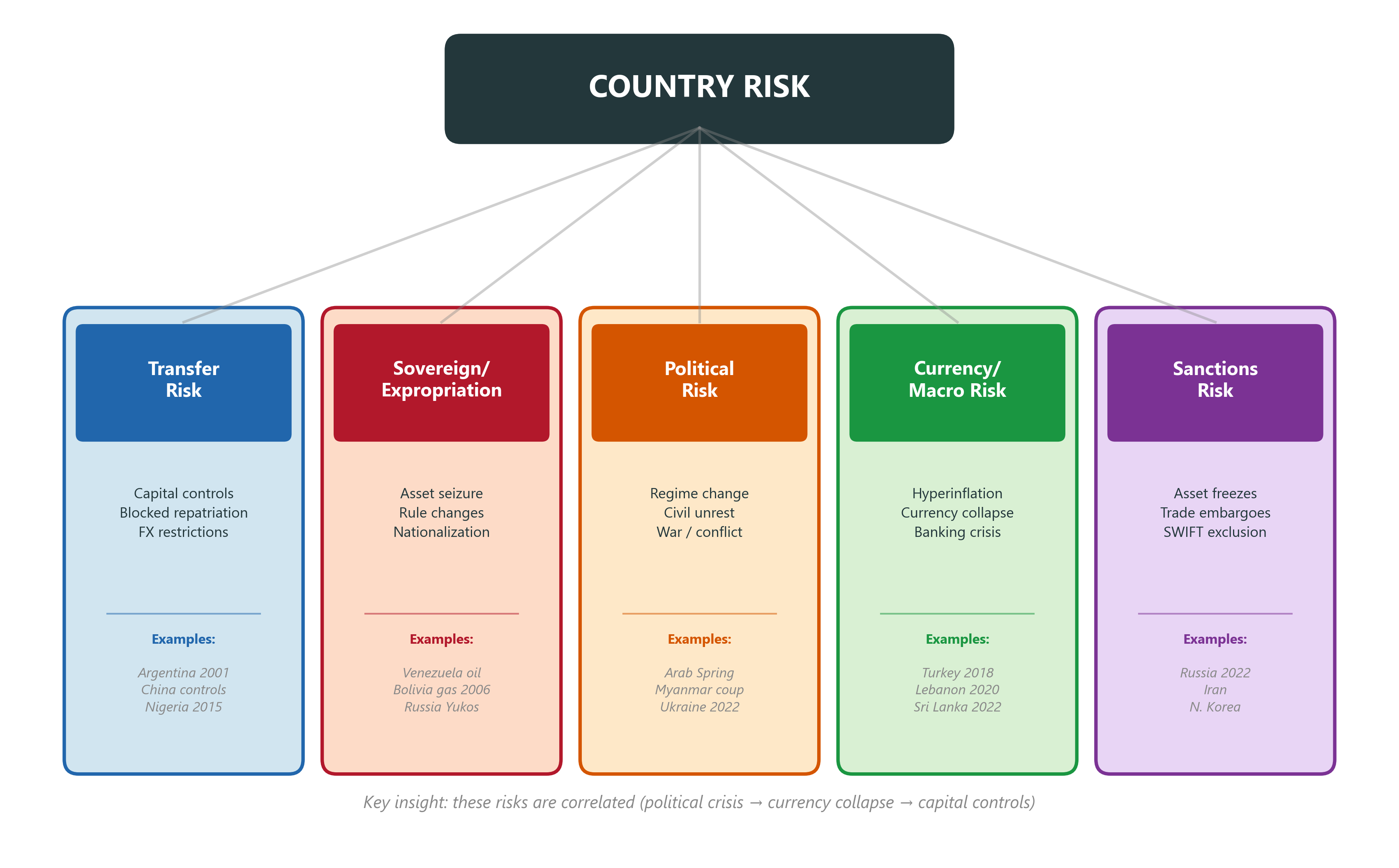

Part 3: The 500bp Fallacy

Common Practice: Adjust the Discount Rate

Many practitioners simply add the sovereign spread to WACC:

US project WACC: 10%

Brazil sovereign spread: 5%

Brazil project WACC: 10% + 5% = 15%

This is called the “500 basis point” approach

This is wrong. It’s convenient, widespread, and fundamentally flawed.

Why It’s Wrong: Problem 1 — Double-Counting

The sovereign spread is already reflected in local interest rates

If you use the local risk-free rate to build your WACC, the spread is already there

Adding it again means you’re counting country risk twice

If you use the US risk-free rate + ICAPM (Lecture 11), you already have the systematic component

The ICAPM discount rate from Lecture 11 already prices whatever systematic component of country risk exists

Why It’s Wrong: Problem 2 — Not All Projects Are Equal

Adding a uniform spread assumes all projects in a country face the same risk

But consider two projects in the same country:

Project

Country Risk Exposure

Export-oriented gold mine

Low: revenues in USD, global buyers

Domestic retail chain

High: local revenues, local regulation

Same country spread, but very different country risk exposure

The DR approach treats them identically — that’s wrong

Why It’s Wrong: Problem 3 — Systematic vs Idiosyncratic

An important component of country risk is country-specific (diversifiable)

Finance theory: only systematic risk deserves a risk premium in the discount rate

Many country-specific events (a single sovereign default, a localized political crisis) are largely diversifiable for a global investor

The ICAPM from Lecture 11 already captures whatever systematic component exists

However: market measures like spreads also embed global risk appetite, dollar liquidity conditions, and contagion effects — so observed spreads are not purely idiosyncratic

Implication: country risk should primarily affect expected cash flows, not the discount rate — but recognize that not all of it is purely diversifiable

Why It’s Wrong: Problem 4 — Ignores Deal Structure

Deal structuring can reduce country risk substantially:

Political risk insurance (MIGA, ECAs, private insurers)

Joint ventures with credible local or international partners

International arbitration and stabilization clauses (ICSID)

Revenue in hard currency, debt in local currency

Critical technology/IP kept offshore where feasible

Adding a flat spread ignores all of these protections

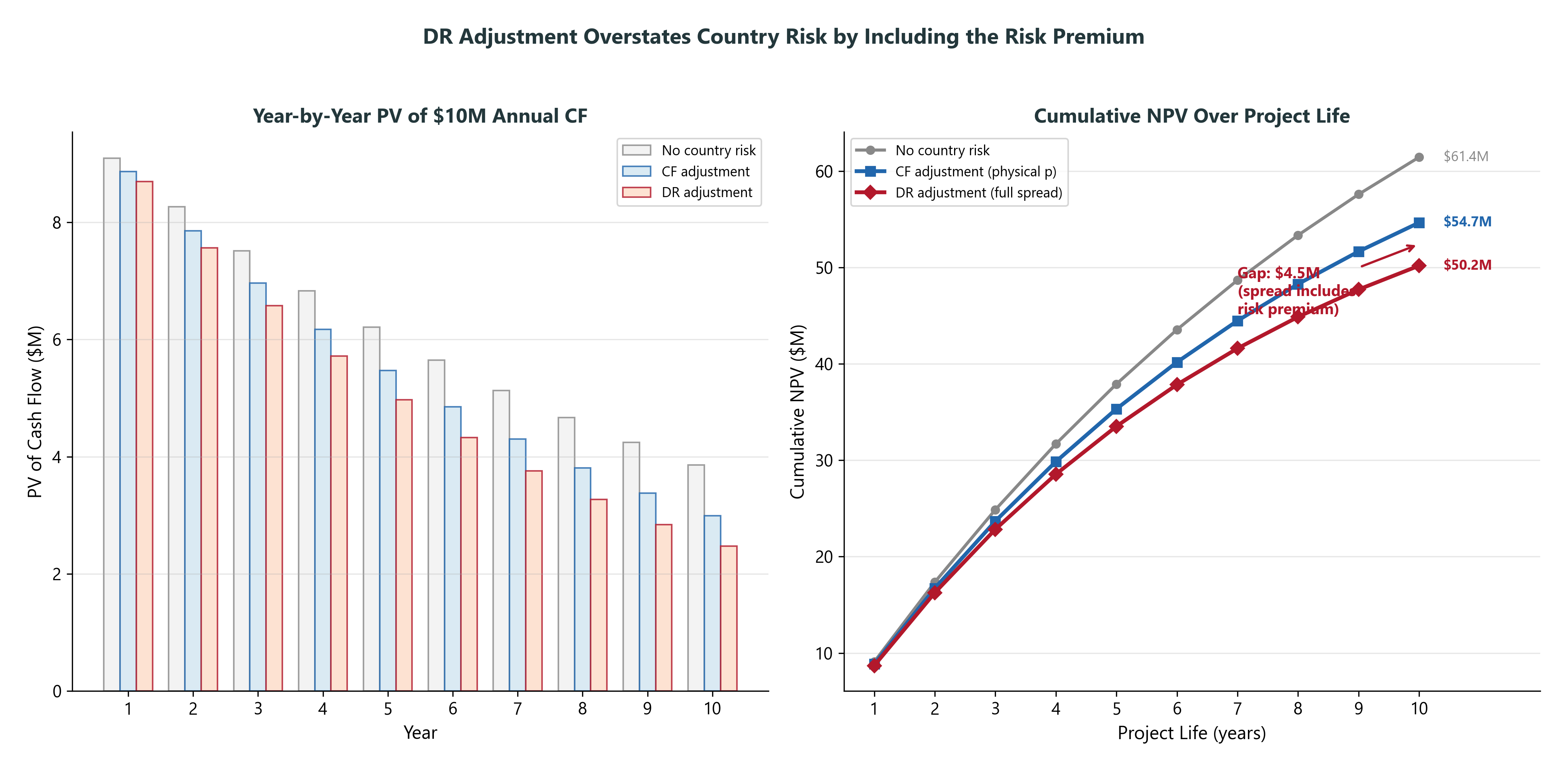

Why It’s Wrong: Problem 5 — Overstates Risk for Long-Lived Projects

Adding the full sovereign spread to the discount rate overstates country risk because the spread includes a risk premium above the actual expected loss

Interlude: Managing Country Risk Before Valuing It

Proactive Management: Reduce Risk Before Pricing It

Country-risk valuation should measure residual risk after feasible mitigation.

Same country, same sovereign spread — different project exposure.

Managers can reduce: probability that an event affects the project; loss given event; timing of disruption; ability to repatriate or redeploy cash; recovery value on exit.

These choices enter valuation via: expected cash flows; scenario probabilities and loss severities; insurance premia/deductibles; APV side effects; exit and abandonment options.

Do not value “country risk in Vietnam.” Value the residual country risk of this specific Vietnam deal.

Transfer Risk: Not All Cash Flows Are Equally Vulnerable

When hard currency becomes scarce, host countries restrict payment channels in roughly this order:

Payment channel

Typical vulnerability

Capital-account transfers

Often blocked first

Dividends / profit repatriation

Ceilings, delays, approvals

Interest / royalties / license fees

More defensible if documented

Trade / technical / management fees

Restricted mainly in severe cases

Establish legitimate, recurring, arm’s-length payment channels before a crisis. Once controls are imposed, it is too late.

Structures must be legal, documented, and arm’s-length.

Proactive Design Levers

Financing and insurance: political-risk insurance (MIGA, ECAs, private insurers); local or third-party debt; DFI / multilateral co-investment (IFC, EBRD, World Bank group).

Contracts and governance: JV with a credible local partner (trades political risk for agency risk); international arbitration and stabilization clauses (ICSID); hard-currency revenues / offtake contracts; local-currency debt as a natural hedge.

Operational levers: keep critical technology/IP offshore where feasible; stage investment to preserve abandonment options.

These protections do not “lower the country spread.” They change the project’s expected cash flows and residual loss distribution.

How Proactive Management Enters APV

APV with residual country risk:

Base-case operating value at the ICAPM rate

Financing and structuring side effects: local-debt tax shields; DFI/ECA guarantees; JV dilution or partner fees; insurance premiums

Residual country-risk adjustment: scenario cash-flow haircuts; insurance deductibles and uncovered losses; delays in compensation; uninsurable sanctions, capital-control, or climate-policy risks

The country-risk adjustment is not exogenous. It depends on the chosen structure.

The Right Approach

Separate the discount rate from country risk; value the residual:

Discount rate — ICAPM / globally integrated capital-market discount rate. Captures systematic risk only (world market and currency factor betas); no country-risk premium added.

Expected cash flows — adjust for residual country risk after feasible mitigation. Scenario-weighted; deal-specific (insurance, JV, debt structure, arbitration clauses).

APV components — separately value insurance premiums, local financing effects, tax shields, guarantees, and other structuring side effects.

The correct country-risk adjustment is deal-specific, not country-generic.

Part 4: Cash Flow Adjustment Methods

Method 1: Bond-Implied Default Probability

Use sovereign spreads to compute annual default probability, then “haircut” cash flows:

Step 1: Extract default probability from spread (quick hazard-rate approximation)

Spread = 4%, recovery rate = 5%

\(p \approx \dfrac{\text{spread}}{1 - \text{recovery}} = \dfrac{0.04}{0.95} \approx 4.2\%\) per year

Useful for a first pass, but it compresses credit risk, liquidity, the credit risk premium, and recovery assumptions into one number. The earlier one-period bond-pricing derivation is related but not identical.

Step 3: Discount at ICAPM rate (no country premium!)

Method 1: Worked Example

Year

Base CF

\((1-p)^t\)

Adjusted CF

PV at 10%

1

$10.0M

0.958

$9.58M

$8.71M

2

$10.0M

0.918

$9.18M

$7.59M

3

$10.0M

0.879

$8.79M

$6.61M

4

$10.0M

0.842

$8.42M

$5.75M

5

$10.0M

0.807

$8.07M

$5.01M

PV of CFs

$33.67M

Assumptions: \(p = 4.2\%\)/year (spread 4%, recovery 5%), ICAPM rate = 10%, base CF = $10M/year. No initial investment subtracted — this is a PV of cash flows, not an NPV.

Method 1: Limitations

This approach assumes:

Binary outcome: either the project survives or it’s a total loss

Reality: many country risk events cause partial loss (tax increase, regulatory change)

Constant default probability: same \(p\) every year

Reality: risk changes over time (elections, commodity cycles)

Same risk for all projects: uses sovereign default as proxy

Bottom line: good for a quick estimate, but too crude for large investments

Method 2: Scenario Analysis

Define country-specific scenarios and assign probabilities:

Scenario

Prob.

CF Impact

Weighted CF

Base case (stable)

60%

$10.0M

$6.00M

Mild deterioration

20%

$7.0M

$1.40M

Severe crisis

12%

$2.0M

$0.24M

Expropriation

8%

$0.0M

$0.00M

Expected CF

$7.64M

More flexible than bond-implied method

Can model partial losses (not just binary)

Can vary scenario probabilities over time

Method 2: Strengths and Weaknesses

Strengths: captures partial losses and multiple risk types; reflects proactive choices (insurance, local debt, JV, arbitration, exit rights, staged investment); allows time-varying probabilities; forces explicit thinking about what can go wrong.

Weaknesses: probabilities are subjective (who decides 8% expropriation risk?); sensitive to scenario design (missing scenarios bias the answer); can be manipulated; hard to audit or benchmark across projects.

Scenario probabilities and loss severities should reflect deal-specific protections, not country-level averages.

Method 3: APV with Political Risk Insurance

“Probably the best approach” — market-priced, deal-specific.

Base case uses the ICAPM rate from L11 and base-case cash flows

Premiums are quoted by MIGA / ECAs / private insurers

Residual losses include deductibles and uncovered sanctions, war, or contract exclusions

Method 3: Advantages

Market-based and deal-specific

Prices the actual risks the insurer is willing to cover

Separates insured and uninsured country-risk exposure

Fits naturally into APV

Method 3: Caveats

Coverage may be unavailable for some countries, sectors, or events

Often covers book value or defined losses, not full market value

Compensation can be delayed

Covert expropriation or regulatory harassment may not trigger coverage

Sanctions, war, or contract exclusions can leave residual risk

Insurance reduces risk; it does not eliminate all country risk

Comparing the Three Methods

Method

Best For

Key Limitation

Bond-implied CF

Quick estimate

Binary outcome only

Scenario analysis

Complex, multi-risk

Subjective probabilities

APV with insurance

Deal-specific valuation

Not all risks insurable

Never recommended: adding a spread to the discount rate

In practice, use Method 3 as the primary approach, supplemented by Method 2 for uninsurable risks

Method 1 is useful for back-of-the-envelope checks

Part 5: Modern Country Risk

The Post-2020 Landscape

Three new dimensions of country risk:

Sanctions risk: the weaponization of economic interdependence

Russia 2022 as the defining case study

ESG and climate risk: country-level transition and physical risks

Stranded assets, carbon border adjustments

Tax and regulatory convergence: BEPS Pillar Two

Global minimum tax eliminates tax haven arbitrage

These risks were largely absent from textbooks written before 2020

Sanctions as Country Risk: Russia 2022

Lessons from Russia 2022: What Went Wrong

Political risk and sanctions risk were correlated — they hit together, not in isolation

Exposures were treated as ordinary operating assets, not contingent claims

Exit options vanished once sanctions and capital controls arrived

Local partnerships did not eliminate geopolitical exposure

Country-risk scenarios were often too narrow (no sanctions tail)

BP’s Rosneft stake was material to reported reserves, production, and earnings; after the 2022 exit decision, those exposures could no longer be treated as ordinary operating cash flows

Lessons from Russia 2022: Valuation Implications

Include sanctions, asset freezes, and forced-exit scenarios in scenario analysis

Model timing: losses can occur suddenly, not gradually

Preserve abandonment and exit options where possible

Diversify across geopolitical blocs, not only across projects or countries

Monitor sanctions, export controls, payment systems, and ownership rules

Scenario probabilities should reflect deal-specific protections (insurance, exit triggers, structuring) — not just country-level averages.

ESG and Climate as Country Risk

Stranded asset risk:

Fossil fuel investments in carbon-dependent countries (Saudi Arabia, Nigeria, Indonesia)

If global transition accelerates, these assets lose value regardless of country stability

Physical climate risk:

Infrastructure in flood/drought-prone areas (Bangladesh, Vietnam)

These risks compound over the project’s life

Transition risk: carbon border adjustments (EU CBAM) penalize countries without carbon pricing

Climate Risk in the CF Framework

Use scenario analysis (Method 2) with climate-specific scenarios:

Scenario

Prob.

Impact on CF

Orderly transition (Paris targets)

30%

Gradual decline after year 5

Delayed transition (sudden policy)

40%

Sharp decline in year 8-10

No transition (business as usual)

20%

CFs stable, physical risks rise

Accelerated transition

10%

Rapid decline from year 3

TCFD/ISSB provide disclosure frameworks for climate scenario analysis; firms often use external scenario sets such as NGFS or IEA

Climate-transition and physical risks belong in scenario cash flows — carbon prices, CBAM, stranded assets, capex needs, and disclosure costs should be modelled explicitly

Climate risk is back-loaded (10+ years) — DR adjustment even less appropriate

Discount rate doesn’t change — these are CF adjustments

BEPS Pillar Two: Mechanics

OECD/G20 global minimum tax framework

Applies to MNE groups above the €750M consolidated revenue threshold (smaller firms out of scope)

Targets a 15% effective minimum tax rate per jurisdiction

Operates via IIR (income inclusion), UTPR (undertaxed profits) and QDMTT (qualified domestic minimum top-up tax)

If a subsidiary’s effective rate < 15%, a top-up is collected — often domestically via a QDMTT, otherwise via the parent

Implementation began from 2024 onward, but timing and mechanics vary by jurisdiction

Implementation is evolving and jurisdiction-specific; update examples before teaching.

BEPS Pillar Two: Valuation Implications

Reduces value of tax holidays and low-tax structures for in-scope MNEs

Raises effective tax rates in some jurisdictions; tax incentives become less durable

Increases compliance and reporting costs; requires scenario analysis for jurisdiction-specific timing

Tax shields from low-tax subsidiaries may shrink for in-scope groups (affects APV Step 2)

Country attractiveness shifts toward real factors: infrastructure, talent, supply chains

Pillar Two affects expected cash flows and APV side effects, not the country-risk spread.

Part 6: Putting It All Together

Worked Example: Vietnam Manufacturing Plant

A US firm is evaluating a $50M manufacturing plant in Vietnam

For simplicity we ignore taxes on insurance premiums in this example, and we discount the premium stream at the project discount rate. In a full APV, the premium stream could be discounted at a rate reflecting the risk and contractual nature of the obligation.

Comparing All Three Methods

Method

NPV

Comment

DR adjustment (wrong)

$13.8M

Conceptually flawed, inflexible

CF adjustment (bond-implied)

$12.6M

Consistent estimate, but binary

APV with insurance (preferred)

$17.1M

Market-priced, deal-specific

Difference: $3.3M between DR and APV approach (19% gap)

DR and CF methods give similar results when derived from the same spread

The APV method is substantially higher because the insurance premium reflects deal-specific risk, not the full sovereign spread

In practice, supplement Method 3 with scenario analysis for uninsurable risks (sanctions, climate, regulatory changes)

The Complete Cross-Border Valuation Toolkit

Step

Component

Lecture

1

Base-case NPV (all-equity, no country risk)

L10 (APV)

\(\hookrightarrow\) Discount rate

L11 (ICAPM)

\(\hookrightarrow\) Cash flows in domestic currency

L11 (returns)

2

+ Tax shields

L10 (APV Step 2)

3

+ Financing side effects (subsidies, guarantees)

L10 (APV Step 3)

4

– Country risk adjustment

L12 (this lecture)

\(\hookrightarrow\) CF adjustment or APV with insurance

Course Connections

L3 (PPP) \(\rightarrow\) determines if FX risk is real

L5 (UIP / carry) \(\rightarrow\) is there an FX risk premium?

L6–8 (hedging) \(\rightarrow\) can you hedge FX risk? At what cost?