But both the numerator and denominator are harder:

Multiple currencies — Which currency for CFs? How to convert? Need consistency.

Multiple tax regimes — Tax shields depend on where you borrow and which rates apply

Country risk — Adjusts CFs or DR or both? (Full treatment in a later lecture)

Funding in different currencies — The basis affects debt cost (Lecture 9)

The EuroCorp example

Running example for this lecture:

EuroCorp (German industrial firm) is evaluating a US manufacturing subsidiary.

Parameter

Value

Investment

USD 55M \(\approx\) EUR 50M

Spot market quote \(X_0\)

1.10 USD/EUR

Valuation spot\(S_0 = 1/X_0\)

0.9091 EUR/USD

USD risk-free rate \(r^{USD}_{rf}\)

4.5%

EUR risk-free rate \(r^{EUR}_{rf}\)

3.0%

1Y forward market quote \(F^X_{0,1}\)

1.1160 USD/EUR

Valuation forward\(F^S_{0,1} = 1/F^X_{0,1}\)

0.8961 EUR/USD

USD unlevered cost of equity

10%

Annual USD FCF (Years 1–10)

USD 9M

Debt ratio (target)

40%

Market quotes are USD/EUR (familiar from trading screens). Valuation formulas in this lecture use EUR/USD, so that USD cash flows are converted to EUR by multiplication: \(55 \times 0.9091 = 50\), so the investment of USD 55M is about EUR 50M.

Valuing Foreign Currency Cash Flows

Notation and quote conventions

Two currencies. HC (home) \(=\) EUR. FC (foreign) \(=\) USD.

Market quote (trading screens)

Valuation rate (all formulas)

Spot, definition

\(X_t\) in USD/EUR

\(S_t = 1/X_t\) in EUR/USD

Spot, EuroCorp

\(X_0 = 1.10\)

\(S_0 = 0.9091\)

Forward, definition

\(F^X_{0,t}\) in USD/EUR

\(F^S_{0,t} = 1/F^X_{0,t}\) in EUR/USD

Forward, EuroCorp

\(F^X_{0,1} = 1.1160\)

\(F^S_{0,1} = 0.8961\)

Conversion rule:\(\;\; C^{EUR}_t \;=\; S_t \times C^{USD}_t \;\) (USD \(\to\) EUR by multiplication; all formulas below use \(S_t\) or \(F^S_{0,t}\), never \(X_t\)).

The fundamental question

Setup: You will receive FC 1 with certainty at time \(T\).

What is its value today in home currency?

You need to move across two dimensions:

Time (future \(\to\) present) — requires discounting

Currency (FC \(\to\) HC) — requires conversion

The question is: in which order?

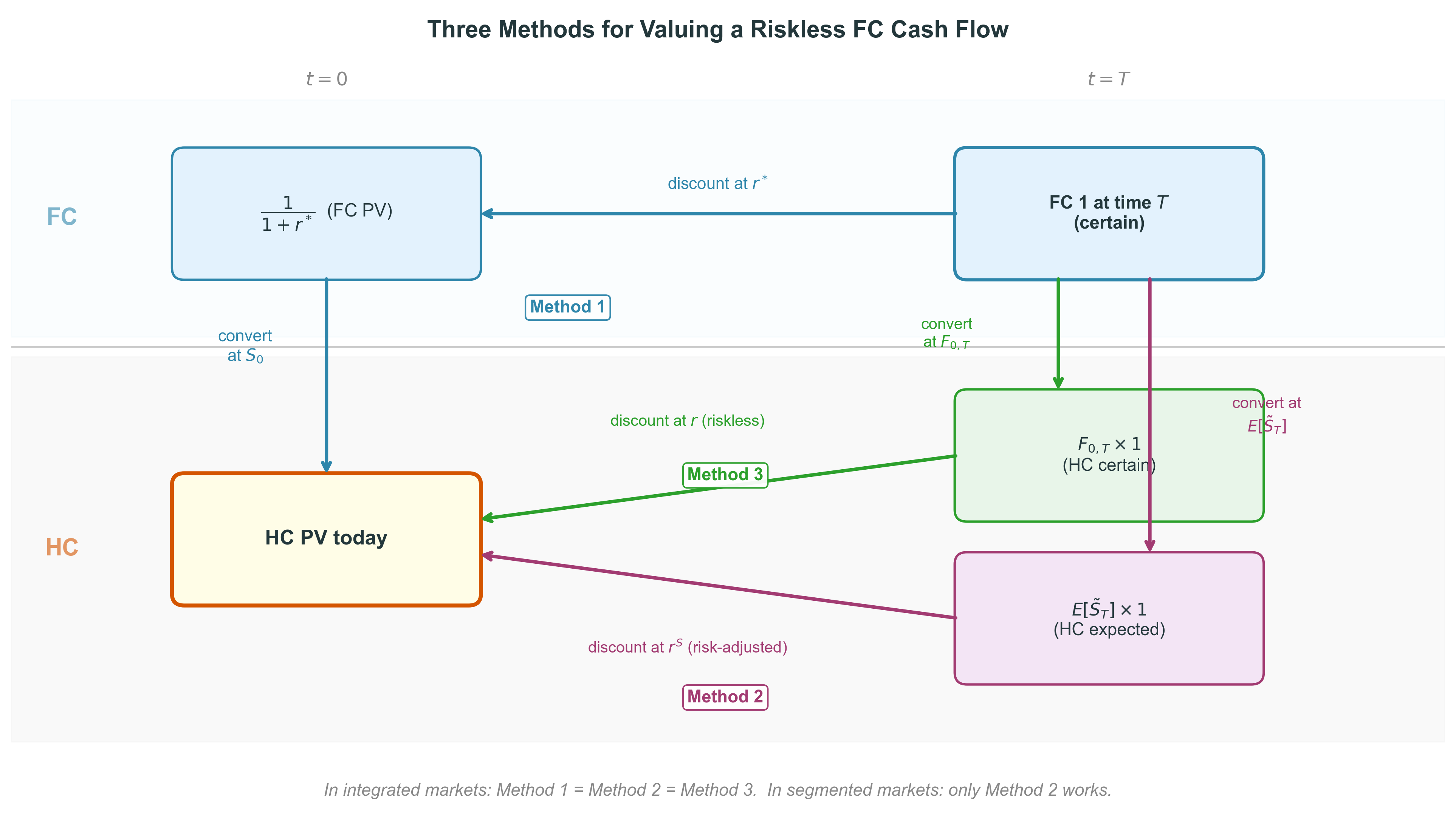

Three methods (riskless FC cash flow)

Method 1: Discount in FC, then convert

First find the present value in FC by discounting at the FC rate. Then convert the FC present value into HC by multiplying by today’s valuation spot \(S_0\) (EUR/USD).

Logic. The FC present value is known today, so converting at today’s spot \(S_0\) is appropriate.

Method 2: Convert at expected spot, then discount

First estimate the HC value of the FC cash flow at maturity: \(\widetilde{S}_T \times C^{FC}_T\). Then discount this risky HC cash flow at a risk-adjusted HC discount rate that reflects both project risk and FX risk.

Note. This requires an explicit exchange-rate forecast and the correct FX risk adjustment — both are difficult (Lecture 5).

Method 3: Convert at forward rate, then discount

Use a forward contract to lock in today the HC value of the FC cash flow: \(F^S_{0,T} \times C^{FC}_T\). This HC value is certain, so discount it at the HC risk-free rate.

Logic. The forward eliminates FX risk; the resulting HC cash flow is riskless, so it gets the riskless discount rate. Because \(F^S\) is EUR/USD, conversion is multiplication.

Do the three methods agree?

Methods 1 and 3 are identical in integrated markets — this is just CIP rearranged. Under our valuation convention, with \(S_t\) in EUR/USD:

Methods 2 and 3 are identical if the HC discount rate \(r^{HC}_{C,S}\) correctly incorporates the FX risk premium. The forward rate is the certainty equivalent of the future spot (Lecture 4).

Optional: in market-quote form (with \(X_t\) in USD/EUR) the same CIP relation reads \(F^X_{0,T}/X_0 = ((1+r^{USD})/(1+r^{EUR}))^{T}\). The valuation form above is what we use throughout.

EuroCorp: riskless cash-flow example

EuroCorp will receive a certain USD 5M in one year. Recall \(S_0 = 0.9091\) EUR/USD and \(F^S_{0,1} = 0.8961\) EUR/USD.

Method 1. Discount in USD, then multiply by \(S_0\).

Both methods give EUR 4.350M. CIP guarantees this. (Equivalent to dividing by the market quotes \(X_0\) and \(F^X_{0,1}\).)

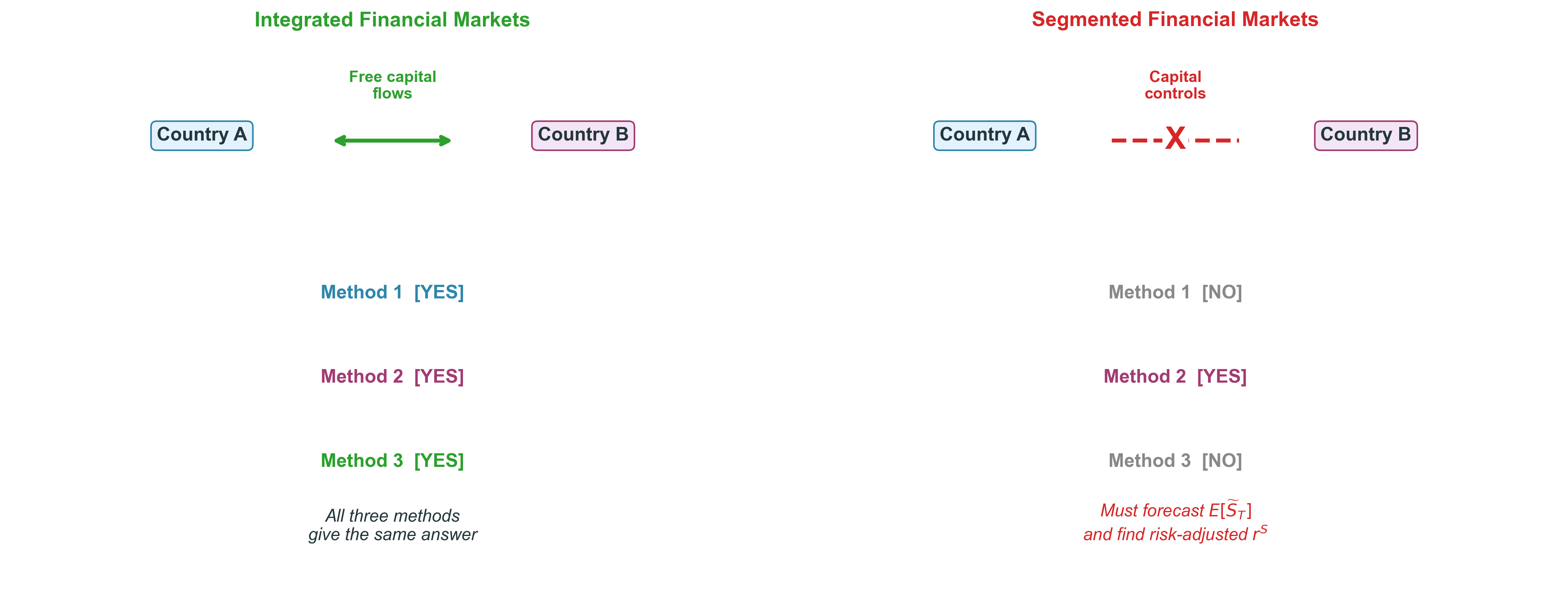

What if markets are segmented?

Segmented markets: only Method 2 works

If financial markets are segmented (capital controls, restricted forward access):

Method 1 fails: No mechanism equates HC value and translated FC value

Investors in each country may discount differently — no arbitrage links them

Method 3 fails: No liquid forward market; CIP doesn’t hold

Can’t lock in a forward rate if the market doesn’t exist

Only Method 2 works. For a real project: forecast \(E[\widetilde{S}_T \times \widetilde{C}^{FC}_T]\) and discount at the appropriate HC risk-adjusted rate \(r^{HC}_{\text{proj},S}\). (For the unit riskless example: forecast \(E[\widetilde{S}_T]\) and use \(r^S\).)

This is bad news — exchange-rate forecasts are unreliable (Lecture 5: random walk).

Practical rule. In integrated markets (EUR/USD, GBP/USD, JPY/USD): use Method 3 for riskless cash flows or Method 1 for risky project cash flows. In EM with capital controls: you may be forced into Method 2.

Risky FC cash flows: Method 1

Now the FC cash flow itself is uncertain: \(\widetilde{C}^{FC}_T\).

where \(r^{HC}_{\text{proj},S}\) reflects both project risk and FX risk. The numerator is the expected EUR cash flow at maturity; discounting at \(r^{HC}_{\text{proj},S}\) gives the EUR present value today.

The covariance complication

In Method 2 the numerator is \(E[\widetilde{S}_T \times \widetilde{C}^{FC}_T]\). In general,

unless \(\widetilde{S}_T\) and \(\widetilde{C}^{FC}_T\) are independent. In practice they are often correlated (e.g., when USD weakens against EUR, \(S_T\) falls and EUR-translated USD revenues fall; commodity exporters: FC revenues and FX often move together).

Implication. You cannot simply multiply an FX forecast by a CF forecast — you must account for the covariance, or use Method 1 in integrated markets.

Risky CFs: equivalence in integrated markets

Methods 1 and 2 give the same answer if the discount rates are consistent. Conceptually:

\[r^{HC}_{\text{proj},S} \;\approx\; r^{FC}_{\text{proj}} \;+\; \text{expected change in } S \;+\; \text{covariance adjustment.}\]

An intuition, not a mechanical rule.

With \(S_t\) in EUR/USD: \(S_t \uparrow\) means USD appreciates vs EUR; \(S_t \downarrow\) means USD depreciates.

Practical rule. In integrated markets (US, EU, UK, JP), use Method 1: forecast CFs in their natural currency, discount at the local project rate, then multiply by \(S_0\).

Compact and familiar — one discount rate captures everything.

What changes internationally?

Cost of equity \(r_E\):

Which market portfolio? Domestic index or global index?

Does FX risk carry a separate premium? (ICAPM lecture)

Cost of debt \(r_D\):

Currency-specific: USD debt vs. EUR debt have different rates

Basis-adjusted: synthetic funding cost \(\neq\) direct cost (Lecture 9)

What changes internationally? (cont.)

Tax shield:

Which country’s tax rate? Parent’s or subsidiary’s?

For EuroCorp: Germany (\(\tau = 30\%\)) vs. the US (\(\tau = 21\%\)). Depends on where the debt sits.

Leverage ratio:

Measured in which currency? Market values fluctuate with FX.

FX changes the measured leverage when debt and project value are in different currencies, or when parent-level leverage is measured on consolidated value. Pure unit conversion alone does not change \(D/V\).

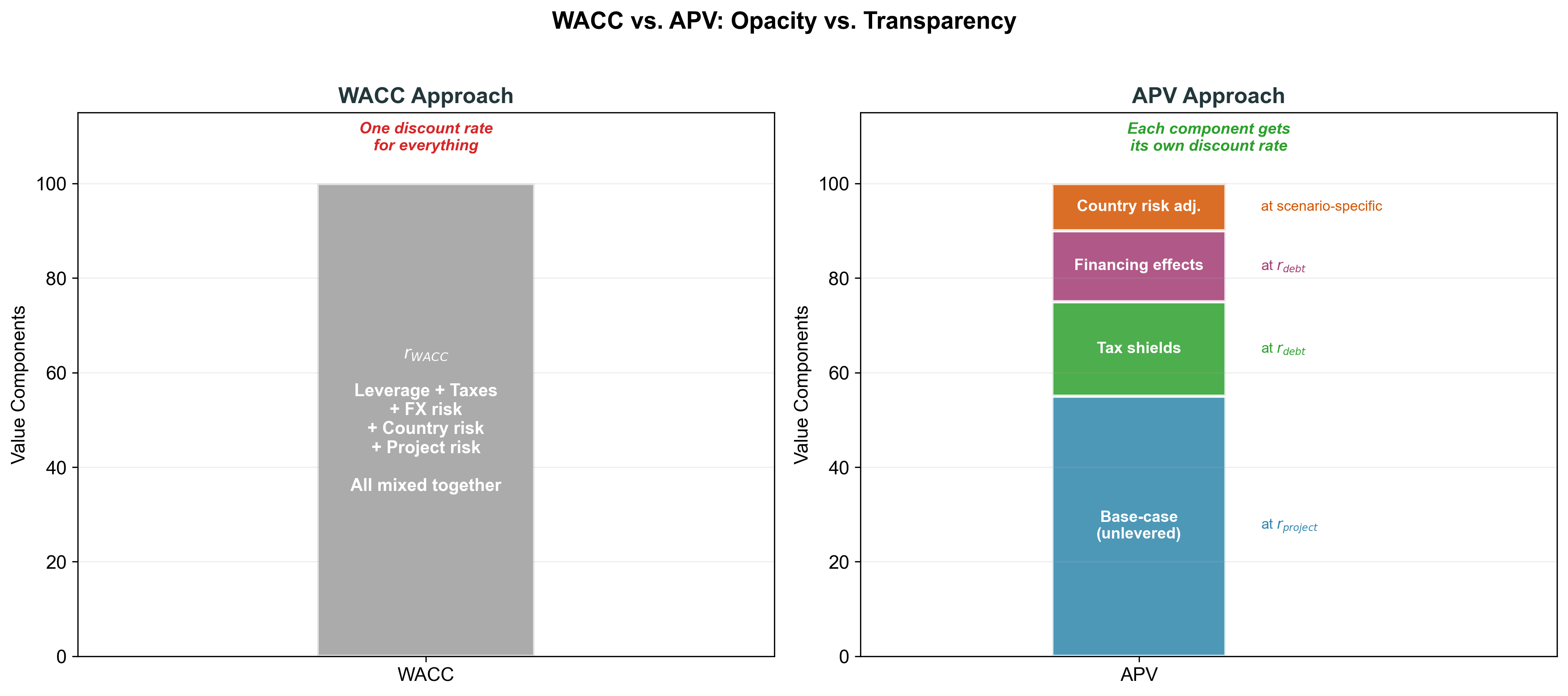

WACC limitations for international projects

Opaque: Mixes leverage, taxes, FX, and country risk into one number — can’t see where value comes from

Constant leverage: Hard to maintain when FX moves change relative values of assets and debt

Country risk: Where does it go? “Add 500bp to WACC” is the most common and worst practitioner approach

Circularity: Need market value weights to compute WACC, but need WACC to compute market values

Subsidized financing: Export credit agencies, development bank loans

Discount rate. For a fixed debt schedule, tax shields are usually discounted at the cost of debt, because the shield inherits the debt’s risk. With target leverage, the debt grows with project value and the tax-shield risk is closer to project risk; many practitioners then discount at the unlevered cost of equity.

For a fixed debt schedule, the tax shield is tied to promised interest payments of known size — that is why practitioners often discount it at \(r_D\). With target leverage, the debt moves with project value, so the tax shield’s risk is closer to project risk and the discount rate moves toward the unlevered cost of equity.

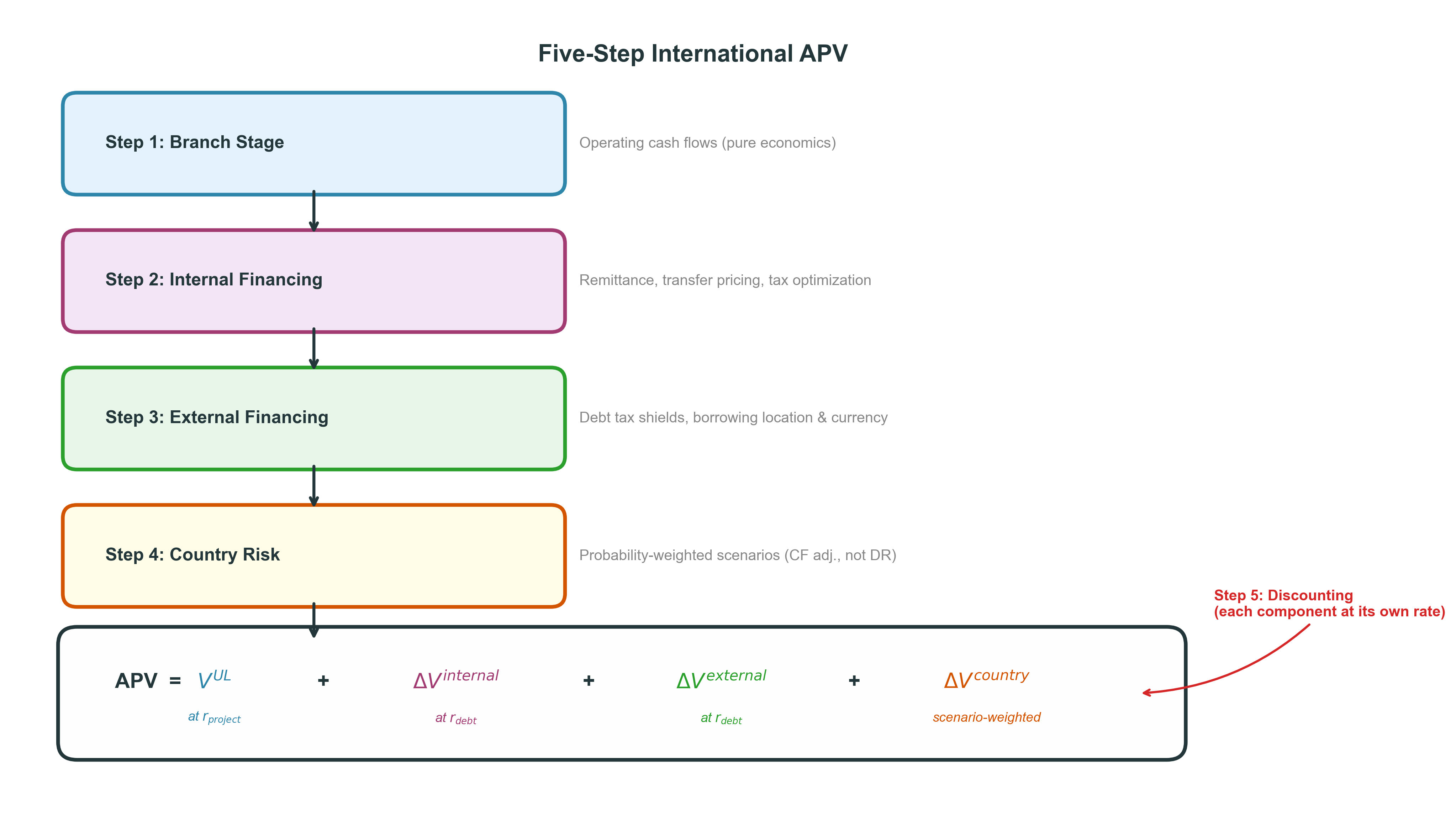

Step 4: Country risk adjustments

Preview only — full treatment in the Country Risk lecture.

Key principle: model idiosyncratic political/country scenarios in the cash flows; keep systematic risk in the discount rate.

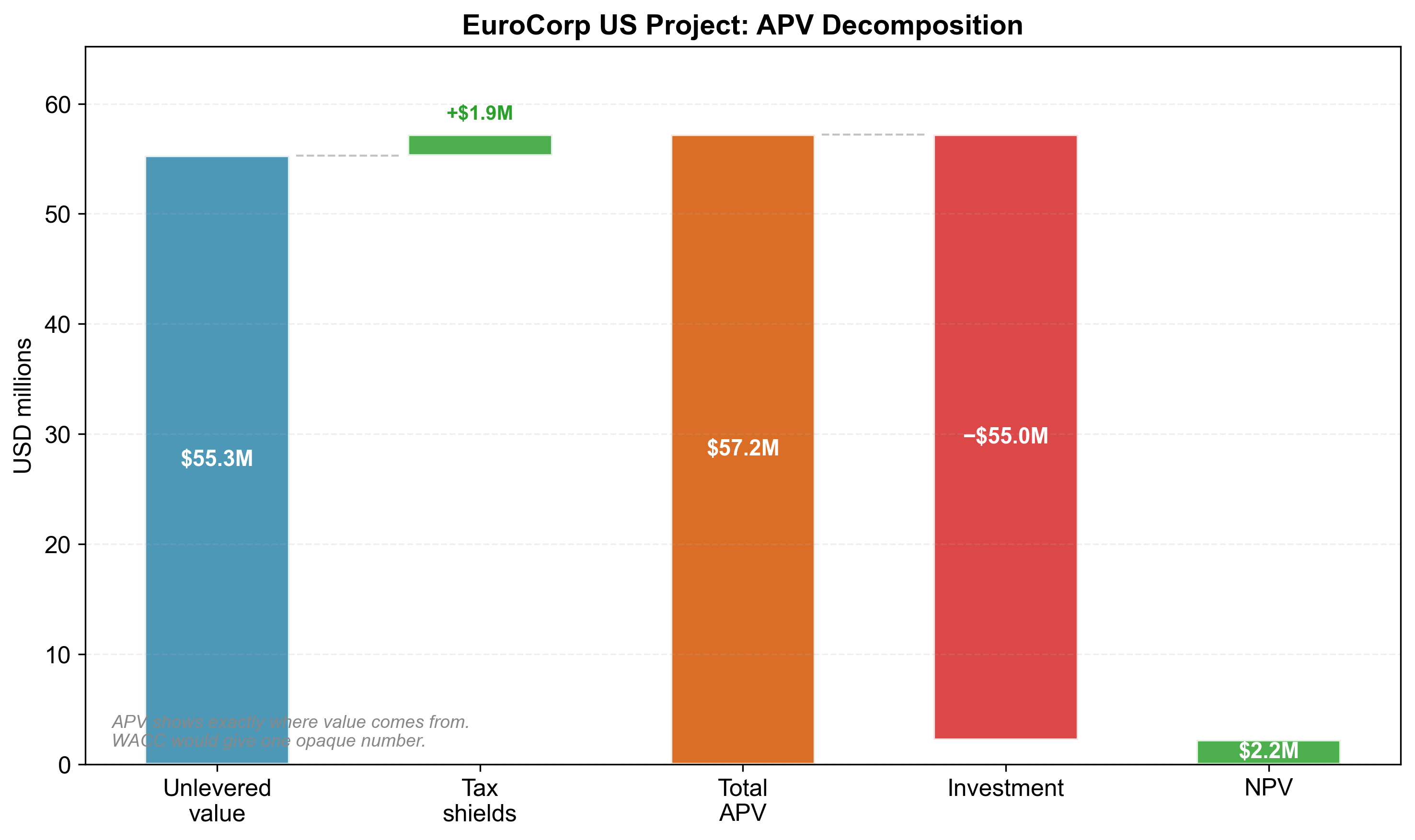

Why does this differ from the WACC NPV (USD 2.9M)? The WACC example assumes a constant target\(D/V\) ratio of 40%, so the implicit tax-shield value grows with project value. This APV example uses a fixed USD 22M debt schedule. WACC and APV give the same value only when the leverage and risk assumptions are aligned.

APV decomposition

APV vs. WACC: the comparison

Feature

WACC

APV

Simplicity

One rate, one DCF

Multiple components

Transparency

Low — all mixed

High — each part visible

Constant leverage?

Required

Not needed

Country risk

“Add 500 bp” (bad)

Explicit CF adjustment (good)

Financing effects

Embedded in rate

Separated and valued

When to use

Quick domestic check

Cross-border projects

WACC and APV give the same answer when leverage is truly constant, country risk is absent, and project risk equals firm-average risk. For international projects these rarely all hold — use APV.

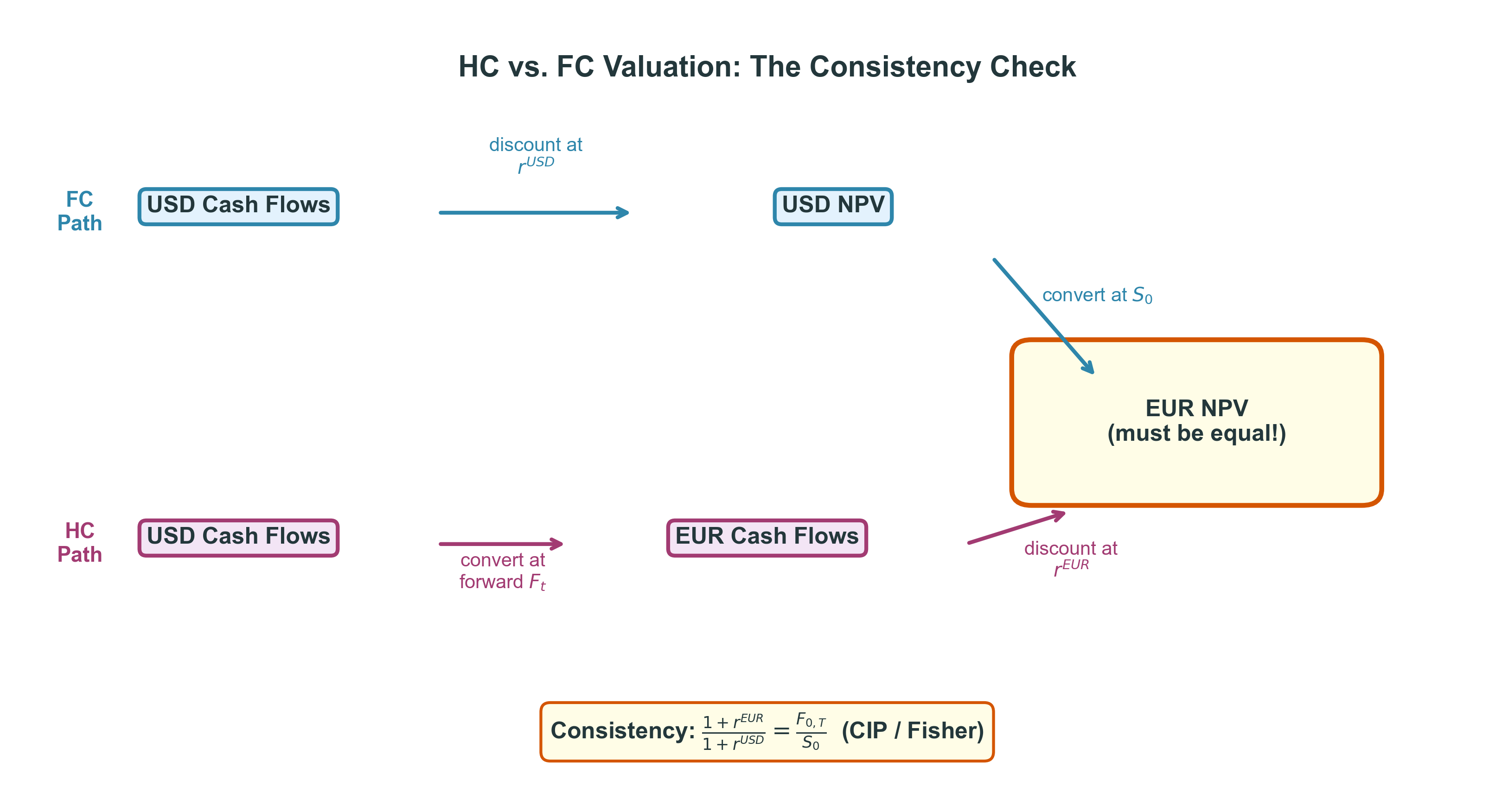

HC vs. FC Valuation: The Consistency Check

Two equivalent DCF approaches

You can value EuroCorp’s US project in either currency.

FC approach (USD).

Forecast project cash flows in USD.

Discount at the USD project discount rate.

Multiply by \(S_0 = 0.9091\) EUR/USD to convert the USD value to EUR.

HC approach (EUR).

Multiply each USD cash flow by the EUR/USD forward \(F^S_{0,t}\) to get EUR cash flows.

Discount those EUR cash flows at the EUR-consistent project discount rate.

The result must match the FC approach.

Both must give the same EUR NPV.

The consistency condition

Why must they agree?

CIP, in valuation form (with \(S_t\) in EUR/USD and \(F^S_{0,t}\) the EUR/USD forward):

Just discount at the USD project rate and convert once at spot

HC approach (convert via forwards) is useful when:

Management wants to see EUR cash flows

Comparing projects across multiple foreign currencies

Building consolidated EUR-denominated financial plans

Always check consistency: if the two approaches give different answers, there is an error in your assumptions.

Caveats for Cross-Border Valuation

Practical warnings

Don’t use speculative currency forecasts. Use forward rates whenever possible.

If forwards aren’t available, check that your forecast is within the range implied by the interest rate differential.

Be careful comparing multiples across countries. P/E ratios differ due to accounting standards, growth rates, and risk premia — not just “cheapness.”

Market risk premium: Take the perspective of the actual shareholders who will bear the risk. If the firm’s shareholders are globally diversified, use the global market premium.

Sensitivity analysis: Difficult-to-quantify aspects (country risk, regulatory change, competitive response) make cross-border valuations inherently uncertain. After finding the APV, stress-test your assumptions.

Summary and Connections

Key takeaways

Three methods for valuing FC cash flows: Discount-then-convert, convert-then-discount, forward-then-discount. All equivalent in integrated markets; only Method 2 in segmented markets.

WACC works but is opaque. It mixes leverage, taxes, FX, and country risk into one rate. Fine for a quick domestic check; dangerous for cross-border projects.

APV is the preferred framework. Five-step approach separates operating value, internal/external financing, and country risk. Each component gets its own discount rate.

Consistency check: HC and FC approaches must give the same answer. If they don’t, there’s an error.

Open question: What discount rate for the base case? \(\to\) answered in the ICAPM lecture.

Connections to the course

Lecture 4 (CIP): CIP guarantees Methods 1 and 3 are equivalent. Without CIP, Method 3 fails.

Lecture 5 (UIP/Predictability): Exchange rate forecasts are unreliable — use forward rates, not speculative forecasts (Method 3 over Method 2 when possible).